Light Gauge Steel Market

Light Gauge Steel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700126 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

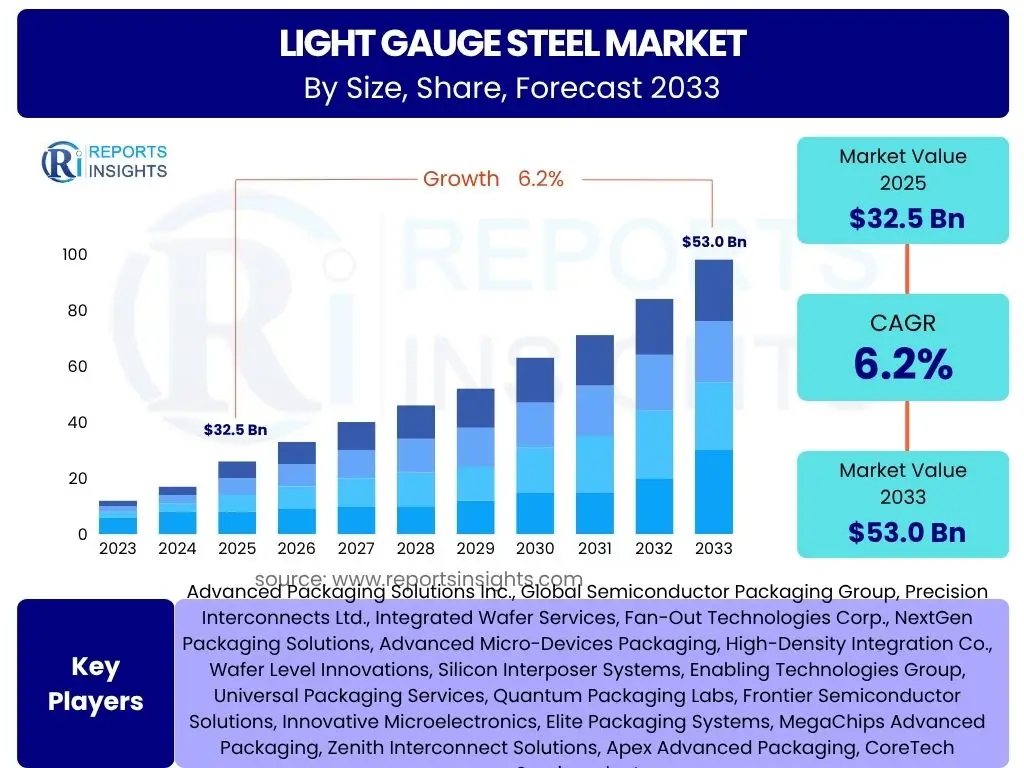

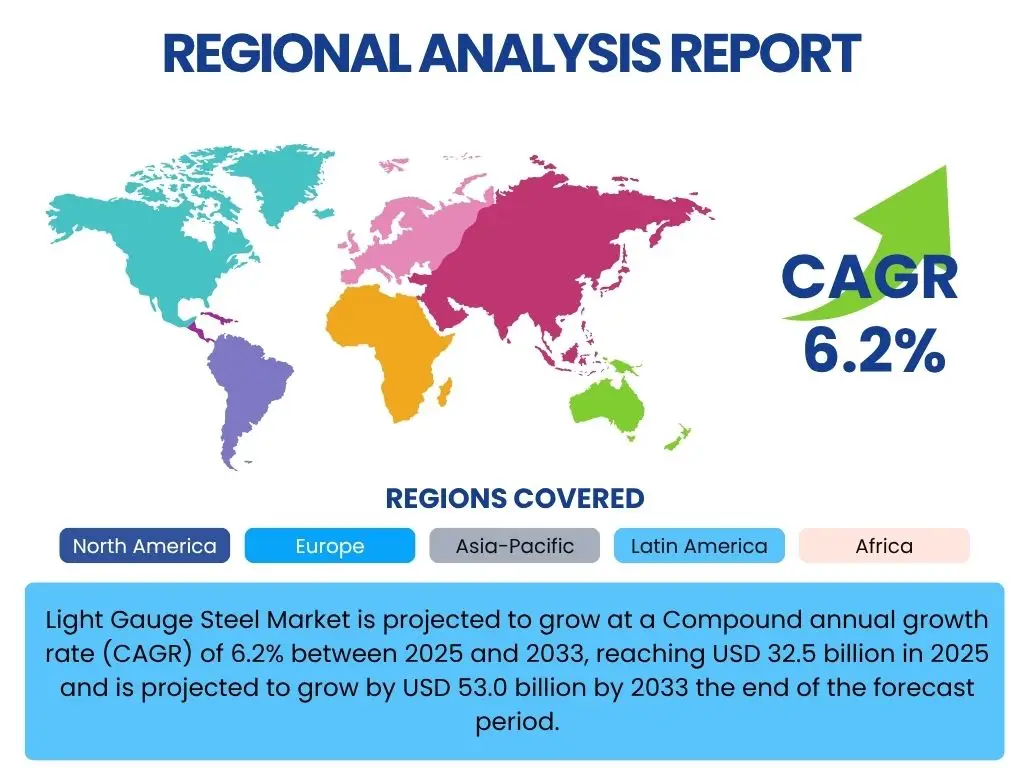

Light Gauge Steel Market is projected to grow at a Compound annual growth rate (CAGR) of 6.2% between 2025 and 2033, reaching USD 32.5 billion in 2025 and is projected to grow by USD 53.0 billion by 2033 the end of the forecast period.

Key Light Gauge Steel Market Trends & Insights

The Light Gauge Steel (LGS) market is experiencing dynamic shifts driven by advancements in construction methodologies and increasing emphasis on sustainable building practices. Key trends indicate a significant acceleration in the adoption of prefabricated and modular construction, where LGS offers inherent advantages due to its lightweight nature, high strength-to-weight ratio, and ease of assembly. This shift is not only improving construction efficiency but also reducing on-site labor requirements and waste generation. Furthermore, there is a growing trend towards designing energy-efficient and resilient structures, with LGS framing facilitating superior insulation and structural integrity against seismic activities and extreme weather conditions.

Technological integration is another paramount trend, encompassing Building Information Modeling (BIM) for precise design and fabrication, and automation in manufacturing processes. This integration enhances accuracy, reduces material waste, and speeds up production cycles, making LGS an even more attractive option for large-scale projects. The market is also witnessing a rising preference for sustainable building materials, positioning LGS as a strong contender due to steel's recyclability and the potential for reduced carbon footprints in construction. Urbanization and the need for rapid infrastructure development globally further underpin these trends, creating sustained demand for efficient and durable construction solutions.

- Accelerated adoption of modular and prefabricated construction methods.

- Increasing demand for sustainable and energy-efficient building solutions.

- Integration of advanced digital technologies like BIM and automation in LGS manufacturing.

- Growing focus on disaster-resilient building design.

- Expansion into diverse applications beyond residential, including commercial and industrial sectors.

- Emphasis on lightweight construction materials for urban infill and vertical expansion.

- Development of advanced LGS alloys and connection systems for enhanced performance.

AI Impact Analysis on Light Gauge Steel

The integration of Artificial Intelligence (AI) is set to revolutionize various facets of the Light Gauge Steel (LGS) market, from design and manufacturing to logistics and on-site assembly. AI-powered algorithms can optimize structural designs, ensuring material efficiency and reducing waste, while simultaneously enhancing structural integrity and performance. In the manufacturing domain, AI can drive predictive maintenance for machinery, improve quality control through automated inspection systems, and optimize production schedules to meet fluctuating demand with greater agility. This not only leads to cost savings but also significantly boosts operational efficiency and product consistency.

Beyond manufacturing, AI is also impacting supply chain management for LGS components by forecasting material needs, optimizing inventory levels, and improving logistics routes, thereby minimizing delays and associated costs. On construction sites, AI and machine learning are being leveraged for project management, risk assessment, and even autonomous or semi-autonomous assembly of LGS structures, leading to faster project completion and improved safety. The data generated from LGS projects, when analyzed by AI, can provide valuable insights into performance, durability, and cost-effectiveness, informing future innovations and driving continuous improvement across the industry.

- Optimization of LGS structural designs for material efficiency and performance.

- Enhanced predictive maintenance and quality control in LGS manufacturing.

- Improved supply chain and logistics management for LGS components.

- AI-driven project management and risk assessment on construction sites.

- Facilitation of autonomous assembly and robotics for faster construction.

Key Takeaways Light Gauge Steel Market Size & Forecast

- The Light Gauge Steel Market is projected to achieve a significant compound annual growth rate (CAGR) of 6.2% between 2025 and 2033.

- The market size is estimated at USD 32.5 billion in 2025, reflecting a robust foundation for future expansion.

- By the end of the forecast period in 2033, the market is expected to reach USD 53.0 billion, indicating substantial growth potential.

- This growth is primarily driven by increasing adoption of prefabricated construction, sustainability initiatives, and technological advancements in design and manufacturing.

- Key regions such as Asia Pacific and North America are anticipated to lead market expansion due to rapid urbanization and infrastructure development.

Light Gauge Steel Market Drivers Analysis

The Light Gauge Steel (LGS) market is propelled by a confluence of macroeconomic and industry-specific factors that underscore its increasing appeal in modern construction. One of the primary drivers is the escalating global demand for rapid and efficient construction solutions, particularly evident in the burgeoning urban centers and regions undergoing significant infrastructure development. LGS framing allows for faster erection times compared to traditional materials, reducing project timelines and associated labor costs, which is crucial in a labor-scarce environment. Furthermore, the inherent advantages of LGS, such as its lightweight nature, high strength-to-weight ratio, and non-combustible properties, contribute to its growing preference in various building applications, from residential to commercial and industrial.

Another significant driver is the growing emphasis on sustainable and green building practices worldwide. Light Gauge Steel is a highly recyclable material, and its use often leads to reduced construction waste on-site. The precision of LGS fabrication minimizes material off-cuts, and the superior thermal performance achievable with LGS framing contributes to more energy-efficient buildings, aligning with global sustainability goals and stringent energy codes. This environmental advantage positions LGS as a preferred material for environmentally conscious projects and LEED-certified buildings. Additionally, the increasing adoption of Building Information Modeling (BIM) and modular construction techniques significantly complements LGS systems, enhancing design accuracy, prefabrication efficiency, and overall project integration, thereby driving its market penetration.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Prefabricated and Modular Construction | +1.8% | Global, especially North America, Europe, Asia Pacific | Short to Medium Term (2025-2029) |

| Growing Demand for Sustainable and Green Building Materials | +1.5% | Global, particularly developed economies | Medium to Long Term (2027-2033) |

| Advancements in Manufacturing Technology and Automation | +1.0% | Developed regions, manufacturing hubs (e.g., China, US, Germany) | Medium Term (2026-2031) |

| Urbanization and Infrastructure Development | +1.2% | Asia Pacific, Latin America, Middle East & Africa | Short to Long Term (2025-2033) |

| Durability and Fire Resistance of Steel Structures | +0.7% | Global, particularly areas with stringent building codes | Long Term (2028-2033) |

Light Gauge Steel Market Restraints Analysis

Despite the robust growth trajectory, the Light Gauge Steel (LGS) market faces several restraints that could impede its full potential. One significant challenge is the volatility in raw material prices, primarily steel. Fluctuations in global steel prices, influenced by supply-demand dynamics, geopolitical events, and trade policies, can directly impact the manufacturing cost of LGS products. This unpredictability makes it difficult for manufacturers and contractors to forecast project costs accurately, potentially affecting profitability and the adoption rate of LGS solutions, especially for budget-sensitive projects.

Another notable restraint is the prevailing lack of awareness and a relatively limited skilled workforce experienced in LGS construction techniques in certain regions. Traditional construction methods remain deeply entrenched in many markets, and shifting industry practices requires substantial investment in training and education for architects, engineers, and construction crews. Overcoming this inertia and building a proficient workforce takes time and resources, which can slow down the wider acceptance and implementation of LGS. Additionally, regional variations in building codes and standards can create fragmentation in the market, requiring specific certifications and adaptations that add complexity and cost to LGS deployment across different geographies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Steel) | -1.3% | Global, particularly manufacturing and import-dependent regions | Short to Medium Term (2025-2029) |

| Limited Awareness and Skilled Labor Shortage | -0.9% | Emerging economies, certain traditional construction markets | Medium Term (2026-2031) |

| Perceived High Initial Cost Compared to Traditional Methods | -0.7% | Globally, for small-scale projects | Short Term (2025-2027) |

| Complexity of Design and Engineering for Non-Standard Projects | -0.5% | Global, for bespoke architectural designs | Medium to Long Term (2027-2033) |

Light Gauge Steel Market Opportunities Analysis

The Light Gauge Steel (LGS) market is poised to capitalize on several significant opportunities driven by evolving construction needs and technological advancements. A key opportunity lies in the expanding scope of modular and off-site construction. As the industry increasingly seeks faster, more cost-effective, and less disruptive building methods, LGS emerges as an ideal material for prefabricated modules and panels. This trend extends beyond residential structures to include commercial buildings, schools, and healthcare facilities, where rapid deployment and minimized on-site disruption are critical. The inherent precision and lightweight nature of LGS make it exceptionally well-suited for manufacturing components in controlled factory environments, enhancing quality and reducing project timelines.

Furthermore, the growing global emphasis on sustainable infrastructure and disaster-resilient construction presents a substantial opportunity for LGS. Governments and private entities are investing in buildings that can withstand extreme weather events, earthquakes, and fires, areas where LGS offers superior performance due to its inherent strength, non-combustibility, and seismic resistance. The recyclability of steel and the potential for LGS to contribute to energy-efficient building envelopes also align with green building certifications and increasing environmental regulations, opening doors in markets prioritizing ecological impact. Moreover, diversification into niche applications such as temporary housing, disaster relief structures, and cold storage facilities can unlock new revenue streams, leveraging LGS's rapid deployability and adaptability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Modular and Off-Site Construction | +1.5% | Global, particularly high-cost labor markets and urban areas | Short to Medium Term (2025-2029) |

| Increasing Focus on Sustainable and Resilient Building Solutions | +1.2% | Developed nations, disaster-prone regions | Medium to Long Term (2027-2033) |

| Growth in Developing Economies and Emerging Markets | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Short to Long Term (2025-2033) |

| Renovation and Retrofitting of Existing Structures | +0.8% | North America, Europe, mature urban centers | Medium Term (2026-2031) |

Light Gauge Steel Market Challenges Impact Analysis

The Light Gauge Steel (LGS) market faces several challenges that require strategic responses from industry players to sustain growth. One significant hurdle is the intense competition from traditional construction materials like wood, concrete, and masonry, which have deeply established supply chains, long-standing industry familiarity, and often lower upfront costs. Overcoming this ingrained preference and demonstrating the long-term value proposition of LGS, including its speed of construction, durability, and sustainability benefits, remains a persistent challenge for market penetration. Educating stakeholders on the total cost of ownership rather than just initial material cost is crucial to address this.

Another challenge stems from the need for specialized design and engineering expertise specific to LGS construction. Unlike conventional methods, LGS systems require precise calculations and detailed fabrication plans, which can sometimes be perceived as more complex or less flexible for highly customized architectural designs. This necessitates continuous training for engineers and architects and the development of more user-friendly design software. Furthermore, supply chain disruptions, such as those witnessed recently due to global events, can significantly impact the availability and cost of steel, directly affecting LGS manufacturers' ability to meet demand and maintain competitive pricing. Navigating these external volatilities while ensuring consistent supply is a critical operational challenge for the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Traditional Construction Materials (Wood, Concrete) | -1.1% | Global, particularly in residential and small commercial sectors | Short to Medium Term (2025-2029) |

| Perception of Limited Design Flexibility for Architects | -0.8% | Globally, among design professionals | Medium Term (2026-2031) |

| Supply Chain Vulnerabilities and Logistics Costs | -0.6% | Global, especially regions reliant on imports | Short Term (2025-2027) |

| Varying Building Codes and Regulatory Approvals | -0.4% | Regional, for international market entry | Long Term (2028-2033) |

Light Gauge Steel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Light Gauge Steel (LGS) market, offering critical insights into its current dynamics, historical performance, and future growth projections. The scope encompasses detailed market sizing, segmentation analysis by material type, application, and end-use, alongside a thorough examination of regional landscapes. The report meticulously identifies key market trends, drivers, restraints, opportunities, and challenges influencing market trajectory, providing stakeholders with a holistic view to inform strategic decision-making. It also includes an extensive competitive landscape analysis, profiling leading companies and their strategic initiatives within the LGS industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 32.5 billion |

| Market Forecast in 2033 | USD 53.0 billion |

| Growth Rate | 6.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Steel Frame Solutions, Kingspan Light + Air, Hadley Group, Metroll Australia, ClarkDietrich Building Systems, Framecad, Vertex Building Systems, EOS Facades, Alukönigstahl, BSF Components, BlueScope Steel, ArcelorMittal, SSAB, Tata Steel, Nippon Steel Corporation, POSCO, JFE Steel Corporation, China Baowu Steel Group, Nucor Corporation, Commercial Metals Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Light Gauge Steel (LGS) market is comprehensively segmented to provide a granular understanding of its diverse applications and product categories, enabling stakeholders to pinpoint specific growth avenues and market niches. This detailed segmentation facilitates a precise analysis of demand patterns and technological adoption across various construction scenarios. Understanding these segments is crucial for manufacturers to tailor their product offerings and for construction firms to optimize material selection for specific project requirements, from large-scale commercial developments to individual residential units, ensuring efficiency and compliance with building standards.

The market is primarily analyzed across product type, application, and end-use vertical. Each segment provides unique insights into the specific needs and trends driving the adoption of LGS components. For instance, the demand for LGS studs and joists typically correlates with residential and light commercial framing, while panels and trusses are increasingly favored for their speed and efficiency in modular construction. Similarly, the end-use segmentation highlights the growing penetration of LGS beyond traditional residential buildings into commercial, industrial, and institutional sectors, indicating a broadening scope of applications and an expanding market footprint.

- By Product Type:

- Light Gauge Steel Studs: Vertical framing members primarily used in non-load-bearing walls, partitions, and curtain walls for their dimensional stability and fire resistance.

- Light Gauge Steel Joists: Horizontal structural members used in floor and roof systems, providing lightweight support with high strength-to-weight ratios.

- Light Gauge Steel Trusses: Prefabricated triangular frameworks used for long spans in roofing and flooring systems, offering design flexibility and efficient load distribution.

- Light Gauge Steel Panels: Factory-assembled wall, floor, or roof sections that can incorporate insulation and sheathing, significantly accelerating on-site construction.

- Others: Includes a variety of specialized LGS components such as LGS sheets, bracing, purlins, and girts used for specific structural or non-structural applications.

- By Application:

- Structural Framing: Encompasses the primary load-bearing and non-load-bearing frameworks of buildings.

- Load-Bearing Structures: Main structural elements supporting the building's weight, including roofs, floors, and multiple stories.

- Non-Load-Bearing Structures: Internal walls and partitions that do not carry vertical loads but provide separation and stability.

- Infill Walls: Non-structural walls used to fill in between main structural elements, often found in high-rise buildings where the primary structure is concrete or hot-rolled steel.

- Roofing: LGS components used for roof framing, including trusses and purlins, offering lightweight and durable solutions.

- Flooring: LGS joists and deck systems used to create robust and level floor surfaces.

- Partitions: Internal dividing walls, typically non-load-bearing, for flexible space planning and fire compartmentation.

- Façades: External building envelopes, where LGS offers lightweight and durable framing for various cladding materials.

- Structural Framing: Encompasses the primary load-bearing and non-load-bearing frameworks of buildings.

- By End-Use Vertical:

- Residential: Construction of homes and multi-unit dwellings.

- Single-Family Homes: Detached or semi-detached housing units.

- Multi-Family Dwellings: Apartments, condominiums, and townhouses.

- Commercial: Buildings designed for business activities.

- Offices: Corporate buildings and business parks.

- Retail Spaces: Shopping malls, stores, and commercial complexes.

- Hospitality: Hotels, motels, and resorts.

- Healthcare Facilities: Hospitals, clinics, and medical centers.

- Industrial: Structures for manufacturing, storage, and processing.

- Warehouses: Storage facilities for goods and materials.

- Factories: Manufacturing plants and production facilities.

- Institutional: Buildings for public or organizational services.

- Schools: Educational institutions from primary to higher education.

- Government Buildings: Administrative offices and public service structures.

- Infrastructure Projects: Large-scale public works such as bridges, public transport stations, and specialized facilities where lightweight and durable solutions are needed.

- Residential: Construction of homes and multi-unit dwellings.

Regional Highlights

The global Light Gauge Steel (LGS) market exhibits distinct regional dynamics, driven by varying economic conditions, construction trends, regulatory frameworks, and technological adoption rates. Each region contributes uniquely to the market's overall growth, with some leading in innovation and adoption, while others present significant untapped potential. Understanding these regional nuances is crucial for strategic market entry and expansion.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market for Light Gauge Steel, primarily due to rapid urbanization, significant infrastructure development, and a burgeoning population across countries like China, India, and Southeast Asian nations. The increasing adoption of prefabricated and modular construction techniques to meet the escalating housing and commercial demands, coupled with government initiatives for smart cities and affordable housing, is fueling the demand for LGS. China, in particular, is a dominant force, driven by massive construction projects and a push towards sustainable building. India and other developing economies are also witnessing rising adoption due to the benefits of speed, cost-efficiency, and resilience offered by LGS.

- North America: North America represents a mature yet continually growing market for LGS. The region, particularly the United States and Canada, benefits from a strong emphasis on sustainable construction, energy efficiency regulations, and the increasing preference for off-site construction methods to address labor shortages and enhance construction quality. Renovation and remodeling activities, alongside new commercial and institutional projects, are key drivers. The widespread acceptance of BIM and advanced construction technologies further supports the integration and growth of LGS in this region. The need for structures resilient to seismic activity and extreme weather also bolsters LGS adoption.

- Europe: The European market for Light Gauge Steel is characterized by stringent environmental regulations, a strong focus on energy-efficient buildings, and a mature construction industry that increasingly embraces modern methods of construction (MMC). Countries like the UK, Germany, and Scandinavia are at the forefront of adopting LGS for its thermal performance, recyclability, and speed of assembly. The drive towards reducing construction waste and carbon footprints, coupled with the precision offered by LGS in prefabrication, makes it an attractive choice for both new builds and retrofitting projects across residential, commercial, and public sectors.

- Middle East and Africa (MEA): This region is experiencing considerable growth in the LGS market, primarily driven by large-scale infrastructural investments, diversification efforts away from oil economies, and ambitious urban development projects, especially in the GCC countries. The rapid pace of construction required for new cities, tourism hubs, and residential complexes makes LGS an appealing solution for its speed and efficiency. Additionally, the need for robust and climate-resilient structures in challenging environmental conditions contributes to the demand. Africa's emerging economies, with their urgent need for housing and commercial infrastructure, also present long-term growth opportunities.

- Latin America: The Latin American market for LGS is in an evolving phase, showing promising growth potential. Countries like Brazil, Mexico, and Chile are witnessing increased adoption due to urbanization trends, a growing middle class, and the need for more efficient and resilient construction methods. The region's vulnerability to seismic activity and natural disasters also makes LGS an attractive option for its structural integrity. As economic conditions stabilize and construction practices modernize, the demand for LGS is expected to rise, particularly in residential and light commercial applications.

Top Key Players:

The market research report covers the analysis of key stake holders of the Light Gauge Steel Market. Some of the leading players profiled in the report include -- Steel Frame Solutions

- Kingspan Light + Air

- Hadley Group

- Metroll Australia

- ClarkDietrich Building Systems

- Framecad

- Vertex Building Systems

- EOS Facades

- Alukönigstahl

- BSF Components

- BlueScope Steel

- ArcelorMittal

- SSAB

- Tata Steel

- Nippon Steel Corporation

- POSCO

- JFE Steel Corporation

- China Baowu Steel Group

- Nucor Corporation

- Commercial Metals Company

Frequently Asked Questions:

What is Light Gauge Steel (LGS) construction?

Light Gauge Steel (LGS) construction utilizes cold-formed steel components, typically thin-gauge galvanized steel sheets, to create structural framing members like studs, joists, and trusses. These components are precision-engineered and often prefabricated off-site, allowing for rapid and accurate on-site assembly. LGS is known for its high strength-to-weight ratio, durability, fire resistance, and recyclability, making it a versatile and sustainable choice for various building types.What are the primary benefits of using Light Gauge Steel in construction?

The primary benefits of using Light Gauge Steel include faster construction times due to prefabrication and lightweight components, enhanced durability and resistance to pests, rot, and fire, and superior seismic performance. LGS also offers excellent dimensional stability, leading to fewer call-backs and reduced material waste, contributing to more sustainable building practices. Its high strength-to-weight ratio allows for lighter foundations and more flexible designs.How does Light Gauge Steel contribute to sustainable building practices?

Light Gauge Steel significantly contributes to sustainable building practices through several key aspects. Steel is a highly recyclable material, with LGS components often containing a high percentage of recycled content and being 100% recyclable at the end of a building's life. Its precision manufacturing reduces on-site waste, and the superior thermal performance achievable with LGS framing can lead to more energy-efficient buildings, lowering operational energy consumption and carbon emissions.In which applications is Light Gauge Steel most commonly used?

Light Gauge Steel is most commonly used in a wide range of applications including residential buildings (single-family homes, multi-family dwellings), commercial structures (offices, retail, hotels, healthcare facilities), and institutional buildings (schools). It is highly favored for infill walls, structural framing, roofing, flooring, and especially in modular and prefabricated construction projects where speed, precision, and efficiency are paramount.What is the market growth outlook for Light Gauge Steel?

The Light Gauge Steel market is projected for robust growth, with a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market size is expected to grow from USD 32.5 billion in 2025 to USD 53.0 billion by 2033. This growth is driven by increasing adoption of modular construction, rising demand for sustainable and resilient building solutions, and continuous technological advancements in manufacturing and design.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted