Mineral Water Market

Mineral Water Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704622 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

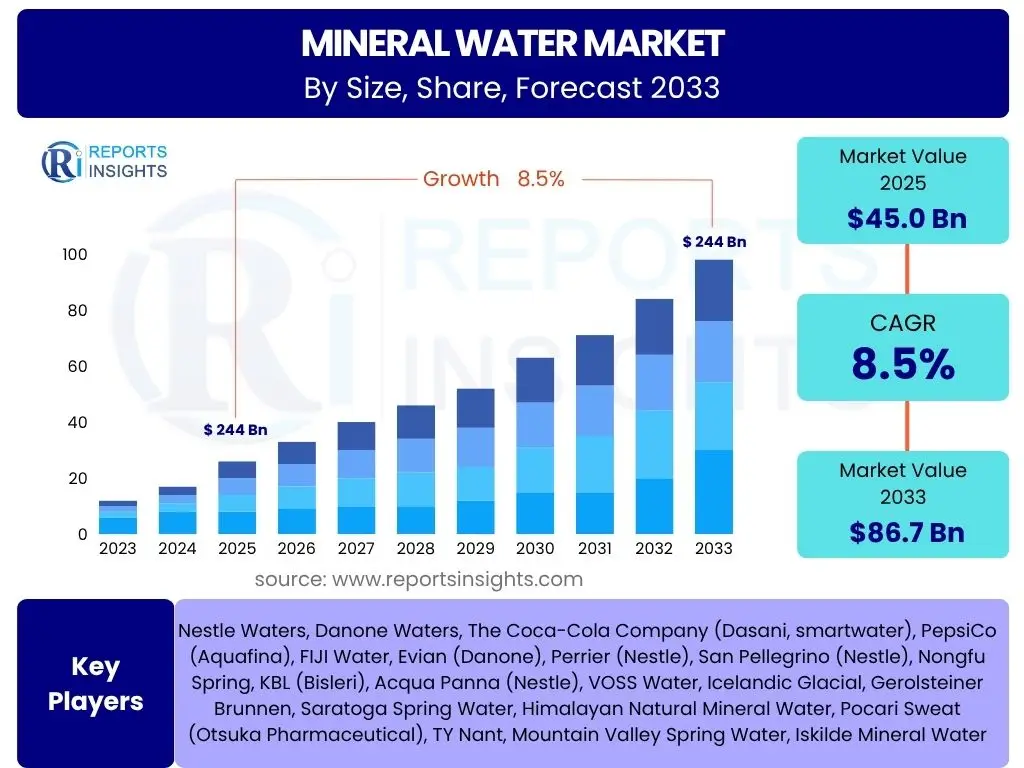

Mineral Water Market Size

According to Reports Insights Consulting Pvt Ltd, The Mineral Water Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 45.0 billion in 2025 and is projected to reach USD 86.7 billion by the end of the forecast period in 2033.

Key Mineral Water Market Trends & Insights

The mineral water market is currently undergoing significant transformation, driven by evolving consumer preferences and increasing awareness regarding health and sustainability. Common user inquiries often revolve around the shift towards natural and functional hydration options, the impact of eco-friendly packaging, and the rise of premium and flavored variants. Consumers are actively seeking beverages that not only quench thirst but also offer added health benefits, such as essential minerals or pH balance, leading to a diversification of product offerings within the sector.

Furthermore, the industry is seeing a notable trend towards sustainable practices, with a growing demand for packaging alternatives that minimize environmental impact. This includes a shift from traditional single-use plastic bottles to options like recycled PET, glass, aluminum cans, and even carton-based packaging. The convenience of e-commerce and home delivery services is also reshaping distribution channels, making mineral water more accessible to a broader consumer base and fostering new consumption patterns.

- Rising consumer health consciousness driving demand for natural and fortified mineral water.

- Increasing preference for sustainable and eco-friendly packaging solutions.

- Growth of premium and artisanal mineral water segments.

- Expansion of flavored and functional mineral water offerings.

- Digitalization of distribution channels, including e-commerce and subscription models.

- Focus on traceability and source transparency for consumer assurance.

AI Impact Analysis on Mineral Water

The integration of Artificial Intelligence (AI) across the mineral water value chain is a topic of growing interest, with users often questioning its potential to enhance operational efficiency, improve product quality, and revolutionize consumer engagement. AI’s capacity to analyze vast datasets can lead to optimized production schedules, predictive maintenance of bottling lines, and more efficient supply chain logistics. This directly addresses user concerns about manufacturing bottlenecks and cost reduction in a competitive market.

Moreover, AI is poised to play a crucial role in understanding nuanced consumer behaviors and preferences. By leveraging AI-driven analytics, companies can tailor marketing campaigns, personalize product recommendations, and even inform new product development, such as specific mineral blends or flavor profiles, based on regional tastes or health trends. While concerns exist about data privacy and the initial investment required, the potential for AI to streamline operations, enhance product innovation, and create highly personalized consumer experiences is significant, making it a key area for strategic investment in the mineral water industry.

- Optimizing production processes and supply chain logistics through predictive analytics.

- Enhancing quality control and safety standards via AI-powered monitoring systems.

- Personalizing consumer experiences and marketing campaigns based on data insights.

- Driving new product development and innovation by identifying emerging taste preferences.

- Improving water source management and sustainability efforts through data-driven environmental monitoring.

- Automating inventory management and demand forecasting for reduced waste.

Key Takeaways Mineral Water Market Size & Forecast

A primary insight from the mineral water market analysis is its robust growth trajectory, underscored by a significant CAGR through 2033. User questions frequently highlight the implications of this expansion for investment opportunities and market saturation. The consistent growth is largely attributed to demographic shifts, urbanization, and a global increase in health and wellness expenditures, positioning mineral water as a staple in modern consumption patterns rather than a luxury.

Another crucial takeaway revolves around the imperative for innovation and sustainability. The forecast emphasizes that companies succeeding in this market will be those that effectively balance product diversification with environmental responsibility. This includes not only advanced filtration and bottling technologies but also a strong commitment to sustainable sourcing and circular packaging solutions. The market’s future dynamism is intrinsically linked to its ability to adapt to environmental pressures and evolving consumer ethical considerations.

- The mineral water market demonstrates strong and sustained growth, projected to nearly double in value by 2033.

- Health and wellness trends are central to market expansion, driving demand for natural and functional hydration.

- Sustainability initiatives, particularly in packaging and sourcing, are critical for competitive advantage and consumer loyalty.

- Technological advancements in production, quality control, and distribution are vital for operational efficiency.

- Emerging markets offer significant untapped potential, while established markets focus on premiumization and niche segments.

- E-commerce and direct-to-consumer models are reshaping market access and consumer purchasing habits.

Mineral Water Market Drivers Analysis

The mineral water market is propelled by several key drivers that reflect a global shift in consumer priorities and lifestyle changes. The escalating awareness concerning health and wellness is perhaps the most significant catalyst, leading consumers to seek out natural and uncontaminated hydration sources over sugary beverages or tap water, especially in regions with perceived water quality issues. This heightened health consciousness extends to a preference for beverages with naturally occurring minerals beneficial for the human body.

Furthermore, rapid urbanization and increasing disposable incomes in developing economies contribute significantly to market expansion. As populations migrate to urban centers, the demand for convenient and safe packaged drinking water rises. Coupled with higher discretionary spending, consumers are more willing to invest in premium or branded mineral water products, perceiving them as a symbol of quality and a healthier choice. This confluence of factors creates a fertile ground for sustained market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Health & Wellness Consciousness | +1.2% | Global, particularly North America, Europe, APAC | Short to Long Term |

| Increasing Disposable Income & Urbanization | +1.0% | APAC, Latin America, Middle East & Africa | Medium to Long Term |

| Perceived Lack of Tap Water Quality | +0.8% | Emerging Economies, parts of North America & Europe | Short to Medium Term |

| Product Innovation & Diversification (e.g., flavored, functional) | +0.7% | Global, particularly developed markets | Short to Medium Term |

| Growth of HoReCa Sector & Tourism | +0.5% | Global, post-pandemic recovery | Short to Medium Term |

Mineral Water Market Restraints Analysis

Despite robust growth, the mineral water market faces several significant restraints that could impede its expansion. Environmental concerns surrounding plastic waste are paramount, leading to increasing consumer and regulatory pressure for sustainable packaging alternatives. The pervasive issue of plastic pollution has prompted boycotts and taxes on single-use plastics, forcing manufacturers to invest heavily in research and development for eco-friendly materials, which can be costly and challenging to implement at scale.

Another notable restraint is the intense competition from alternative beverage categories, including purified water, tap water enhancements, and various soft drinks. Consumers have a wide array of choices, and the perceived premium pricing of mineral water compared to tap water can deter price-sensitive segments. Furthermore, stringent regulations regarding water sourcing, bottling, and labeling vary significantly by region, adding complexity and cost to production and distribution for international players, thereby limiting market penetration in some areas.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Concerns & Plastic Waste | -0.9% | Global, particularly Europe, North America | Short to Long Term |

| Intense Competition from Other Beverages | -0.6% | Global | Short to Long Term |

| High Packaging & Logistics Costs | -0.5% | Global | Short to Medium Term |

| Stringent Regulatory Landscape | -0.4% | Europe, North America, specific emerging markets | Medium Term |

| Consumer Preference for Tap Water in Developed Regions | -0.3% | North America, Europe | Long Term |

Mineral Water Market Opportunities Analysis

The mineral water market is ripe with opportunities, particularly in the realm of product diversification and sustainable innovation. The burgeoning demand for functional and flavored mineral waters presents a significant avenue for growth, allowing companies to cater to consumers seeking more than just basic hydration. Infusion with vitamins, electrolytes, or natural fruit essences can attract new segments and drive premiumization. This trend aligns with the broader health and wellness movement, where consumers are increasingly looking for fortified and beneficial beverage options.

Another substantial opportunity lies in the development and adoption of advanced sustainable packaging solutions. As environmental concerns escalate, brands that invest in and successfully market alternatives like plant-based bottles, aluminum cans, refillable systems, or recycled content will gain a distinct competitive advantage and foster strong brand loyalty. Expanding distribution channels, especially through e-commerce platforms and subscription services, also represents a key opportunity. This not only enhances market reach but also caters to the growing consumer preference for convenience and direct delivery, particularly in urban and digitally connected areas.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Functional & Flavored Mineral Water | +0.9% | Global, particularly Developed Markets | Short to Medium Term |

| Investment in Sustainable Packaging Solutions | +0.8% | Global, especially Europe, North America | Short to Long Term |

| Expansion into Emerging Markets | +0.7% | APAC, Latin America, Middle East & Africa | Medium to Long Term |

| Growth of E-commerce & Direct-to-Consumer Models | +0.6% | Global | Short to Medium Term |

| Premiumization and Artisanal Offerings | +0.5% | Developed Markets (Europe, North America, Japan) | Short to Medium Term |

Mineral Water Market Challenges Impact Analysis

The mineral water market confronts several formidable challenges that necessitate strategic responses from industry players. The escalating backlash against plastic pollution and environmental degradation poses a significant hurdle, as consumers and governments increasingly demand a reduction in single-use plastic bottles. This not only mandates costly shifts in packaging materials and production processes but also impacts brand image for companies perceived as environmentally irresponsible.

Moreover, maintaining consistent water quality and ensuring the authenticity of the "mineral" claim are persistent challenges. As consumer scrutiny over sourcing and natural purity intensifies, brands must invest heavily in advanced filtration, quality assurance, and transparent labeling to avoid reputational damage. Supply chain disruptions, often triggered by climate change events or geopolitical instability, also present a substantial challenge, affecting sourcing, production, and distribution, thereby leading to increased operational costs and potential market shortages.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Plastic Pollution & Environmental Scrutiny | -0.7% | Global, especially Europe, North America | Short to Long Term |

| Maintaining Authenticity & Quality Control | -0.5% | Global | Short to Medium Term |

| Supply Chain Disruptions & Geopolitical Risks | -0.4% | Global | Short Term |

| Intense Price Competition & Market Saturation | -0.3% | Developed Markets | Short to Medium Term |

| High Logistics and Distribution Costs in Remote Areas | -0.2% | Emerging Markets, Island Nations | Medium Term |

Mineral Water Market - Updated Report Scope

This report provides a comprehensive analysis of the global mineral water market, offering detailed insights into market dynamics, segmentation, and regional trends. It covers historical performance, current market size, and future projections, aiming to equip stakeholders with essential data for strategic decision-making. The scope encompasses an in-depth examination of key drivers, restraints, opportunities, and challenges influencing market evolution, along with a spotlight on the competitive landscape and the impact of emerging technologies like AI.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 45.0 billion |

| Market Forecast in 2033 | USD 86.7 billion |

| Growth Rate | 8.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Nestle Waters, Danone Waters, The Coca-Cola Company (Dasani, smartwater), PepsiCo (Aquafina), FIJI Water, Evian (Danone), Perrier (Nestle), San Pellegrino (Nestle), Nongfu Spring, KBL (Bisleri), Acqua Panna (Nestle), VOSS Water, Icelandic Glacial, Gerolsteiner Brunnen, Saratoga Spring Water, Himalayan Natural Mineral Water, Pocari Sweat (Otsuka Pharmaceutical), TY Nant, Mountain Valley Spring Water, Iskilde Mineral Water |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The mineral water market is comprehensively segmented to provide granular insights into its diverse components, allowing for a detailed understanding of consumer preferences, product characteristics, and distribution dynamics. These segmentations help in identifying niche markets, emerging product categories, and effective sales channels. The market can be dissected based on the type of mineral water, the materials used for packaging, the channels through which it reaches consumers, and its geographical origin, each offering unique growth opportunities and competitive landscapes.

Understanding these segments is crucial for market participants to tailor their strategies, from product development and branding to marketing and distribution. For instance, the demand for still versus sparkling mineral water varies significantly across regions, while the choice of packaging type directly correlates with environmental consciousness and convenience preferences. Similarly, the effectiveness of online retail versus traditional brick-and-mortar stores depends heavily on consumer behavior and infrastructure development in different territories.

- By Product Type:

- Still Mineral Water: Dominates the market due to its widespread acceptance and daily consumption.

- Sparkling Mineral Water: Gaining popularity as a healthy alternative to carbonated soft drinks.

- Functional Mineral Water: Infused with added benefits like vitamins, electrolytes, or specific minerals for targeted health outcomes.

- Flavored Mineral Water: Appeals to consumers seeking variety and a subtle taste without added sugars.

- By Packaging Type:

- PET Bottles: Most common due to cost-effectiveness and light weight, facing increasing sustainability scrutiny.

- Glass Bottles: Preferred for premium products and perceived purity, growing due to environmental concerns over plastic.

- Cans: Emerging as a sustainable and convenient option, particularly for sparkling and flavored variants.

- Other (Cartons, Pouches): Niche but growing segments for specific applications or environmental initiatives.

- By Distribution Channel:

- Retail Stores (Supermarkets, Hypermarkets, Convenience Stores): Traditional and dominant channel for mass market reach.

- Online Retail: Experiencing rapid growth due to convenience, home delivery services, and wider product availability.

- Foodservice/HORECA (Hotels, Restaurants, Cafes): Critical for premium brands and out-of-home consumption.

- Institutional Sales: Includes sales to offices, schools, and other organizations.

- By Source:

- Natural Spring Water: Sourced from underground formations where water flows naturally to the earth's surface.

- Artesian Water: Derived from a well that taps into a confined aquifer where the water level stands above the top of the aquifer.

- Mineral-Enriched Water: Purified water with added minerals to meet specific nutritional profiles or taste preferences.

Regional Highlights

- North America: This region is characterized by high consumption of bottled water, driven by a perception of tap water quality issues and a strong emphasis on health and wellness. The market is mature, with a significant presence of both domestic and international brands. Key trends include the growth of premium, functional, and flavored mineral water, as well as increasing consumer demand for sustainable packaging, particularly in the United States and Canada. Innovation in e-commerce and direct-to-consumer models is also a prominent feature.

- Europe: Europe represents a highly developed and diverse mineral water market, with strong regional preferences and a deep-rooted culture of mineral water consumption, especially in countries like France, Italy, and Germany. The market is driven by a strong heritage of natural spring waters, strict regulatory standards for mineral water classification, and growing consumer demand for natural products. Sustainability initiatives and the adoption of glass bottles and cans are particularly strong in this region due to stringent environmental regulations and consumer advocacy against plastic waste.

- Asia Pacific (APAC): APAC is the fastest-growing region for mineral water, primarily fueled by rapid urbanization, rising disposable incomes, and increasing awareness of safe drinking water, particularly in populous countries like China, India, and Indonesia. The perceived contamination of tap water in many urban areas also boosts demand. While traditional PET bottles dominate, there's a growing segment for premium and international brands. The region also presents significant opportunities for innovation in functional and flavored categories tailored to local tastes.

- Latin America: This region shows significant growth potential, driven by improving economic conditions, expanding middle-class populations, and concerns over municipal water quality in several countries. Brazil and Mexico are leading markets, with a growing demand for both basic and premium mineral water. The distribution landscape is evolving, with a mix of traditional retail and emerging e-commerce channels. Brand loyalty and local sourcing play an important role in consumer purchasing decisions.

- Middle East and Africa (MEA): The MEA region exhibits strong demand for bottled water due to hot climates, limited access to clean tap water in certain areas, and a growing expatriate population with preferences for international brands. Saudi Arabia, UAE, and South Africa are key markets. While price sensitivity exists, there is a developing segment for premium and imported mineral waters. Investments in local bottling plants and sustainable practices are emerging to address both demand and environmental concerns.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Mineral Water Market.- Nestle Waters

- Danone Waters

- The Coca-Cola Company

- PepsiCo

- FIJI Water

- Evian

- Perrier

- San Pellegrino

- Nongfu Spring

- KBL (Bisleri)

- Acqua Panna

- VOSS Water

- Icelandic Glacial

- Gerolsteiner Brunnen

- Saratoga Spring Water

- Himalayan Natural Mineral Water

- Pocari Sweat (Otsuka Pharmaceutical)

- TY Nant

- Mountain Valley Spring Water

- Iskilde Mineral Water

Frequently Asked Questions

Analyze common user questions about the Mineral Water market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is mineral water?

Mineral water is water sourced from an underground formation protected from contamination, containing naturally occurring dissolved solids, minerals, and trace elements that give it a distinctive taste and health benefits. It is bottled at the source and remains largely unaltered.

Is mineral water healthier than regular bottled water or tap water?

Mineral water contains naturally occurring minerals like calcium, magnesium, and potassium, which can contribute to daily nutrient intake. While tap water is generally safe, mineral water offers a specific mineral profile and purity that some consumers prefer for perceived health benefits and taste.

What are the primary factors driving the growth of the mineral water market?

Key drivers include increasing health consciousness, rising disposable incomes, urbanization, concerns over tap water quality, and continuous product innovation such as functional and flavored varieties. The shift towards natural and healthier beverage options is a significant catalyst.

How is the mineral water industry addressing environmental concerns?

The industry is increasingly focused on sustainability by investing in recycled PET (rPET), glass bottles, aluminum cans, and carton packaging. Companies are also exploring refillable systems and reducing plastic use through lightweighting bottles and optimizing logistics to minimize carbon footprint.

What are the main types of mineral water available in the market?

The main types include Still Mineral Water (non-carbonated), Sparkling Mineral Water (naturally carbonated or carbonated during bottling), Functional Mineral Water (with added vitamins or electrolytes), and Flavored Mineral Water (with natural essences).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted