Magnetron Market

Magnetron Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706643 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Magnetron Market Size

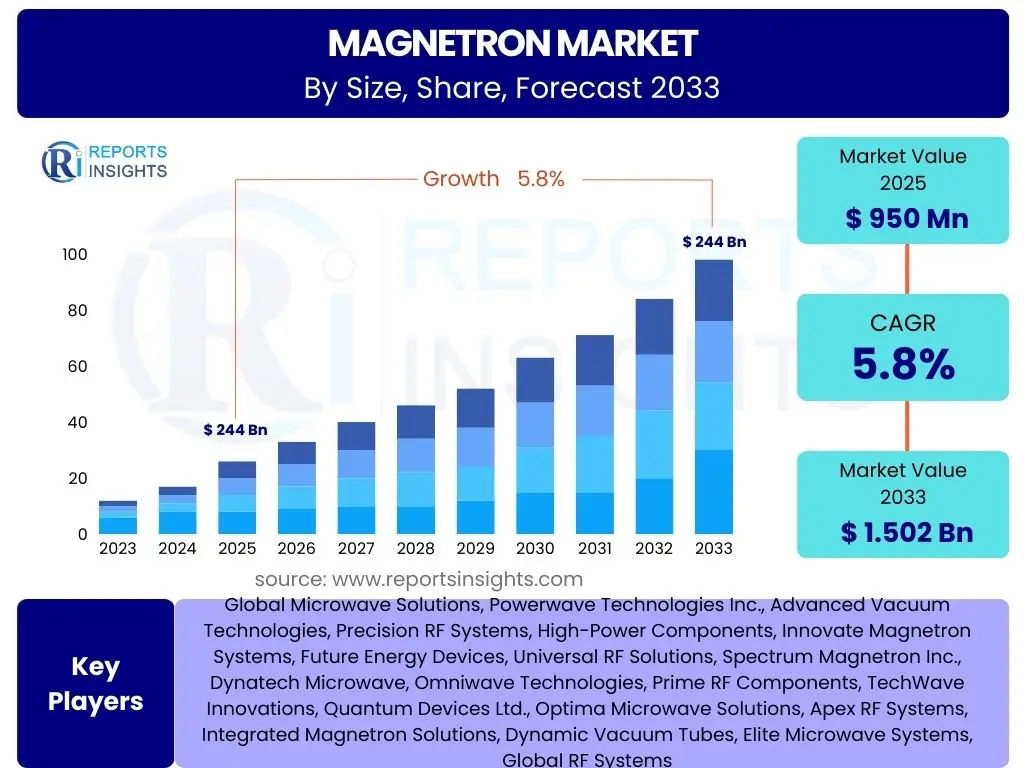

According to Reports Insights Consulting Pvt Ltd, The Magnetron Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 950 Million in 2025 and is projected to reach USD 1.502 Billion by the end of the forecast period in 2033.

Key Magnetron Market Trends & Insights

The global magnetron market is experiencing a significant transformation driven by technological innovation and evolving application demands. A prominent trend involves the pursuit of enhanced energy efficiency and extended operational lifespan, driven by increasing environmental regulations and the need for cost-effective solutions across industrial and commercial sectors. This focus is leading to advancements in magnetron design, including improved cooling mechanisms and material science breakthroughs, which reduce power consumption and increase durability. Furthermore, the market is witnessing a diversification of applications beyond traditional microwave ovens, with significant growth in industrial heating, medical devices, and advanced radar systems, necessitating magnetrons with diverse power outputs and frequency capabilities.

Another key insight is the growing demand for compact and lightweight magnetrons, particularly for portable devices and space-constrained applications. This trend is fostering innovation in miniaturization techniques and the development of high-power-density magnetrons. Additionally, the increasing adoption of solid-state alternatives in certain applications is pushing magnetron manufacturers to innovate, focusing on areas where magnetrons offer superior performance or cost-effectiveness, such as high-power industrial processes and specialized scientific research. The integration of smart features and connectivity for remote monitoring and control is also an emerging trend, enhancing the operational efficiency and predictive maintenance capabilities of magnetron-based systems.

- Emphasis on energy-efficient magnetron designs.

- Miniaturization and compact form factor development.

- Diversification into non-traditional applications like industrial heating, medical, and scientific fields.

- Integration of smart monitoring and control capabilities.

- Advancements in high-power density magnetrons for specialized uses.

AI Impact Analysis on Magnetron

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is poised to revolutionize various aspects of the magnetron market, addressing common user questions regarding performance optimization, predictive maintenance, and manufacturing efficiency. AI can significantly enhance magnetron design by simulating complex electromagnetic fields and thermal behaviors, allowing for rapid prototyping and optimization of new magnetron models for specific power outputs and frequencies. This accelerates the research and development cycle, leading to more efficient and reliable products. Furthermore, AI-driven analytics can process vast amounts of operational data from deployed magnetrons, identifying patterns indicative of potential failures or suboptimal performance, thus enabling proactive maintenance and reducing downtime.

In manufacturing, AI and ML algorithms can optimize production lines, improve quality control, and minimize material waste by precisely controlling fabrication processes. This leads to higher yields and reduced manufacturing costs, which are critical for maintaining competitiveness. For end-users, AI can provide real-time performance monitoring and intelligent control systems for magnetron-powered equipment, such as industrial furnaces or radar systems, ensuring optimal operational parameters and extending equipment lifespan. The predictive capabilities of AI can transform how magnetrons are serviced, shifting from reactive repairs to preventative maintenance, thereby enhancing reliability and overall equipment effectiveness (OEE).

- Predictive maintenance for magnetron-based systems, reducing downtime.

- AI-driven optimization of magnetron design and simulation, improving efficiency.

- Enhanced manufacturing process control and quality assurance through machine learning.

- Real-time performance monitoring and adaptive control systems for operational efficiency.

- Automated fault detection and diagnostics in magnetron applications.

Key Takeaways Magnetron Market Size & Forecast

The magnetron market is positioned for substantial growth, reflecting a robust Compound Annual Growth Rate (CAGR) through 2033, indicating a significant expansion from its current valuation. This growth trajectory is fundamentally driven by the expanding scope of magnetron applications, moving beyond their conventional use in consumer microwave ovens to increasingly vital roles in industrial heating, advanced defense systems, medical imaging, and scientific research. The market's resilience and forward momentum are further supported by ongoing technological advancements focused on improving efficiency, extending lifespan, and reducing the environmental footprint of these devices, addressing key user concerns about sustainability and operational costs. The projected increase in market valuation underscores a strong demand and an optimistic outlook for manufacturers and stakeholders.

A crucial takeaway is the market's evolving segmentation, with high-power and pulsed magnetrons gaining prominence due to their critical utility in specialized industrial and defense applications. This shift highlights a strategic pivot for market players towards higher-value, performance-driven segments. Furthermore, the regional dynamics reveal Asia Pacific as a dominant force, primarily due to its robust manufacturing base and rapidly expanding consumer and industrial sectors, while North America and Europe continue to invest heavily in R&D and high-end applications. The sustained innovation pipeline, coupled with diversification into new end-use industries, positions the magnetron market as a dynamic and expanding sector with considerable opportunities for growth and technological advancement in the coming years.

- Consistent growth trajectory with a significant increase in market valuation by 2033.

- Diversification of applications beyond consumer electronics into industrial and specialized sectors.

- Strong emphasis on technological advancements for improved efficiency and durability.

- Asia Pacific dominates market share, with significant contributions from North America and Europe.

- Increasing strategic focus on high-power and pulsed magnetrons for niche applications.

Magnetron Market Drivers Analysis

The magnetron market is propelled by a confluence of factors, primarily the escalating demand across a diverse range of applications. The robust growth in the industrial sector, particularly in areas requiring precise and efficient heating, such as material processing, plasma generation, and drying, significantly contributes to the demand for high-power magnetrons. Concurrently, the continuous innovation in consumer electronics, especially the ongoing popularity and technological enhancements in microwave ovens, sustains a foundational demand for lower-power magnetrons globally. These two sectors, alongside the specialized requirements of defense and scientific research, form the core demand drivers for magnetron technology.

Technological advancements also play a critical role in expanding the market. Improvements in magnetron design, material science, and manufacturing processes have led to more efficient, reliable, and compact units. This has not only extended their applicability but also made them more attractive to industries seeking energy-efficient solutions and reduced operational costs. Furthermore, the increasing investment in defense and aerospace sectors for advanced radar and electronic warfare systems, which rely heavily on high-performance magnetrons, provides a consistent growth impetus. The development of new medical and scientific instruments that utilize magnetron technology for therapeutic or analytical purposes further diversifies the market's growth avenues.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand in Industrial Heating and Processing | +1.8% | Asia Pacific, North America, Europe | Short- to Mid-Term |

| Continuous Innovation and Adoption in Microwave Ovens | +1.5% | Global, particularly Asia Pacific | Mid-Term |

| Growing Investment in Radar and Defense Systems | +1.2% | North America, Europe, Middle East | Long-Term |

| Emerging Applications in Medical and Scientific Instruments | +0.8% | North America, Europe | Mid- to Long-Term |

Magnetron Market Restraints Analysis

Despite its growth potential, the magnetron market faces several significant restraints that could impede its expansion. One primary challenge is the relatively high power consumption associated with traditional magnetrons compared to alternative heating or power generation technologies. This issue becomes particularly pronounced in an era of increasing energy costs and stringent energy efficiency regulations, pushing industries and consumers towards more energy-efficient solutions. Furthermore, concerns regarding the environmental impact of magnetron manufacturing and disposal, particularly concerning hazardous materials and energy-intensive production, present a regulatory and public perception hurdle that manufacturers must address.

Another critical restraint is the intensifying competition from alternative technologies, notably solid-state power devices. While magnetrons excel in certain high-power, high-frequency applications, solid-state alternatives offer advantages in terms of precision, linearity, and potentially longer lifespan in lower to medium power ranges. This competition forces magnetron manufacturers to innovate continuously and focus on niche applications where their technology remains superior. Additionally, the inherent lifespan limitations of magnetrons due to cathode wear, especially under continuous high-power operation, contribute to higher maintenance and replacement costs for end-users, posing a financial restraint for adoption in certain industrial settings where long-term operational costs are a key consideration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Power Consumption and Energy Inefficiency | 1.3% | Global | Short- to Mid-Term |

| Growing Competition from Solid-State Alternatives | 1.0% | North America, Europe, Asia Pacific | Mid- to Long-Term |

| Limited Lifespan and Maintenance Requirements | 0.7% | Global | Short- to Mid-Term |

| Environmental Concerns and Disposal Challenges | 0.5% | Europe, North America | Long-Term |

Magnetron Market Opportunities Analysis

The magnetron market is ripe with opportunities driven by technological advancements, expanding applications, and untapped geographical markets. A significant opportunity lies in the continuous development of energy-efficient and environmentally sustainable magnetrons. As global energy consumption regulations become stricter and industries prioritize sustainability, the demand for magnetrons that consume less power and are manufactured using eco-friendly processes will surge. This pushes manufacturers to invest in R&D for more efficient designs, innovative materials, and improved manufacturing techniques, which can open up new market segments and enhance competitive advantage.

Another key opportunity is the diversification into niche and high-growth applications beyond traditional consumer microwave ovens. This includes the increasing adoption of magnetrons in advanced medical devices for therapeutic applications, high-precision scientific instruments, and specialized industrial processes such as plasma deposition, semiconductor manufacturing, and advanced material processing. Furthermore, the expansion of global telecommunications infrastructure, particularly for 5G and beyond, presents avenues for magnetrons in high-frequency transmission systems. The burgeoning industrialization and increasing disposable incomes in emerging economies, particularly in Asia Pacific and Latin America, also represent significant untapped markets for both consumer and industrial magnetron applications, offering considerable growth potential for market players willing to strategically expand their presence.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Energy-Efficient and Sustainable Magnetrons | +1.5% | Global | Mid- to Long-Term |

| Expansion into New Industrial and Scientific Niche Applications | +1.2% | North America, Europe, Asia Pacific | Mid- to Long-Term |

| Untapped Market Potential in Emerging Economies | +0.9% | Asia Pacific, Latin America, MEA | Long-Term |

| Integration into Advanced Telecommunication Systems | +0.7% | Global | Mid- to Long-Term |

Magnetron Market Challenges Impact Analysis

The magnetron market is navigating several challenges that demand strategic responses from manufacturers and stakeholders. One significant hurdle is the complexity and high cost associated with the manufacturing of advanced magnetrons. Producing high-power and specialized magnetrons requires sophisticated fabrication techniques, precision engineering, and often involves rare or expensive materials, which can drive up production costs and limit scalability. This inherent complexity also contributes to longer research and development cycles, hindering rapid innovation and market responsiveness, especially in fast-evolving application areas.

Another critical challenge involves the volatility and security of the supply chain for essential raw materials. Magnetrons often require specific metals and components, and disruptions in the supply chain, whether due to geopolitical tensions, natural disasters, or trade disputes, can lead to material shortages and price fluctuations. This unpredictability impacts production schedules and profitability. Furthermore, the market faces increasing pressure from stringent regulatory compliance requirements, particularly concerning electromagnetic interference (EMI) and power emission standards. Adhering to diverse global and regional regulations adds layers of complexity and cost to product design and certification, posing a continuous challenge for market entry and product deployment across different geographies. Maintaining competitiveness in the face of these manufacturing, supply chain, and regulatory complexities requires significant investment and strategic foresight.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Complexity and Costs | 1.2% | Global | Short- to Mid-Term |

| Supply Chain Volatility for Critical Raw Materials | 1.0% | Global | Short-Term |

| Stringent Regulatory Compliance and Emission Standards | 0.8% | Europe, North America, Asia Pacific | Mid-Term |

| Intense R&D Requirements for Next-Generation Magnetrons | 0.6% | Global | Long-Term |

Magnetron Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global magnetron market, encompassing historical data, current market dynamics, and future projections. The scope includes a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges influencing industry growth. It offers extensive segmentation analysis by type, application, power range, frequency band, and end-use industry, alongside a thorough regional assessment to provide a holistic view of the market landscape. The report also profiles key industry players, offering insights into their competitive strategies and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 950 Million |

| Market Forecast in 2033 | USD 1.502 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Microwave Solutions, Powerwave Technologies Inc., Advanced Vacuum Technologies, Precision RF Systems, High-Power Components, Innovate Magnetron Systems, Future Energy Devices, Universal RF Solutions, Spectrum Magnetron Inc., Dynatech Microwave, Omniwave Technologies, Prime RF Components, TechWave Innovations, Quantum Devices Ltd., Optima Microwave Solutions, Apex RF Systems, Integrated Magnetron Solutions, Dynamic Vacuum Tubes, Elite Microwave Systems, Global RF Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The magnetron market is meticulously segmented across various parameters to provide granular insights into its diverse applications, technological variations, and end-user adoption patterns. This detailed segmentation allows for a comprehensive understanding of the market dynamics, identifying specific growth pockets and competitive landscapes within each category. Analyzing the market by type, such as Continuous Wave (CW) and Pulsed Magnetrons, helps differentiate between steady output applications and those requiring short, high-energy bursts, revealing their respective market sizes and growth rates based on technological advancements and specific industry needs.

Further segmentation by application areas, including microwave ovens, radar systems, industrial heating, and medical instruments, illuminates the primary demand drivers and the evolving importance of magnetrons in critical sectors. Power range and frequency band segmentation provide insights into the technical specifications driving demand, from low-power consumer devices to high-power industrial and defense systems. Lastly, the end-use industry segmentation provides a clear picture of magnetron consumption across key verticals like consumer electronics, industrial manufacturing, defense, and healthcare, aiding stakeholders in strategic planning and product development targeted at specific industry requirements and market opportunities.

- By Type:

- Continuous Wave (CW) Magnetrons

- Pulsed Magnetrons

- By Application:

- Microwave Ovens

- Radar Systems

- Industrial Heating

- Medical Applications

- Scientific Instruments

- Others

- By Power Range:

- Low Power (less than 1 kW)

- Medium Power (1 kW to 10 kW)

- High Power (greater than 10 kW)

- By Frequency Band:

- S-Band

- C-Band

- X-Band

- Ku-Band

- Ka-Band

- L-Band

- Others

- By End-Use Industry:

- Consumer Electronics

- Industrial

- Defense

- Healthcare

- Scientific Research

- Telecommunications

Regional Highlights

- North America: This region demonstrates a strong demand for magnetrons, particularly in the defense and aerospace sectors due to significant investments in radar and electronic warfare systems. The presence of robust industrial manufacturing and advanced research facilities also fuels the adoption of high-power magnetrons for various industrial heating and scientific applications.

- Europe: Europe is a key market driven by advancements in industrial automation, material processing, and scientific research. The region's stringent energy efficiency regulations also push for innovation in more energy-efficient magnetron designs, fostering growth in both consumer and specialized industrial segments.

- Asia Pacific (APAC): APAC stands as the dominant market for magnetrons, primarily due to its massive manufacturing base for consumer electronics, especially microwave ovens. Rapid industrialization, increasing defense spending in countries like China and India, and expanding healthcare infrastructure further contribute to the region's substantial market share and growth potential.

- Latin America: This region is an emerging market for magnetrons, experiencing gradual growth driven by increasing industrialization and expanding consumer electronics markets. Investments in infrastructure development and growing adoption of industrial heating processes contribute to the demand.

- Middle East and Africa (MEA): The MEA region exhibits growth potential, largely influenced by rising defense expenditures and ongoing infrastructure projects that require advanced radar and communication systems. The industrial sector's development in key countries also contributes to the modest but growing demand for magnetron applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Magnetron Market.- Global Microwave Solutions

- Powerwave Technologies Inc.

- Advanced Vacuum Technologies

- Precision RF Systems

- High-Power Components

- Innovate Magnetron Systems

- Future Energy Devices

- Universal RF Solutions

- Spectrum Magnetron Inc.

- Dynatech Microwave

- Omniwave Technologies

- Prime RF Components

- TechWave Innovations

- Quantum Devices Ltd.

- Optima Microwave Solutions

- Apex RF Systems

- Integrated Magnetron Solutions

- Dynamic Vacuum Tubes

- Elite Microwave Systems

- Global RF Systems

Frequently Asked Questions

Analyze common user questions about the Magnetron market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a magnetron and what are its primary applications?

A magnetron is a high-power vacuum tube that generates microwaves using the interaction of a stream of electrons with a magnetic field. Its primary applications include microwave ovens for cooking, radar systems for detection and ranging, industrial heating and drying processes, medical linear accelerators, and scientific research instruments.

How large is the global magnetron market and what is its growth forecast?

The global magnetron market is estimated at USD 950 Million in 2025 and is projected to reach USD 1.502 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 5.8%. This growth is driven by expanding applications and technological advancements.

What are the key factors driving the growth of the magnetron market?

Key drivers include increasing demand from industrial heating and processing sectors, sustained innovation in consumer microwave ovens, growing investments in defense and radar systems, and emerging applications in medical and scientific instruments. Technological advancements for improved efficiency also play a significant role.

What challenges does the magnetron market face?

Challenges include high manufacturing complexity and costs, volatility in the supply chain for critical raw materials, stringent regulatory compliance for emissions and safety, and intense research and development requirements for next-generation magnetrons. Competition from alternative technologies like solid-state devices also poses a restraint.

How is AI impacting the magnetron industry?

AI is impacting the magnetron industry by enabling predictive maintenance for enhanced reliability, optimizing magnetron design and simulation for improved efficiency, automating quality control in manufacturing, and facilitating real-time performance monitoring in operational systems. This leads to better performance, reduced downtime, and lower costs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted