Hydrogenated Oil Market

Hydrogenated Oil Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702220 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

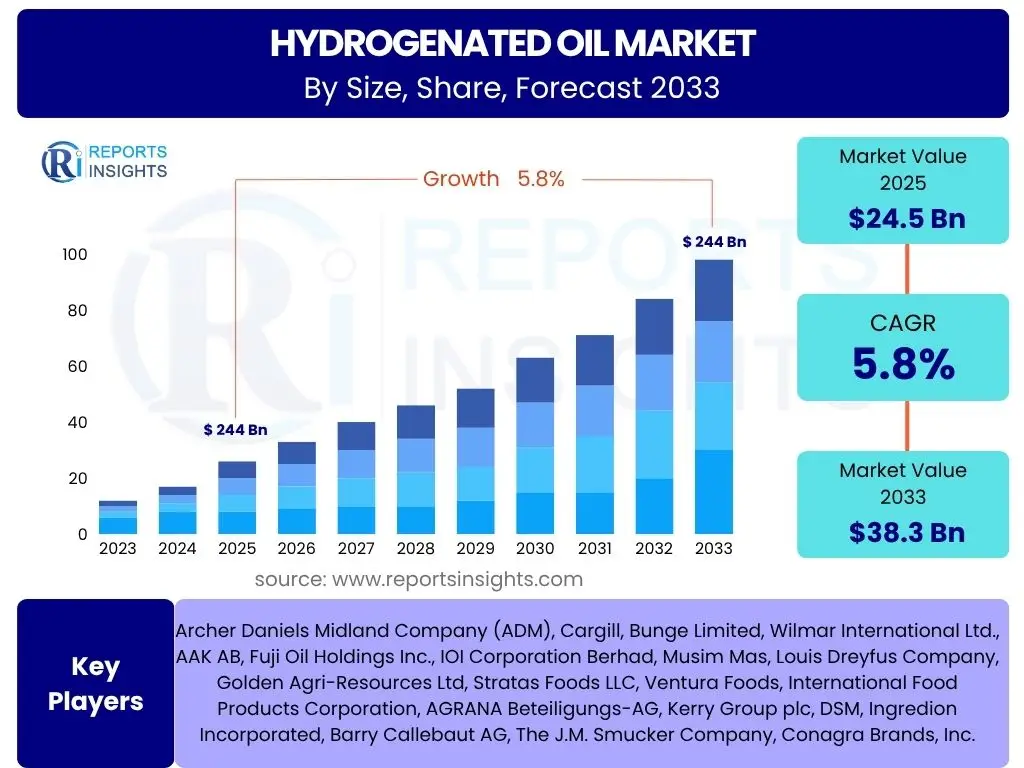

Hydrogenated Oil Market Size

According to Reports Insights Consulting Pvt Ltd, The Hydrogenated Oil Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 24.5 Billion in 2025 and is projected to reach USD 38.3 Billion by the end of the forecast period in 2033.

Key Hydrogenated Oil Market Trends & Insights

The hydrogenated oil market is undergoing a significant transformation driven by evolving consumer preferences, stringent regulatory frameworks, and advancements in processing technologies. A dominant trend involves the shift away from partially hydrogenated oils (PHOs) due to concerns over trans fat content, leading to increased demand for fully hydrogenated oils (FHOs) and alternatives that offer similar functional properties without the associated health risks. This regulatory pressure, particularly in developed economies, is reshaping product formulations across the food and beverage industry.

Furthermore, there is a growing emphasis on plant-based ingredients and sustainable sourcing practices, which influences the types of oils being hydrogenated and the supply chain dynamics. Innovation in enzymatic and interesterification processes provides manufacturers with methods to achieve desired texture and stability profiles while minimizing or eliminating trans fats. This technological evolution allows for the creation of healthier fat solutions, catering to both consumer demand for wellness-oriented products and industry needs for cost-effective and functionally superior ingredients.

Another emerging trend is the expansion of hydrogenated oils beyond traditional food applications into industrial sectors such as cosmetics, personal care, and biofuels. The versatility of these modified fats, offering benefits like improved shelf stability, emulsification, and specific melting points, makes them valuable components in a diverse range of non-food products. This diversification of application areas contributes to market resilience and opens new avenues for growth, offsetting some of the challenges faced in the food segment due to health perceptions.

- Transition towards Fully Hydrogenated Oils (FHOs) and non-PHO alternatives.

- Increased demand for plant-based and sustainably sourced oil ingredients.

- Technological advancements in enzymatic and interesterification processes.

- Expansion of hydrogenated oil applications in industrial sectors.

- Evolving regulatory landscape driving product reformulation.

AI Impact Analysis on Hydrogenated Oil

The integration of Artificial intelligence (AI) is set to significantly revolutionize various aspects of the hydrogenated oil industry, from raw material procurement to final product distribution. Manufacturers are increasingly exploring AI-driven solutions to optimize production processes, improve efficiency, and enhance product quality. AI algorithms can analyze vast datasets from supply chains, identifying patterns and predicting market fluctuations, thereby enabling more strategic purchasing of raw materials like palm, soybean, and rapeseed oils and mitigating price volatility.

In the production phase, AI's application extends to real-time process monitoring, predictive maintenance of machinery, and optimization of hydrogenation parameters. By analyzing sensor data, AI systems can fine-tune reaction conditions, ensuring consistent product quality, reducing energy consumption, and minimizing waste. This leads to higher yields and more cost-effective operations. Furthermore, AI-powered quality control systems can rapidly identify deviations in product specifications, such as fat composition or melting point, allowing for immediate corrective actions and ensuring compliance with stringent food safety and industrial standards.

Beyond manufacturing, AI is also impacting research and development efforts in the hydrogenated oil sector. Machine learning models can accelerate the discovery of novel fat formulations and alternative hydrogenation processes that offer improved functional properties or healthier profiles. By simulating molecular interactions and predicting material characteristics, AI can significantly shorten development cycles and reduce the need for extensive physical testing. This capability is crucial for companies looking to innovate and adapt quickly to evolving market demands for trans fat-free and sustainably produced fat solutions.

- Optimized raw material procurement and supply chain management through predictive analytics.

- Enhanced production efficiency and reduced energy consumption via real-time process monitoring.

- Improved product quality and consistency through AI-driven quality control and parameter optimization.

- Accelerated research and development of new fat formulations and hydrogenation technologies.

- Predictive maintenance for manufacturing equipment, minimizing downtime and operational costs.

Key Takeaways Hydrogenated Oil Market Size & Forecast

The hydrogenated oil market is poised for steady growth through 2033, driven by its indispensable role in the food processing, cosmetics, and industrial sectors, despite ongoing health and regulatory scrutiny. The forecasted expansion is largely attributed to the robust demand for processed foods globally, particularly in emerging economies where urbanization and changing dietary habits are prevalent. Furthermore, advancements in hydrogenation technologies that produce trans fat-free or low-trans fat alternatives are mitigating some of the previous health-related concerns, enabling market players to innovate and meet evolving consumer expectations.

A significant takeaway is the market's strategic pivot towards fully hydrogenated oils (FHOs) and interesterified fats, which offer the functional benefits of texture, stability, and shelf life without the presence of harmful trans fats found in partially hydrogenated oils (PHOs). This shift is not merely a response to regulatory mandates but also a proactive measure by manufacturers to align with consumer wellness trends and maintain market relevance. Companies are investing heavily in R&D to develop novel fat solutions that balance functionality, health, and sustainability, positioning the market for continued innovation.

The diversification of hydrogenated oil applications beyond the food industry, into sectors like personal care, oleochemicals, and biofuels, represents a crucial growth vector. This broad utility underscores the versatility of modified fats and creates new revenue streams, providing a buffer against potential saturation or stricter regulations in any single application area. Overall, the market's future will be characterized by sustained growth, driven by technological adaptation, focus on healthier formulations, and expansion into diverse industrial applications.

- Projected steady growth driven by diverse applications and technological advancements.

- Strategic shift towards trans fat-free and low-trans fat alternatives (FHOs and interesterified fats).

- Significant investments in R&D for healthier and more sustainable fat solutions.

- Expansion into non-food industries like cosmetics, oleochemicals, and biofuels.

- Market resilience despite regulatory pressures, fueled by innovation and adaptability.

Hydrogenated Oil Market Drivers Analysis

The hydrogenated oil market is propelled by a confluence of factors, primarily the persistent and increasing demand from the global food processing industry. Hydrogenated oils are critical ingredients in a wide array of products, including bakery goods, confectionery, snacks, and spreads, providing essential functional properties like texture, shelf life, and mouthfeel. As populations grow and urbanization accelerates, particularly in developing regions, the consumption of processed and convenience foods continues to rise, directly fueling the demand for these ingredients. The cost-effectiveness and versatility of hydrogenated oils compared to some alternative fats also contribute significantly to their continued adoption by food manufacturers.

Beyond the food sector, the expanding applications of hydrogenated oils in various industrial fields serve as a strong market driver. These oils are vital components in the production of oleochemicals, which are used in cosmetics, personal care products, soaps, detergents, and even lubricants and biofuels. The intrinsic properties of hydrogenated fats, such as their enhanced stability, increased melting points, and improved oxidative resistance, make them ideal for these non-food applications. This diversification of end-use industries provides a broader and more stable demand base for the hydrogenated oil market, reducing its sole reliance on the food sector.

Furthermore, technological advancements in hydrogenation processes, particularly the development of methods that produce trans fat-free or low-trans fat oils, are mitigating previous health concerns and boosting market acceptance. Innovations like enzymatic interesterification and improved catalytic hydrogenation allow manufacturers to create healthier fat alternatives that retain the desired functional characteristics. These advancements enable manufacturers to comply with stricter health regulations while still offering products that meet consumer expectations for taste and texture. This technological evolution makes hydrogenated oils a more viable and attractive option for formulators aiming to develop healthier product lines.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Processed Food Industry | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium Term (2025-2029) |

| Expanding Industrial Applications (Cosmetics, Biofuels, etc.) | +1.2% | North America, Europe, China, India | Medium to Long Term (2027-2033) |

| Technological Advancements for Trans Fat Reduction | +1.0% | Global, particularly North America, Europe | Short to Medium Term (2025-2030) |

| Cost-Effectiveness and Functional Versatility | +0.8% | Global | Ongoing |

Hydrogenated Oil Market Restraints Analysis

A primary restraint on the hydrogenated oil market is the persistent health concern associated with trans fatty acids (TFAs), particularly those found in partially hydrogenated oils (PHOs). Numerous health organizations and scientific studies have linked TFA consumption to an increased risk of cardiovascular diseases. This widespread public awareness has led to a negative perception of hydrogenated oils among health-conscious consumers, prompting them to seek out healthier alternatives and pushing food manufacturers to reformulate products to be trans fat-free. While fully hydrogenated oils do not contain trans fats, the lingering association with "hydrogenated" often creates consumer apprehension, impacting overall market growth potential.

Adding to this pressure are increasingly stringent government regulations and bans on trans fats in many countries. Governments and regulatory bodies worldwide, including the U.S. FDA, have taken decisive steps to limit or ban the use of PHOs in food products. Such regulations force food manufacturers to discontinue the use of PHOs and invest in research and development for alternative fat solutions, which can be costly and time-consuming. While these regulations are beneficial for public health, they pose a significant challenge for traditional hydrogenated oil producers who must adapt their production processes and product portfolios rapidly to remain compliant and competitive.

Furthermore, the growing competition from healthier fat alternatives, such as non-hydrogenated oils (e.g., olive oil, sunflower oil, canola oil), interesterified fats, and specially formulated blended oils, presents a considerable restraint. These alternatives often offer similar functional properties to hydrogenated oils but without the health drawbacks or regulatory hurdles. As consumer demand for "clean label" and naturally healthy ingredients increases, manufacturers are increasingly opting for these alternatives, thereby reducing the market share for hydrogenated oils. The higher cost of some of these alternative solutions, however, still positions hydrogenated oils as a cost-effective option for certain applications, but the trend clearly favors non-hydrogenated options where feasible.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Health Concerns Over Trans Fats | -1.5% | Global | Ongoing |

| Stringent Government Regulations and Bans | -1.2% | North America, Europe, Developed Asia Pacific | Short to Medium Term (2025-2030) |

| Competition from Healthier Fat Alternatives | -1.0% | Global | Medium to Long Term (2027-2033) |

| Raw Material Price Volatility | -0.7% | Global | Short Term (2025-2027) |

Hydrogenated Oil Market Opportunities Analysis

The hydrogenated oil market presents significant opportunities through the development and commercialization of trans fat-free and low-trans fat alternatives. With increasing global awareness of the health risks associated with trans fats and stringent regulatory mandates, there is a substantial demand for fats that offer the functional advantages of hydrogenation without the negative health implications. This has spurred innovation in fully hydrogenated oils (FHOs), which inherently contain minimal trans fats, and in interesterification processes that chemically modify fats to achieve desired properties without hydrogenation. Companies investing in these advanced techniques can tap into a growing market segment that prioritizes both product functionality and consumer health, leading to new product development and market penetration in health-conscious regions.

Another key opportunity lies in the expanding applications of hydrogenated oils within the burgeoning plant-based food sector. As consumer interest in vegan and vegetarian diets rises, there is a parallel demand for plant-based alternatives to traditional dairy and meat products. Hydrogenated vegetable oils are crucial ingredients in formulating plant-based butter, cheeses, creams, and meat substitutes, providing the necessary texture, mouthfeel, and stability. This niche but rapidly growing segment offers a fresh avenue for hydrogenated oil manufacturers to innovate and supply specialized fat solutions that cater to the unique requirements of plant-based food production, contributing to market diversification and sustained growth.

Furthermore, exploring and expanding the use of hydrogenated oils in diverse non-food industrial applications represents a lucrative opportunity. Beyond traditional uses in soaps and cosmetics, there is increasing potential in sectors such as sustainable biofuels, lubricants, and specialized oleochemicals. The unique physical and chemical properties of hydrogenated fats, such as their high oxidative stability and varying melting points, make them ideal candidates for advanced industrial formulations. Investing in R&D to tailor hydrogenated oils for these high-value industrial uses can open new revenue streams, reduce reliance on the food sector, and contribute to the development of more sustainable industrial practices, driving long-term market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Trans Fat-Free Alternatives (e.g., FHOs, Interesterified Fats) | +1.8% | Global, especially Developed Markets | Short to Medium Term (2025-2030) |

| Growth in Plant-Based Food Sector | +1.5% | North America, Europe, Asia Pacific | Medium to Long Term (2027-2033) |

| Expansion into New Industrial Applications (Biofuels, Lubricants) | +1.2% | Global | Medium to Long Term (2028-2033) |

| Emerging Markets with Rising Disposable Incomes | +1.0% | Asia Pacific, Latin America, Africa | Short to Medium Term (2025-2030) |

Hydrogenated Oil Market Challenges Impact Analysis

The hydrogenated oil market faces significant challenges, primarily stemming from the pervasive negative perception associated with the term "hydrogenated oil" due to its historical link with trans fats. Despite technological advancements that allow for the production of trans fat-free fully hydrogenated oils (FHOs), the general public often conflates all hydrogenated products with unhealthy trans fats. This negative connotation impacts consumer willingness to purchase products containing these ingredients and puts pressure on food manufacturers to find alternative fat solutions or to adopt "clean label" strategies that avoid ingredients perceived as unhealthy, regardless of their current formulation. Overcoming this deep-seated negative perception requires extensive public education and industry-wide efforts to clearly differentiate modern, healthier hydrogenated oil products.

Another critical challenge is the evolving and increasingly stringent regulatory landscape concerning trans fat content in food products. Governments worldwide are implementing bans or strict limitations on partially hydrogenated oils (PHOs), which were historically the main source of dietary trans fats. While these regulations aim to improve public health, they necessitate significant reformulation efforts and investment from hydrogenated oil producers and food manufacturers. Compliance can be costly, requiring new processing equipment, R&D into alternative ingredients, and sometimes leading to product discontinuation if reformulation is not feasible or economically viable. The varying nature of regulations across different regions also complicates global trade and market access for companies operating internationally.

Sourcing sustainable and ethically produced raw materials also poses a substantial challenge for the hydrogenated oil market. Many hydrogenated oils are derived from palm oil, a commodity frequently associated with deforestation, habitat destruction, and social issues in producing regions. Growing consumer and corporate demand for sustainably sourced ingredients puts pressure on manufacturers to ensure their supply chains are transparent and adhere to environmental and social standards. Achieving sustainable certification (e.g., RSPO) for large volumes of palm oil can be complex and expensive, while shifting to alternative oil sources may impact cost-effectiveness and product functionality. Balancing economic viability, functional requirements, and sustainability mandates is a continuous hurdle for market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative Consumer Perception and Branding Issues | -1.3% | Global | Ongoing |

| Complex and Varied Regulatory Compliance | -1.0% | Global, particularly major economies | Short to Medium Term (2025-2030) |

| Sourcing Sustainable and Ethical Raw Materials | -0.8% | Global, especially Southeast Asia (Palm Oil) | Medium to Long Term (2027-2033) |

| High Investment in R&D for Alternatives | -0.6% | Global | Short to Medium Term (2025-2029) |

Hydrogenated Oil Market - Updated Report Scope

This comprehensive market research report provides a detailed analysis of the global Hydrogenated Oil Market, offering insights into its current size, historical performance, and future growth projections. The scope encompasses a thorough examination of market trends, key drivers, restraints, opportunities, and challenges influencing the industry landscape. It delves into the impact of technological advancements, particularly AI, and regulatory changes on market dynamics. The report further segments the market by type, source, and application, providing granular insights into each segment's contribution and growth potential. Regional analyses offer a nuanced understanding of market characteristics across major geographies, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Key players in the market are profiled to provide a competitive landscape overview, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 24.5 Billion |

| Market Forecast in 2033 | USD 38.3 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Archer Daniels Midland Company (ADM), Cargill, Bunge Limited, Wilmar International Ltd., AAK AB, Fuji Oil Holdings Inc., IOI Corporation Berhad, Musim Mas, Louis Dreyfus Company, Golden Agri-Resources Ltd, Stratas Foods LLC, Ventura Foods, International Food Products Corporation, AGRANA Beteiligungs-AG, Kerry Group plc, DSM, Ingredion Incorporated, Barry Callebaut AG, The J.M. Smucker Company, Conagra Brands, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The hydrogenated oil market is meticulously segmented to provide a comprehensive understanding of its diverse components and their respective market dynamics. This segmentation facilitates detailed analysis of consumer preferences, technological adaptations, and regional influences. The primary segmentation categories include analysis by Type, which distinguishes between Partially Hydrogenated Oils (PHO) and Fully Hydrogenated Oils (FHO), reflecting the industry's shift away from trans fat-containing products. PHOs have faced significant regulatory challenges and declining adoption, while FHOs are gaining traction due to their trans fat-free nature and functional benefits. This distinction is crucial for understanding current market composition and future growth trajectories.

Further segmentation by Source highlights the various raw materials used for hydrogenation, such as Palm Oil, Soybean Oil, Rapeseed Oil, Sunflower Oil, Coconut Oil, Corn Oil, Cottonseed Oil, and Others. The availability, cost-effectiveness, and sustainability profiles of these raw materials significantly influence their utilization in different regions. For instance, palm oil and soybean oil are dominant sources globally due to their abundant supply and versatile properties, but sourcing concerns often lead to increased demand for sustainably certified options or alternatives. This segmentation helps identify supply chain vulnerabilities and opportunities for diversification.

The market is also segmented by Application, differentiating between Food & Beverages and Industrial uses. The Food & Beverages segment is further sub-segmented into Bakery & Confectionery, Snacks & Savory, Spreads & Dressings, Dairy & Desserts, and Others, illustrating the broad utility of hydrogenated oils in processed foods. The Industrial segment encompasses Cosmetics & Personal Care, Soaps & Detergents, Biofuels, Lubricants & Greases, and Other industrial applications, underscoring the expanding utility of these modified fats beyond the culinary realm. Each application area has unique requirements for fat functionality, driving innovation in specific hydrogenated oil formulations. This multi-layered segmentation provides a granular view of the market's structure and growth opportunities across various end-use sectors.

- By Type:

- Partially Hydrogenated Oil (PHO)

- Fully Hydrogenated Oil (FHO)

- By Source:

- Palm Oil

- Soybean Oil

- Rapeseed Oil

- Sunflower Oil

- Coconut Oil

- Corn Oil

- Cottonseed Oil

- Others

- By Application:

- Food & Beverages

- Bakery & Confectionery

- Snacks & Savory

- Spreads & Dressings

- Dairy & Desserts

- Others

- Industrial

- Cosmetics & Personal Care

- Soaps & Detergents

- Biofuels

- Lubricants & Greases

- Others

- Food & Beverages

- By Geography:

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, UK, Italy, Spain, Rest of Europe)

- Asia Pacific (China, Japan, India, South Korea, Southeast Asia, Australia & New Zealand, Rest of Asia Pacific)

- South America (Brazil, Argentina, Rest of South America)

- Middle East & Africa (GCC Countries, South Africa, Rest of MEA)

Regional Highlights

- Asia Pacific: Emerging as the largest and fastest-growing market for hydrogenated oils, driven by rapid urbanization, increasing disposable incomes, and a burgeoning processed food industry. Countries like China and India exhibit high consumption due to their vast populations and evolving dietary habits, with significant demand for bakery, confectionery, and convenience foods.

- North America: A mature market characterized by stringent regulations regarding trans fats, leading to a strong shift towards trans fat-free fully hydrogenated oils and interesterified fats. Innovation in healthier fat solutions and a robust industrial sector for cosmetics and biofuels contribute to its steady market value.

- Europe: Facing strict regulatory environments and high consumer awareness regarding healthy eating, this region is a leader in adopting advanced fat modification technologies to produce trans fat-free alternatives. The demand is stable, with a focus on sustainable sourcing and clean label products.

- Latin America: Experiencing consistent growth, particularly in Brazil and Argentina, fueled by expanding food processing sectors and increasing demand for convenience foods. Economic development and rising middle-class populations are driving consumption, with a growing focus on meeting international health standards.

- Middle East & Africa (MEA): Showing nascent but promising growth, influenced by expanding food industries, population growth, and increasing Westernization of diets. Demand for convenience foods and imported processed products is driving the need for hydrogenated oils, with growing awareness of product safety and quality.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Hydrogenated Oil Market.- Archer Daniels Midland Company (ADM)

- Cargill

- Bunge Limited

- Wilmar International Ltd.

- AAK AB

- Fuji Oil Holdings Inc.

- IOI Corporation Berhad

- Musim Mas

- Louis Dreyfus Company

- Golden Agri-Resources Ltd

- Stratas Foods LLC

- Ventura Foods

- International Food Products Corporation

- AGRANA Beteiligungs-AG

- Kerry Group plc

- DSM

- Ingredion Incorporated

- Barry Callebaut AG

- The J.M. Smucker Company

- Conagra Brands, Inc.

Frequently Asked Questions

What is hydrogenated oil and why is it used?

Hydrogenated oil is vegetable oil that has undergone a chemical process called hydrogenation, where hydrogen atoms are added to unsaturated fatty acids. This process solidifies the oil, increases its shelf life, and provides desirable textures and mouthfeel in food products, such as crispiness in snacks and creaminess in spreads. It is also used extensively in industrial applications for its stability and physical properties.

What are the primary applications of hydrogenated oil?

Hydrogenated oils are primarily used in the food and beverage industry for products like bakery items (biscuits, cakes), confectionery (chocolates, candies), snacks, spreads (margarine), and processed dairy alternatives. Industrially, they are key ingredients in cosmetics, personal care products, soaps, detergents, lubricants, and increasingly, in the production of sustainable biofuels.

Are hydrogenated oils safe to consume?

The safety of hydrogenated oils depends on their type. Partially hydrogenated oils (PHOs) contain trans fats, which are scientifically linked to increased risk of heart disease and are largely banned in many countries. Fully hydrogenated oils (FHOs), however, contain minimal to no trans fats and are considered safe for consumption by regulatory bodies. The industry is rapidly shifting towards FHOs and other trans fat-free alternatives.

How do regulations impact the hydrogenated oil market?

Regulations, particularly concerning trans fat content, significantly impact the market by phasing out or banning partially hydrogenated oils (PHOs). This forces manufacturers to reformulate products using trans fat-free alternatives like fully hydrogenated oils (FHOs) or interesterified fats. These regulations drive innovation and shape product development, ensuring compliance and addressing public health concerns.

What are the key trends in the hydrogenated oil market?

Key trends include a strong shift towards trans fat-free solutions (like fully hydrogenated oils and interesterified fats), increased demand from the plant-based food sector for texture and stability, diversification of applications into non-food industries such as cosmetics and biofuels, and a growing emphasis on sustainable sourcing of raw materials. Technological advancements are also enabling more efficient and healthier hydrogenation processes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted