Oil and Gas Pipeline Market

Oil and Gas Pipeline Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700063 | Last Updated : July 22, 2025 |

Format : ![]()

![]()

![]()

![]()

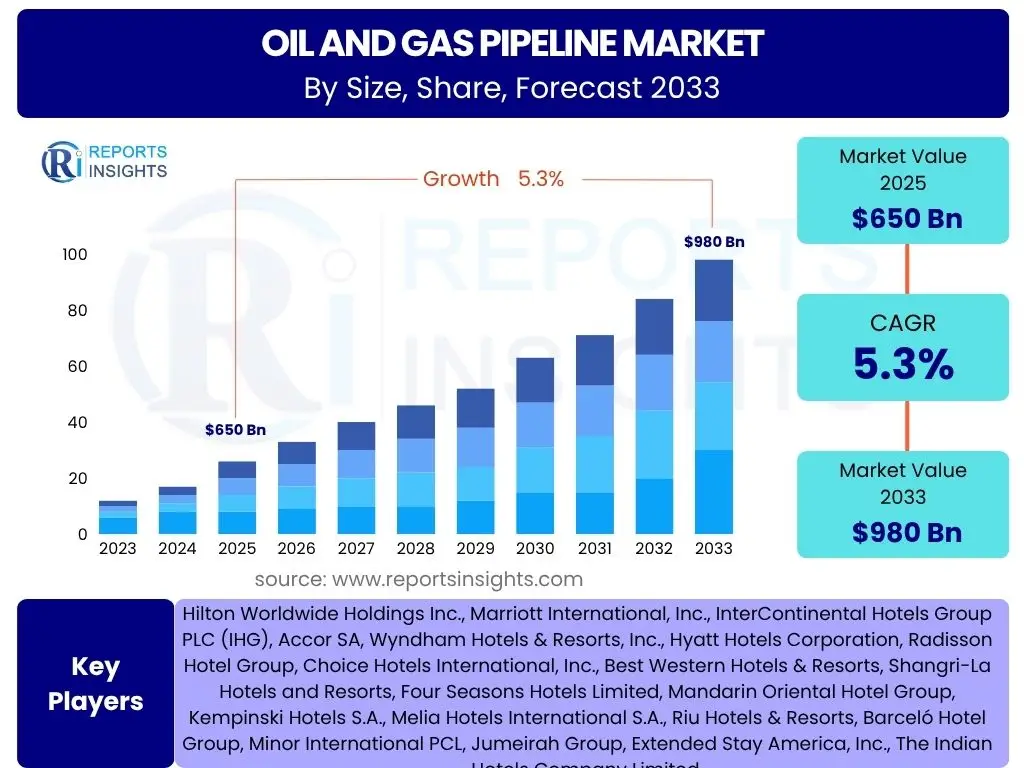

Oil and Gas Pipeline Market is projected to grow at a Compound annual growth rate (CAGR) of 5.25% between 2025 and 2033, valued at USD 650 billion in 2025 and is projected to grow to USD 980 billion by 2033 at the end of the forecast period.

Key Oil and Gas Pipeline Market Trends & Insights

The global oil and gas pipeline market is undergoing significant transformations driven by a confluence of technological advancements, evolving energy demands, and stringent regulatory frameworks. Key trends indicate a strategic pivot towards enhancing operational efficiency, ensuring safety, and integrating sustainable practices across the pipeline infrastructure. The industry is witnessing increased investments in digital technologies to optimize asset performance and mitigate risks. Furthermore, the imperative for energy security continues to fuel cross-border pipeline projects, while environmental concerns are accelerating the adoption of cleaner technologies and materials. These shifts are shaping the future trajectory of crude oil, refined products, and natural gas transportation.

The market's dynamic nature is further influenced by geopolitical developments and the global push for decarbonization. This has led to a dual focus: expanding essential infrastructure to meet immediate energy needs, particularly in developing economies, and simultaneously exploring pathways for transporting alternative energy carriers like hydrogen or CO2. The emphasis on pipeline integrity management, through advanced inspection and monitoring techniques, remains paramount to prevent leaks and ensure reliable supply. Moreover, the industry is keen on attracting and retaining a skilled workforce, addressing potential labor shortages that could impact project execution and maintenance. These multifaceted trends collectively define the present and future landscape of the oil and gas pipeline sector.

- Increased adoption of digital twins and predictive maintenance analytics.

- Growing investments in carbon capture, utilization, and storage (CCUS) infrastructure.

- Rising demand for hydrogen-ready pipelines and repurposing of existing assets.

- Emphasis on enhanced pipeline integrity management and leak detection systems.

- Development of smart pipeline networks incorporating IoT and automation.

- Strict environmental regulations driving sustainable construction and operation practices.

- Geopolitical factors influencing routing and security of critical energy corridors.

AI Impact Analysis on Oil and Gas Pipeline

Artificial intelligence (AI) is rapidly emerging as a transformative force within the oil and gas pipeline sector, fundamentally reshaping how these critical infrastructures are designed, operated, and maintained. AI-driven solutions offer unprecedented capabilities for predictive analytics, enabling operators to anticipate equipment failures, optimize maintenance schedules, and enhance overall operational efficiency. By processing vast amounts of sensor data, AI algorithms can identify subtle anomalies that might indicate potential issues, thereby significantly reducing the risk of costly downtime and environmental incidents. This proactive approach to asset management is vital for ensuring the continuous and safe transport of hydrocarbons.

The application of AI extends beyond operational efficiency to encompass enhanced safety and security protocols. AI-powered surveillance systems can detect unauthorized intrusions or suspicious activities along pipeline routes, providing real-time alerts to security personnel. Furthermore, AI contributes to environmental stewardship by improving leak detection accuracy and speed, minimizing the impact of spills. The technology also plays a crucial role in optimizing energy consumption for pumping stations and compressing facilities, leading to reduced operational costs and a lower carbon footprint. As the industry increasingly embraces digitalization, AI is set to become an indispensable tool for maximizing performance, ensuring integrity, and navigating the complexities of modern energy transportation.

- Predictive maintenance for critical pipeline assets, minimizing downtime.

- Enhanced leak detection and anomaly identification through advanced analytics.

- Optimization of pipeline flow rates and energy consumption for pumping.

- AI-driven risk assessment and integrity management for aging infrastructure.

- Automation of inspection processes using drones and robotic systems with AI vision.

- Improved security monitoring and threat detection along pipeline routes.

- Data-driven decision-making for capacity planning and network optimization.

Key Takeaways Oil and Gas Pipeline Market Size & Forecast

- The global oil and gas pipeline market is projected for substantial expansion, reaching USD 980 billion by 2033.

- Growth is primarily driven by increasing global energy demand and the need for reliable energy transportation.

- The market is expected to exhibit a Compound Annual Growth Rate (CAGR) of 5.25% from 2025 to 2033.

- Major revenue contributions are anticipated from new pipeline construction projects, particularly in emerging economies.

- Significant investment is also directed towards maintenance, upgrade, and expansion of existing pipeline networks.

- Natural gas pipelines are foreseen to witness higher growth rates compared to crude oil pipelines, reflecting the energy transition.

- Technological advancements in pipeline monitoring, safety, and integrity management will bolster market value.

Oil and Gas Pipeline Market Drivers Analysis

The oil and gas pipeline market is propelled by several fundamental drivers that underscore its critical role in the global energy ecosystem. Foremost among these is the persistent and growing global energy demand, especially from rapidly industrializing economies. As populations expand and living standards rise, the need for reliable and efficient transportation of crude oil, natural gas, and refined products intensifies. Pipelines offer the most cost-effective and secure method for long-distance bulk transportation of these vital energy resources, making them indispensable to economic growth and energy security strategies worldwide.

Furthermore, significant investments in new upstream exploration and production activities across various regions necessitate robust midstream infrastructure to bring these resources to market. This includes the development of unconventional oil and gas fields, such as shale gas and oil sands, which often require extensive pipeline networks to connect remote production sites to processing facilities and consumption centers. Technological advancements in pipeline construction materials, monitoring systems, and integrity management solutions also contribute to market expansion by enhancing the safety, efficiency, and longevity of pipeline assets. These innovations make pipeline projects more feasible and attractive to investors, despite their substantial capital requirements. The confluence of these factors creates a strong demand environment for pipeline development and maintenance services globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Energy Demand | +1.5% | Asia Pacific, North America, Middle East | Long-term (2025-2033) |

| Expansion of Upstream Oil and Gas Production | +1.2% | North America (Shale), Middle East, Africa | Medium-term (2025-2030) |

| Emphasis on Energy Security and Supply Reliability | +1.0% | Europe, Asia Pacific, North America | Medium-term to Long-term |

| Technological Advancements in Pipeline Infrastructure | +0.8% | Global, particularly developed regions | Short-term to Long-term |

| Inter-regional Gas Pipeline Projects | +0.7% | Europe, Asia, Africa | Medium-term |

Oil and Gas Pipeline Market Restraints Analysis

Despite robust growth drivers, the oil and gas pipeline market faces several significant restraints that could temper its expansion. Environmental regulations and increasing public opposition represent a primary hurdle. Growing awareness regarding climate change and the environmental impact of fossil fuels has led to more stringent permitting processes, legal challenges, and heightened scrutiny for new pipeline projects. Activist groups and local communities often resist new constructions, leading to project delays, increased costs, or outright cancellations. This "social license to operate" is becoming increasingly difficult to obtain, particularly in regions with strong environmental advocacy.

High capital expenditure and complex financing structures also pose considerable restraints. Pipeline projects are inherently large-scale infrastructure undertakings requiring massive upfront investments, often running into billions of dollars. Securing adequate financing can be challenging, especially in a volatile economic climate where investor confidence in fossil fuel projects might waver due to energy transition policies. Furthermore, geopolitical risks, including political instability, cross-border disputes, and trade sanctions, can significantly impact the feasibility and operational continuity of international pipeline projects. These factors introduce unpredictability and elevate the risk profile for investors and operators, making project development more complex and sometimes less attractive.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations and Opposition | -0.8% | North America, Europe, parts of Asia Pacific | Long-term |

| High Capital Expenditure and Project Financing Challenges | -0.7% | Global | Medium-term to Long-term |

| Geopolitical Instability and Cross-border Conflicts | -0.6% | Eastern Europe, Middle East, Africa | Short-term to Medium-term |

| Volatility of Oil and Gas Prices | -0.5% | Global | Short-term |

| Competition from Renewable Energy Sources | -0.4% | Europe, North America | Long-term |

Oil and Gas Pipeline Market Opportunities Analysis

The oil and gas pipeline market, despite its challenges, presents several compelling opportunities for growth and innovation. One significant area is the increasing interest in repurposing existing natural gas pipelines for hydrogen transportation or developing dedicated hydrogen pipeline infrastructure. As the world transitions towards a hydrogen economy, the extensive network of pipelines offers a cost-effective solution for distributing this clean energy carrier. This represents a long-term strategic shift that could revitalize pipeline investments and diversify revenue streams for operators. Furthermore, the burgeoning Carbon Capture, Utilization, and Storage (CCUS) sector creates demand for new pipelines designed to transport captured CO2 to storage sites, offering a crucial pathway for decarbonization efforts within heavy industries.

Another substantial opportunity lies in the digitalization and automation of pipeline operations. The integration of advanced technologies such as IoT sensors, artificial intelligence, machine learning, and digital twins can dramatically enhance operational efficiency, reduce maintenance costs, improve safety, and provide real-time data for better decision-making. These technological advancements enable predictive maintenance, faster leak detection, and optimized flow management, which are critical for maximizing asset utilization and minimizing environmental impact. Moreover, expanding pipeline networks in developing regions, particularly in Asia Pacific and Africa, to support their rapidly growing energy consumption and new resource discoveries, provides conventional growth avenues. These regions often lack extensive pipeline infrastructure, necessitating significant investments to connect production areas with demand centers, thereby fostering new construction projects and service opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Hydrogen Transportation Infrastructure | +0.9% | Europe, North America, Asia Pacific | Long-term |

| Growth in Carbon Capture, Utilization, and Storage (CCUS) Projects | +0.8% | North America, Europe, Middle East | Medium-term to Long-term |

| Digitalization and Smart Pipeline Technologies Adoption | +0.7% | Global | Short-term to Long-term |

| Expansion in Emerging Economies (Africa, Asia Pacific) | +0.6% | Asia Pacific, Africa, Latin America | Medium-term |

| Upgrades and Maintenance of Aging Infrastructure | +0.5% | North America, Europe, Russia | Ongoing |

Oil and Gas Pipeline Market Challenges Impact Analysis

The oil and gas pipeline market confronts a range of critical challenges that demand robust strategic responses from industry stakeholders. Cybersecurity threats pose an increasingly severe risk, with digitalized pipeline operations becoming vulnerable to sophisticated attacks that could disrupt supply, cause environmental damage, or compromise critical infrastructure. Protecting operational technology (OT) systems and ensuring data integrity is a continuous and evolving battle for pipeline operators. Furthermore, the inherent complexity and high cost associated with obtaining permits and rights-of-way for new pipeline projects can significantly impede development. Navigating diverse regulatory landscapes, environmental assessments, and securing landowner agreements often lead to protracted timelines and escalating project costs, acting as major deterrents to investment.

Another significant challenge is managing the extensive and often aging existing pipeline infrastructure. A substantial portion of global pipelines was constructed decades ago, requiring continuous inspection, maintenance, and rehabilitation to ensure integrity and prevent failures. This involves significant operational expenditure and specialized expertise. Additionally, the industry faces a growing shortage of skilled labor, particularly in specialized fields such as welding, pipeline inspection, and integrity management, which can impact project execution efficiency and the ability to maintain current infrastructure. Lastly, social license to operate continues to be a formidable challenge, as public and political opposition to fossil fuel infrastructure often translates into project delays and increased litigation, requiring companies to invest heavily in stakeholder engagement and community relations to gain acceptance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Threats to Critical Infrastructure | -0.6% | Global | Ongoing |

| Complex Permitting and Right-of-Way Acquisition | -0.5% | North America, Europe, South Asia | Long-term |

| Aging Infrastructure and Integrity Management | -0.4% | North America, Europe, Russia | Ongoing |

| Skilled Labor Shortage and Workforce Development | -0.3% | Global | Medium-term |

| Public and Political Opposition to New Projects | -0.3% | North America, Europe | Long-term |

Oil and Gas Pipeline Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global oil and gas pipeline market, offering strategic insights into its growth trajectory, key segments, and competitive landscape. The report meticulously examines historical data, current market dynamics, and future projections to provide a holistic understanding of the industry's evolution. It covers essential market attributes, including size, growth rate, and influential trends, empowering stakeholders with the necessary intelligence for informed decision-making. The scope also encompasses a detailed review of market drivers, restraints, opportunities, and challenges, providing a balanced perspective on the forces shaping the market. Furthermore, the report delves into regional performance and profiles leading companies, offering a complete picture of the market's structure and competitive intensity.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 650 Billion |

| Market Forecast in 2033 | USD 980 Billion |

| Growth Rate | 5.25% (2025 to 2033) |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | TransCanada Corporation, Enbridge Inc., Kinder Morgan Inc., GAIL (India) Limited, TC Energy Corporation, Gazprom, China National Petroleum Corporation (CNPC), National Oilwell Varco (NOV), Baker Hughes, Siemens Energy AG, Wood Group, Saipem S.p.A., TechnipFMC plc, Emerson Electric Co., Perma-Pipe International Holdings Inc., Shawcor Ltd., Tenaris S.A., Vallourec S.A., Wasco Energy, DNV GL |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

:The oil and gas pipeline market is meticulously segmented to provide a detailed understanding of its diverse components and sub-sectors, enabling a granular analysis of market dynamics across various dimensions. This segmentation helps identify specific growth areas, operational nuances, and strategic opportunities within the broader pipeline industry. Each segment represents a critical aspect of how oil and gas are transported and managed globally, reflecting different operational characteristics, material requirements, and application contexts. Understanding these distinct segments is crucial for stakeholders to tailor their strategies and investments effectively, ensuring alignment with market demand and technological advancements. The structured breakdown allows for targeted analysis of market trends, competitive landscapes, and regulatory impacts specific to each category.

The market is primarily divided by the type of fluid transported, operational environment, application, materials used in construction, and the services rendered throughout the pipeline lifecycle. These categorizations provide a comprehensive framework for assessing market size, growth rates, and key influences on each segment. For instance, the distinction between crude oil, natural gas, and refined products pipelines highlights varied demands and infrastructure requirements. Similarly, separating onshore from offshore operations sheds light on distinct technological and environmental challenges. Analyzing these segments not only clarifies market structure but also reveals opportunities for specialization, innovation, and strategic partnerships, guiding business development and market penetration efforts across the globe. Each segment's unique characteristics contribute to the overall complexity and potential of the oil and gas pipeline market.

- By Type: This segment differentiates pipelines based on the primary commodity they transport, directly impacting design, safety standards, and operational considerations.

- Crude Oil Pipeline: Infrastructure designed for the bulk transportation of unrefined petroleum from production sites to refineries.

- Natural Gas Pipeline: Networks dedicated to moving natural gas from processing plants to distribution centers or end-users.

- Refined Products Pipeline: Systems for transporting processed petroleum products, such as gasoline, diesel, and jet fuel, from refineries to distribution terminals.

- By Operation Type: This segment distinguishes pipelines based on their geographical and environmental installation, influencing construction methods and maintenance challenges.

- Onshore Pipelines: Pipelines laid on land, typically requiring extensive land rights acquisition and environmental impact assessments.

- Offshore Pipelines: Subsea pipelines used to transport oil and gas from offshore production platforms to land-based facilities.

- By Application: This segment categorizes pipelines based on their ultimate functional purpose within the energy supply chain.

- Transportation: Long-distance, high-capacity pipelines connecting major production basins to consumption centers or export terminals.

- Distribution: Smaller, localized networks that deliver natural gas or refined products from main transmission lines to end-consumers.

- By Material: This segment focuses on the primary materials used in pipeline construction, impacting durability, cost, and suitability for various environments.

- Steel Pipelines: Predominantly used due to their strength, durability, and cost-effectiveness; includes carbon steel and alloy steel.

- Composite Pipelines: Newer materials offering corrosion resistance and flexibility, often used in specific applications or challenging environments.

- Other Materials: Includes High-Density Polyethylene (HDPE) for smaller distribution lines and specialized applications.

- By Service: This segment encompasses the various services required throughout the lifecycle of a pipeline, from initial setup to ongoing management.

- Construction & Installation: Activities involved in the physical building and laying of new pipeline infrastructure.

- Maintenance & Repair: Services aimed at ensuring the ongoing operational integrity and safety of existing pipelines, including corrective and preventive actions.

- Integrity Management: Proactive measures and programs to assess, monitor, and mitigate risks to pipeline safety and reliability.

- Surveillance & Monitoring: Technologies and methods used to continuously oversee pipeline operations, detect anomalies, and prevent incidents.

- Consulting & Engineering: Professional services providing expertise in design, planning, regulatory compliance, and project management for pipeline projects.

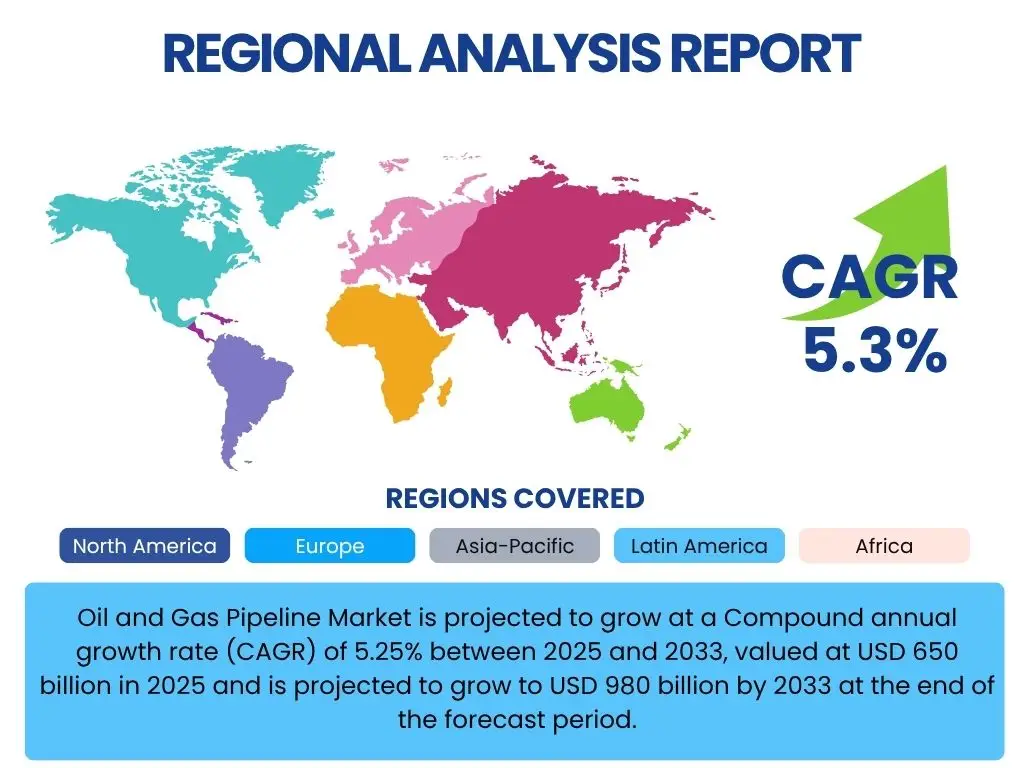

Regional Highlights

The global oil and gas pipeline market exhibits diverse growth dynamics across various regions, influenced by a combination of energy demand, geopolitical factors, infrastructure development, and regulatory environments. Each major region contributes uniquely to the market's overall trajectory, showcasing distinct opportunities and challenges.

- North America: This region remains a dominant market, primarily driven by extensive shale oil and gas production in the United States and Canada. The need for new takeaway capacityfrom prolific basins, coupled with significant investments in upgrading aging infrastructure and improving pipeline integrity, makes it a critical hub. The focus is on expanding interstate natural gas transmission and crude oil lines, alongside increasing adoption of advanced monitoring technologies and addressing environmental concerns.

- Asia Pacific (APAC): Expected to be the fastest-growing region, APAC is characterized by surging energy demand from industrialization and urbanization, particularly in China, India, and Southeast Asian countries. This growth necessitates substantial investments in new pipeline networks for importing natural gas and transporting domestic production. Cross-border pipeline projects aimed at enhancing energy security and regional connectivity are also key drivers.

- Europe: The European market is mature but focuses heavily on modernization, integrity management, and the repurposing of existing infrastructure for future energy carriers like hydrogen and CO2. While new large-scale crude oil pipeline projects are less common, the region invests significantly in natural gas import routes and domestic distribution networks, influenced by energy transition policies and geopolitical considerations.

- Middle East and Africa (MEA): This region is crucial due to its vast hydrocarbon reserves and export-oriented production. Pipeline development in the Middle East is primarily driven by expanding export capabilities for crude oil and LNG, and internal distribution for growing domestic energy consumption. In Africa, new discoveries of oil and gas, particularly in East and West Africa, are fueling demand for associated pipeline infrastructure to bring these resources to market, alongside efforts to improve energy access.

- Latin America: The market in Latin America is shaped by new oil and gas discoveries, particularly in Brazil (pre-salt) and Argentina (shale), as well as by efforts to integrate regional energy markets. Pipeline projects are often linked to increasing production capacities and improving intra-regional energy trade, though economic volatility and political stability can influence investment timelines.

Top Key Players:

The market research report covers the analysis of key stake holders of the Oil and Gas Pipeline Market. Some of the leading players profiled in the report include -:- TransCanada Corporation

- Enbridge Inc.

- Kinder Morgan Inc.

- GAIL (India) Limited

- TC Energy Corporation

- Gazprom

- China National Petroleum Corporation (CNPC)

- National Oilwell Varco

- Baker Hughes

- Siemens Energy AG

- Wood Group

- Saipem S.p.A.

- TechnipFMC plc

- Emerson Electric Co.

- Perma-Pipe International Holdings Inc.

- Shawcor Ltd.

- Tenaris S.A.

- Vallourec S.A.

- Wasco Energy

- DNV GL

Frequently Asked Questions:

What is the projected growth rate for the Oil and Gas Pipeline Market?

The Oil and Gas Pipeline Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.25% between 2025 and 2033. This growth is driven by increasing global energy demand, expanding upstream production, and the critical need for secure and efficient energy transportation infrastructure worldwide.

What key factors are driving the growth of the Oil and Gas Pipeline Market?

Key drivers include the rising global energy demand, significant investments in new upstream oil and gas exploration and production, the imperative for energy security and supply reliability across regions, and continuous technological advancements in pipeline materials and operational management systems that enhance efficiency and safety.

How does AI impact the Oil and Gas Pipeline sector?

Artificial intelligence significantly impacts the Oil and Gas Pipeline sector by enabling predictive maintenance for assets, enhancing leak detection capabilities, optimizing pipeline flow and energy consumption, improving security monitoring, and facilitating data-driven decision-making for integrity management and capacity planning. AI contributes to greater operational efficiency, safety, and reduced environmental impact.

What are the major challenges faced by the Oil and Gas Pipeline Market?

Major challenges include the escalating threat of cybersecurity attacks on critical infrastructure, complex and lengthy permitting processes compounded by environmental regulations, the ongoing need to manage and upgrade aging pipeline infrastructure, a growing shortage of skilled labor, and increasing public and political opposition to new fossil fuel projects.

What emerging opportunities exist in the Oil and Gas Pipeline Market?

Significant opportunities are emerging from the development of hydrogen transportation infrastructure (including repurposing existing pipelines), the growth in Carbon Capture, Utilization, and Storage (CCUS) projects, increasing adoption of digitalization and smart pipeline technologies for enhanced operations, and expansion into rapidly industrializing emerging economies in Asia Pacific and Africa to meet their rising energy consumption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted