Lightning Arrestor Market

Lightning Arrestor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702087 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Lightning Arrestor Market Size

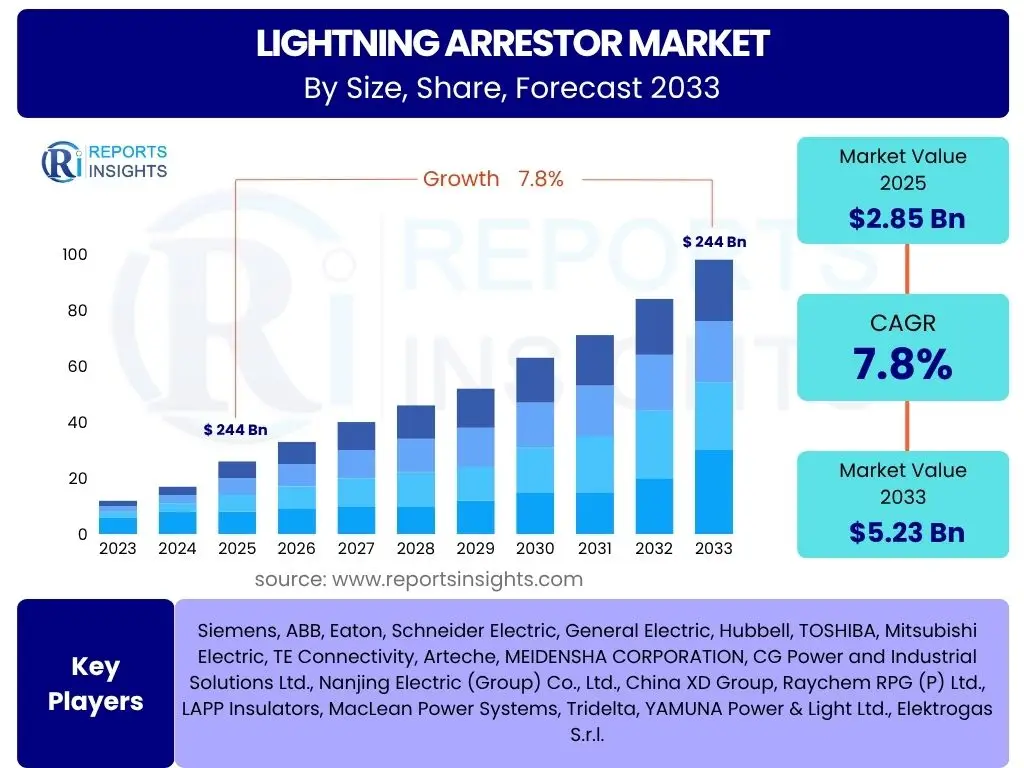

According to Reports Insights Consulting Pvt Ltd, The Lightning Arrestor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 5.23 billion by the end of the forecast period in 2033.

Key Lightning Arrestor Market Trends & Insights

The global lightning arrestor market is experiencing dynamic shifts driven by accelerating infrastructure development, particularly in emerging economies, and the global push towards renewable energy integration. Users frequently inquire about the forces shaping this market, including technological advancements and evolving regulatory landscapes. A primary trend involves the increasing demand for sophisticated lightning protection solutions in smart grids and urbanized areas, where grid stability and equipment longevity are paramount. Furthermore, the market is witnessing a shift towards polymer-based arrestors due to their lighter weight, improved hydrophobic properties, and superior performance in contaminated environments compared to traditional porcelain types.

Another significant insight revolves around the growing emphasis on predictive maintenance and real-time monitoring capabilities, which are becoming integral components of modern lightning protection systems. This trend is fueled by the desire to minimize downtime, reduce operational costs, and enhance the overall reliability of power transmission and distribution networks. The expansion of high-voltage direct current (HVDC) transmission lines and ultra-high voltage (UHV) substations globally also necessitates more robust and higher-rated lightning arrestors, driving innovation in design and material science to meet these demanding specifications. Stakeholders are keen to understand how these trends will influence investment decisions and market competitiveness.

- Increasing adoption of polymer-based lightning arrestors for enhanced performance and durability.

- Integration of smart monitoring systems and IoT capabilities for real-time fault detection and predictive maintenance.

- Rising demand for high-voltage and ultra-high-voltage lightning arrestors driven by HVDC and UHV transmission projects.

- Emphasis on sustainable and environmentally friendly materials in arrestor manufacturing.

- Growing trend of retrofitting and upgrading aging power infrastructure with modern protection solutions.

AI Impact Analysis on Lightning Arrestor

User queries regarding the impact of Artificial Intelligence (AI) on the lightning arrestor domain typically focus on how AI can enhance the effectiveness, efficiency, and intelligence of protection systems. AI is poised to revolutionize the design, monitoring, and maintenance of lightning arrestors by enabling more sophisticated predictive analytics. Through machine learning algorithms, AI can analyze vast datasets of weather patterns, lightning strike probabilities, grid conditions, and historical equipment performance to predict potential failures or optimal maintenance schedules for arrestors, thereby reducing unexpected outages and extending asset life. This capability moves beyond traditional condition-based monitoring to a truly predictive paradigm.

Furthermore, AI can facilitate the development of adaptive lightning protection systems that can dynamically adjust their parameters based on real-time environmental conditions and grid load variations. This could lead to more precise and efficient surge protection, minimizing energy losses and optimizing system responsiveness. In manufacturing, AI can be employed for quality control, material optimization, and automated assembly processes, leading to higher quality and more cost-effective production of arrestors. The integration of AI also supports the broader vision of smart grids, where lightning arrestors become intelligent nodes contributing to the overall resilience and self-healing capabilities of the power network, addressing user expectations for enhanced reliability and operational intelligence.

- Enhanced predictive maintenance and fault detection through machine learning algorithms analyzing environmental and operational data.

- Optimization of lightning arrestor performance and lifespan by dynamic adjustment based on real-time conditions.

- Improved manufacturing processes, quality control, and material optimization using AI-driven analytics.

- Integration of intelligent lightning protection components into smart grid infrastructure for autonomous decision-making.

- Development of advanced simulation and modeling tools for arrestor design and placement using AI.

Key Takeaways Lightning Arrestor Market Size & Forecast

The lightning arrestor market is set for substantial growth through 2033, driven primarily by global investments in power transmission and distribution infrastructure and the burgeoning renewable energy sector. Users are keen to understand the primary drivers behind this expansion and where the most significant opportunities lie. The market's upward trajectory is firmly linked to urbanization, industrialization, and the increasing complexity of modern electrical grids, all of which necessitate robust surge protection mechanisms. The forecast indicates a stable and accelerated demand, reflecting the essential nature of lightning arrestors in ensuring grid reliability and safety across diverse applications, from utility-scale operations to industrial facilities.

A crucial takeaway is the evolving technological landscape, with a notable shift towards smarter, more durable, and environmentally conscious solutions. This includes the widespread adoption of metal oxide varistor (MOV) technology and the increasing preference for polymer-housed arrestors over traditional porcelain types. Geographically, Asia Pacific is expected to remain a dominant force, fueled by massive infrastructure projects and expanding power generation capacities. For stakeholders, understanding these market dynamics is vital for strategic planning, product development, and identifying key regions for investment to capitalize on the sustained growth projected for the lightning arrestor market.

- Consistent market expansion driven by global infrastructure development and renewable energy integration.

- Technological advancements, particularly in MOV and polymer arrestor solutions, are shaping product offerings.

- Asia Pacific is projected to lead market growth due to rapid industrialization and urbanization.

- Emphasis on grid modernization and smart technology integration will enhance market value.

- The essential role of lightning arrestors in ensuring electrical safety and minimizing economic losses underscores continuous demand.

Lightning Arrestor Market Drivers Analysis

The global lightning arrestor market is significantly propelled by several key factors that underscore its indispensable role in modern electrical infrastructure. A primary driver is the accelerating global demand for electricity, which necessitates the expansion and upgrade of power generation, transmission, and distribution networks. As more power plants, substations, and overhead lines are constructed, the corresponding requirement for effective lightning protection solutions naturally escalates. This is particularly evident in emerging economies undergoing rapid industrialization and urbanization, leading to massive investments in grid infrastructure.

Furthermore, the escalating integration of renewable energy sources such as solar and wind power into national grids acts as a substantial growth catalyst. These renewable installations, often located in open and exposed areas, are highly susceptible to lightning strikes, thus requiring comprehensive and reliable lightning arrestor solutions to protect expensive equipment and ensure continuous power supply. Additionally, stringent government regulations and safety standards across various industries, mandating the installation of surge protection devices to safeguard human life and critical equipment, contribute significantly to market expansion. The global push for smart grid initiatives, aiming for enhanced grid reliability and efficiency, also drives demand for advanced and intelligent lightning arrestors capable of seamless integration into these modern systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Power Generation & Transmission Infrastructure | +2.1% | Global, particularly APAC, MEA | Short to Long-term (2025-2033) |

| Increasing Integration of Renewable Energy Sources | +1.8% | Europe, North America, China, India | Short to Long-term (2025-2033) |

| Strict Regulatory Compliance and Safety Standards | +1.5% | Global, especially Developed Economies | Ongoing, Continuous |

| Rapid Urbanization and Industrialization | +1.2% | Asia Pacific, Latin America, Africa | Medium to Long-term (2025-2033) |

| Expansion of Smart Grid Initiatives | +0.8% | North America, Europe, parts of Asia | Medium to Long-term (2027-2033) |

Lightning Arrestor Market Restraints Analysis

Despite robust growth drivers, the lightning arrestor market faces several restraints that could potentially impede its expansion. One significant challenge revolves around the relatively high initial investment costs associated with deploying advanced lightning arrestor systems, especially for large-scale utility projects or industrial applications. While these costs are justified by long-term protection and reduced downtime, budget constraints, particularly in developing regions, can lead to the deferral or scaling back of essential infrastructure upgrades, impacting demand for premium solutions. This cost factor often influences purchase decisions, pushing buyers towards more economical, albeit less advanced, alternatives.

Another restraint is the fluctuating prices of raw materials, such as porcelain, polymers, and metal oxides, which are crucial for arrestor manufacturing. Volatility in commodity markets can lead to increased production costs, subsequently affecting the final product pricing and profit margins for manufacturers. Furthermore, the lack of standardized regulations and varying local codes across different regions can create complexities for global manufacturers. Adhering to diverse specifications requires customized production processes and can increase compliance costs, hindering market penetration in certain geographies. The extended lifespan of existing lightning arrestors also presents a restraint, as it reduces the frequency of replacement demand, primarily limiting new sales to expansion projects rather than widespread retrofitting, although this is gradually changing with advancements in technology.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs | -1.0% | Developing Economies, Budget-constrained Utilities | Short to Medium-term (2025-2029) |

| Volatility in Raw Material Prices | -0.7% | Global | Short to Medium-term (2025-2029) |

| Lack of Standardized Regulations Across Regions | -0.5% | Global, particularly emerging markets | Medium to Long-term (2027-2033) |

| Long Operational Lifespan of Existing Devices | -0.3% | Developed Economies | Long-term (2028-2033) |

Lightning Arrestor Market Opportunities Analysis

Significant opportunities are emerging within the lightning arrestor market, particularly driven by technological advancements and the global shift towards more resilient and efficient power infrastructure. The advent of smart lightning arrestors, integrated with IoT capabilities for real-time monitoring, diagnostics, and predictive analytics, presents a substantial growth avenue. These intelligent devices can communicate their operational status, alert maintenance teams to potential issues, and even self-diagnose, significantly reducing downtime and operational costs for utility providers and industrial operators. This shift towards smart protection systems aligns perfectly with the broader smart grid initiatives worldwide, creating a demand for technologically advanced solutions.

Another major opportunity lies in the burgeoning market for retrofitting and upgrading aging power infrastructure, especially in developed economies. Many existing transmission and distribution networks rely on older, less efficient lightning protection technologies, making them vulnerable to modern grid demands and increasingly severe weather events. The need to enhance grid resilience and improve safety provides a continuous market for advanced lightning arrestors designed for seamless integration into legacy systems. Furthermore, the rapid expansion of data centers, telecommunication networks, and electric vehicle charging infrastructure globally represents a niche but high-growth segment, as these critical facilities require robust and uninterrupted power supply, making advanced surge protection essential. The development of rural electrification projects in underserved regions also offers greenfield opportunities for basic to medium-voltage arrestors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Smart Lightning Protection Systems (IoT-enabled) | +1.5% | Global, focus on developed markets | Short to Long-term (2025-2033) |

| Retrofitting and Upgrading Aging Infrastructure | +1.2% | North America, Europe, Japan | Medium to Long-term (2027-2033) |

| Growth in Data Centers & Telecommunication Networks | +0.9% | Global | Short to Medium-term (2025-2030) |

| Rural Electrification Initiatives | +0.7% | Asia Pacific, Africa, Latin America | Medium to Long-term (2026-2033) |

Lightning Arrestor Market Challenges Impact Analysis

The lightning arrestor market, while promising, is not immune to significant challenges that can affect its growth trajectory and operational efficiency. Intense competition among a large number of established global players and regional manufacturers poses a constant challenge. This competitive landscape often leads to pricing pressures, forcing companies to innovate continuously and differentiate their products based on performance, cost-effectiveness, and ancillary services. Maintaining profitability amidst aggressive pricing strategies becomes a critical concern, particularly for smaller market participants who may lack the economies of scale of larger entities.

Another notable challenge is the complexity of supply chain management, particularly for manufacturers sourcing specialized raw materials and components globally. Geopolitical tensions, trade disputes, and unforeseen events such as pandemics can lead to disruptions in the supply chain, causing delays in production and increasing logistical costs. This volatility demands robust supply chain resilience and diversification strategies. Furthermore, the rapid pace of technological advancements, while an opportunity, also presents a challenge of technological obsolescence. Manufacturers must invest heavily in R&D to keep pace with evolving industry standards and customer demands, such as the transition to higher voltage applications or the integration of digital features, ensuring their products remain relevant and competitive in a dynamic market. Educating end-users about the long-term benefits of investing in premium lightning protection solutions over cheaper alternatives also remains a continuous challenge for market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Price Pressures | -0.8% | Global | Ongoing, Continuous |

| Supply Chain Disruptions and Raw Material Volatility | -0.6% | Global | Short to Medium-term (2025-2029) |

| Technological Obsolescence and Need for Continuous R&D | -0.4% | Global | Medium to Long-term (2027-2033) |

| Awareness and Education Gap in Developing Regions | -0.3% | Emerging Markets | Long-term (2028-2033) |

Lightning Arrestor Market - Updated Report Scope

This market research report offers a comprehensive analysis of the global lightning arrestor market, providing detailed insights into its current size, historical performance, and future growth projections from 2025 to 2033. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges that shape the industry landscape. It also delves into key market trends, technological advancements, and the competitive environment, offering a strategic outlook for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 5.23 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens, ABB, Eaton, Schneider Electric, General Electric, Hubbell, TOSHIBA, Mitsubishi Electric, TE Connectivity, Arteche, MEIDENSHA CORPORATION, CG Power and Industrial Solutions Ltd., Nanjing Electric (Group) Co., Ltd., China XD Group, Raychem RPG (P) Ltd., LAPP Insulators, MacLean Power Systems, Tridelta, YAMUNA Power & Light Ltd., Elektrogas S.r.l. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

A comprehensive segmentation analysis of the lightning arrestor market provides granular insights into various product categories, material types, voltage ratings, and end-use applications. This detailed breakdown is critical for understanding specific market niches, identifying high-growth areas, and tailoring strategic approaches. The market is broadly categorized by type, which includes distribution line, station line, riser pole, and line type arrestors, each designed for specific points within the electrical grid. This differentiation reflects the diverse operational requirements and environmental conditions encountered in various parts of the power infrastructure.

Further segmentation by material—primarily porcelain and polymer (silicone rubber, EPDM)—highlights the ongoing shift towards advanced composite materials due to their superior performance characteristics, such as lighter weight, better hydrophobic properties, and enhanced resistance to pollution and vandalism. The voltage-based segmentation, ranging from low to ultra-high voltage, directly corresponds to the different levels of power transmission and distribution, indicating specialized demand for each segment. Moreover, the segmentation by application (e.g., overhead lines, substations, industrial equipment) and end-use industry (e.g., energy & power, industrial, telecommunications) provides a clear picture of where lightning arrestors are most critically deployed, revealing the varied demands and growth potential across different sectors.

- By Type:

- Distribution Line Arrestor: Designed for distribution lines and transformers, protecting residential and commercial areas.

- Station Line Arrestor: Used in substations to protect critical high-voltage equipment.

- Riser Pole Arrestor: Specifically for protecting pole-mounted equipment.

- Line Type Arrestor: Applied directly to transmission lines for enhanced protection.

- Others: Includes special application arrestors.

- By Material:

- Porcelain: Traditional material, known for robustness but susceptible to breakage and heavier.

- Polymer:

- Silicone Rubber: Widely used due to excellent hydrophobic properties and light weight.

- EPDM (Ethylene Propylene Diene Monomer): Offers good electrical insulation and weather resistance.

- Other Composites: Emerging materials offering enhanced performance and durability.

- By Voltage:

- Low Voltage (Up to 1 kV): Primarily for residential, commercial, and small industrial applications.

- Medium Voltage (1 kV to 69 kV): Common in power distribution networks.

- High Voltage (70 kV to 220 kV): Used in main transmission lines and larger substations.

- Extra High Voltage (221 kV to 765 kV): Crucial for long-distance power transmission.

- Ultra High Voltage (Above 765 kV): For the most advanced and high-capacity transmission systems.

- By Application:

- Overhead Lines: Primary application for protecting vast electrical networks.

- Substations: Critical for safeguarding high-value equipment like transformers, circuit breakers.

- Transformers: Direct protection for power transformers at various voltage levels.

- Switchgears: Protection for switching and control devices.

- Power Distribution Equipment: Encompasses various components within the distribution grid.

- Industrial Equipment: Safeguarding machinery and control systems in factories.

- Telecommunication Towers: Essential for protecting sensitive communication electronics.

- Residential & Commercial Buildings: Protection for internal electrical systems and appliances.

- By End-Use Industry:

- Energy & Power:

- Utility Sector: Largest segment, includes power generation, transmission, and distribution.

- Renewable Energy Plants: Solar farms, wind turbines, hydro power plants.

- Industrial: Manufacturing facilities, oil & gas refineries, mining operations, chemical plants.

- Residential: Homes and residential complexes.

- Commercial: Offices, retail centers, data centers.

- Telecommunications: Cell towers, communication hubs.

- Railways & Transportation: Signaling systems, electric locomotives, metro networks.

- Energy & Power:

Regional Highlights

- North America: This region demonstrates a mature market for lightning arrestors, driven by the ongoing need for grid modernization, replacement of aging infrastructure, and significant investments in renewable energy integration. The U.S. and Canada are key contributors, focusing on smart grid development and enhancing grid resilience against severe weather events. Strict regulatory frameworks and a high awareness of electrical safety further bolster demand for advanced, high-performance arrestors.

- Europe: Europe is characterized by stringent environmental regulations and a strong emphasis on sustainable energy solutions, leading to a high demand for eco-friendly and polymer-based lightning arrestors. Countries like Germany, France, and the UK are investing heavily in offshore wind farms and cross-border interconnectors, necessitating robust high-voltage protection. The push for smart cities and smart grids also contributes significantly to market growth here.

- Asia Pacific (APAC): APAC is anticipated to be the fastest-growing market for lightning arrestors, fueled by rapid industrialization, urbanization, and massive investments in power generation and transmission infrastructure, particularly in China and India. The expanding renewable energy sector, coupled with government initiatives for rural electrification and upgrading existing grids, drives substantial demand. Southeast Asian countries also present significant growth opportunities due to their developing economies and increasing power consumption.

- Latin America: This region is experiencing steady growth in the lightning arrestor market, largely due to ongoing grid expansion projects, increasing industrial activities, and the development of renewable energy projects, particularly in Brazil and Mexico. The vulnerability to severe lightning storms in many parts of the region also necessitates robust protection solutions, although economic fluctuations can occasionally impact investment timelines.

- Middle East and Africa (MEA): The MEA region is witnessing considerable growth driven by substantial investments in oil & gas infrastructure, rapid urbanization, and diversification of economies away from fossil fuels towards renewable energy. Countries like Saudi Arabia, UAE, and South Africa are undertaking large-scale infrastructure projects that require advanced electrical protection. The expansion of telecommunication networks also contributes to market demand in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Lightning Arrestor Market.- Siemens

- ABB

- Eaton

- Schneider Electric

- General Electric

- Hubbell

- TOSHIBA

- Mitsubishi Electric

- TE Connectivity

- Arteche

- MEIDENSHA CORPORATION

- CG Power and Industrial Solutions Ltd.

- Nanjing Electric (Group) Co., Ltd.

- China XD Group

- Raychem RPG (P) Ltd.

- LAPP Insulators

- MacLean Power Systems

- Tridelta

- YAMUNA Power & Light Ltd.

- Elektrogas S.r.l.

Frequently Asked Questions

What is a lightning arrestor and how does it function?

A lightning arrestor, also known as a surge arrester, is an electrical device designed to protect electrical equipment and power systems from high-voltage surges caused by lightning strikes or other transient overvoltages. It functions by diverting the excessive current from the surge to the ground, thereby limiting the voltage across the equipment and preventing damage, then immediately returning to a non-conducting state once the surge has passed.

What are the primary types of lightning arrestors available in the market?

The primary types of lightning arrestors include distribution line arrestors, station line arrestors, riser pole arrestors, and line type arrestors, each tailored for specific applications within the power grid. They are also categorized by voltage rating (low, medium, high, extra-high, ultra-high) and material (porcelain or polymer-based like silicone rubber or EPDM), reflecting diverse operational requirements and technological advancements.

Which factors are driving the growth of the lightning arrestor market?

Key drivers include rapid expansion of power generation and transmission infrastructure globally, increasing integration of renewable energy sources, stringent safety regulations mandating surge protection, accelerating urbanization and industrialization, and the ongoing development of smart grid initiatives aimed at enhancing grid reliability and efficiency.

How does AI impact the lightning arrestor industry?

AI impacts the lightning arrestor industry by enabling enhanced predictive maintenance through data analysis, optimizing arrestor performance and lifespan, improving manufacturing processes and quality control, and facilitating the integration of intelligent protection components into smart grid systems for autonomous operations and real-time responsiveness.

What are the significant challenges faced by the lightning arrestor market?

Major challenges include intense market competition leading to price pressures, volatility in raw material prices and supply chain disruptions, the continuous need for research and development to counter technological obsolescence, and the long operational lifespan of existing devices which can slow replacement cycles, particularly in developed regions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted