LEO Satellite Communication Market

LEO Satellite Communication Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703654 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

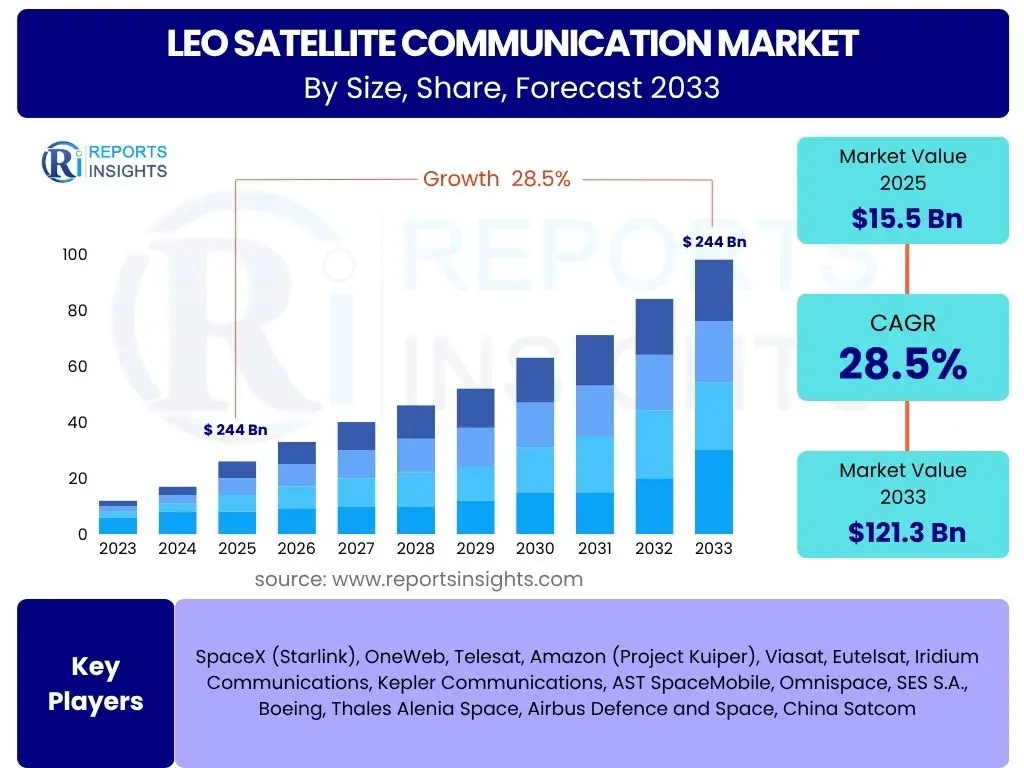

LEO Satellite Communication Market Size

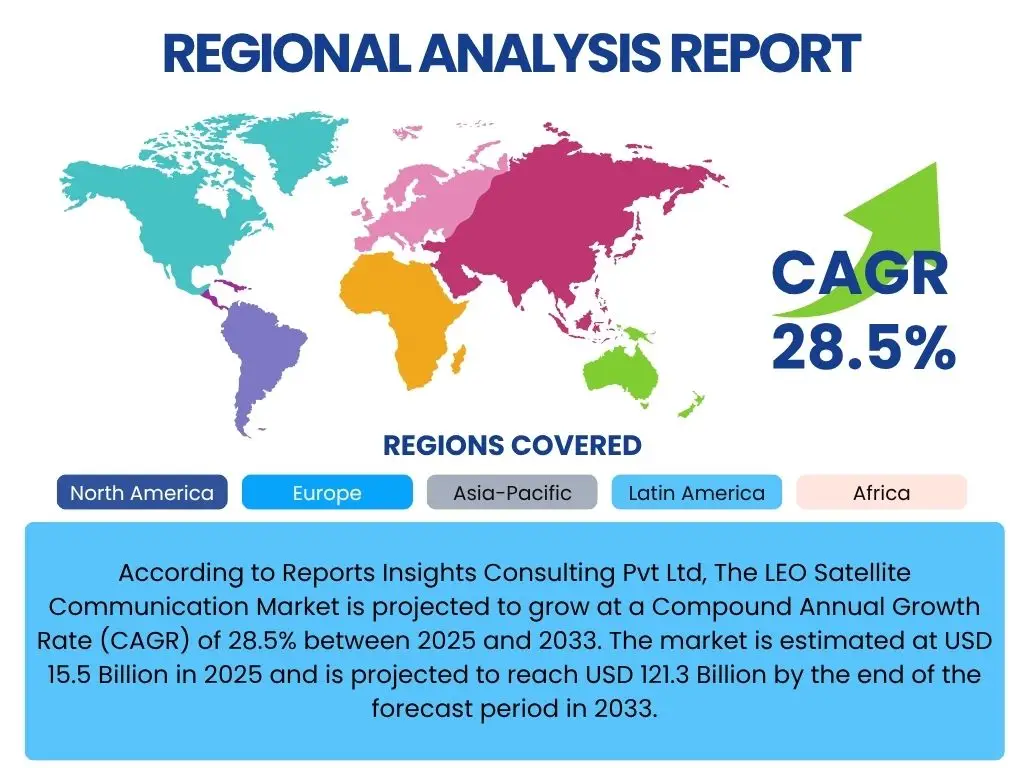

According to Reports Insights Consulting Pvt Ltd, The LEO Satellite Communication Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. The market is estimated at USD 15.5 Billion in 2025 and is projected to reach USD 121.3 Billion by the end of the forecast period in 2033.

Key LEO Satellite Communication Market Trends & Insights

The LEO satellite communication market is undergoing rapid evolution, driven by a confluence of technological advancements and increasing global demand for connectivity. Key inquiries from stakeholders often revolve around the overarching shifts in technology, regulatory frameworks, and market adoption that are shaping this emerging sector. The pervasive need for high-speed, low-latency internet access, particularly in underserved and remote areas, is a fundamental driver, pushing the development and deployment of vast LEO constellations. This global demand is further augmented by the growing reliance on connected devices and the expansion of the Internet of Things (IoT), which requires robust and ubiquitous communication infrastructure.

Another significant trend is the increasing diversification of applications beyond traditional broadband. Enterprises are exploring LEO solutions for secure corporate networks, real-time asset tracking, and remote operations in sectors such as agriculture, mining, and maritime. Governments and defense organizations are also recognizing the strategic importance of LEO constellations for national security, disaster response, and enhanced military communications, leading to significant investments and partnerships. Furthermore, the advancements in satellite manufacturing, miniaturization, and launch capabilities are enabling more cost-effective deployment and replenishment of LEO constellations, accelerating market expansion and fostering a competitive environment among new entrants and established players.

The market also exhibits a strong trend towards integration with terrestrial networks, leading to hybrid communication solutions that leverage the strengths of both satellite and ground-based infrastructure. This includes seamless handovers between cellular and satellite networks for mobile users, and the deployment of satellite backhaul for 5G networks in areas where fiber optic infrastructure is impractical. Such integration is critical for achieving true global connectivity and ensuring service continuity across diverse geographic landscapes, ultimately enhancing the value proposition of LEO satellite communication.

- Proliferation of large LEO satellite constellations for global broadband internet.

- Increasing demand for low-latency, high-speed connectivity in remote and underserved areas.

- Integration of LEO satellite services with 5G networks and terrestrial infrastructure.

- Advancements in satellite miniaturization and cost-effective launch capabilities.

- Growing adoption of LEO solutions for enterprise, government, and defense applications.

- Development of direct-to-device (D2D) connectivity capabilities.

- Rising investments in ground segment infrastructure and user terminals.

- Emergence of new business models, including satellite-as-a-service.

AI Impact Analysis on LEO Satellite Communication

Common user questions regarding AI's impact on LEO satellite communication frequently focus on how artificial intelligence can enhance operational efficiency, optimize network performance, and enable new service capabilities. There is considerable interest in AI's role in managing the immense complexity of large LEO constellations, which involve thousands of interconnected satellites, dynamic link management, and real-time resource allocation. Users are keen to understand how AI can automate tasks, reduce operational costs, and improve the overall reliability and resilience of satellite networks, particularly in response to fluctuating demand and unforeseen events.

AI is poised to revolutionize several critical aspects of LEO satellite communication. It can significantly enhance network orchestration by intelligently routing traffic, managing beamforming, and dynamically assigning bandwidth based on real-time demand and channel conditions. This intelligent management ensures optimal utilization of satellite resources and delivers a more consistent and high-quality user experience. Furthermore, AI algorithms can be employed for predictive maintenance of satellites and ground infrastructure, identifying potential failures before they occur and minimizing downtime. This predictive capability extends to anomaly detection, allowing operators to quickly identify and address unusual network behavior or potential security threats.

Beyond network management, AI also plays a crucial role in the development and deployment phases. Machine learning models can be used to optimize satellite design, propulsion systems, and constellation configurations for improved coverage and efficiency. On the user side, AI can personalize service offerings, optimize terminal performance, and enhance cybersecurity measures to protect sensitive data transmitted via LEO networks. The integration of AI tools is not merely about automation; it is about creating more adaptive, resilient, and intelligent LEO communication systems that can evolve with changing user needs and technological landscapes, ultimately driving greater market adoption and value.

- Enhanced network orchestration and dynamic resource allocation through machine learning.

- Predictive maintenance and anomaly detection for satellites and ground infrastructure.

- Optimized satellite traffic management and routing algorithms.

- Improved cybersecurity and threat detection within satellite networks.

- Automated constellation management and orbital debris avoidance.

- AI-driven beamforming and interference mitigation techniques.

- Personalized service delivery and user experience optimization.

- Data analytics for performance monitoring and strategic decision-making.

Key Takeaways LEO Satellite Communication Market Size & Forecast

Key inquiries from users regarding the LEO Satellite Communication market size and forecast often center on the primary growth drivers, the critical factors contributing to market expansion, and the long-term viability of this burgeoning sector. Stakeholders are particularly interested in understanding the magnitude of investment required, the potential for market disruption across various industries, and the specific technological advancements that underpin the projected growth. There is also significant focus on the competitive landscape and the strategies employed by key market players to capture market share and sustain growth in a rapidly evolving environment.

The forecast for the LEO satellite communication market indicates a robust and sustained growth trajectory, largely fueled by the insatiable global demand for ubiquitous, high-speed internet connectivity, especially in areas historically underserved by terrestrial infrastructure. The proliferation of mega-constellations is significantly expanding coverage and capacity, making LEO services increasingly accessible and competitive. Moreover, the inherent low-latency advantage of LEO satellites positions them as a compelling alternative or complement to traditional geostationary satellite services and even fiber optic networks for certain applications, driving adoption across diverse end-use sectors.

A crucial takeaway is the increasing vertical integration within the industry, with companies not only launching satellites but also developing ground infrastructure, user terminals, and offering end-to-end services. This integrated approach aims to streamline operations, reduce costs, and enhance the overall customer experience. Furthermore, government initiatives and defense applications are emerging as substantial growth catalysts, as nations recognize the strategic importance of resilient and independent satellite communication capabilities. The market's future will be characterized by continued technological innovation, fierce competition, and a broadening array of applications, cementing LEO satellite communication as a fundamental component of the global digital infrastructure.

- The LEO satellite communication market is poised for exceptional growth, driven by global connectivity demand.

- Significant market expansion is attributed to the deployment of large constellations and technological advancements.

- Low-latency capabilities are a primary differentiator, opening new application avenues.

- Increased investment in both space and ground segments indicates long-term industry commitment.

- Strategic importance for government and defense sectors is a strong growth driver.

- Integration with terrestrial networks is critical for broader market adoption and service delivery.

- Competitive landscape is intensifying with new entrants and established telecommunication firms.

LEO Satellite Communication Market Drivers Analysis

The expansion of the LEO satellite communication market is primarily propelled by the escalating global demand for high-speed, low-latency internet access, particularly in remote and underserved regions. Traditional terrestrial infrastructure often struggles to reach these areas efficiently, making LEO satellites a viable and often superior alternative. The proliferation of digital technologies, remote work trends, and the increasing reliance on online services across various industries further amplify this demand. Additionally, the inherent advantages of LEO constellations, such as reduced signal delay and enhanced bandwidth capabilities compared to geostationary satellites, make them highly attractive for modern communication needs, including real-time applications and cloud services.

Another significant driver is the continuous innovation in satellite technology and launch capabilities. Advancements in miniaturization, mass production techniques for satellites, and the development of reusable rockets have drastically reduced the cost of deploying large constellations. This cost efficiency allows for more frequent launches and the rapid scaling of network capacity, accelerating market penetration. Furthermore, the growing adoption of LEO services by various enterprise sectors, including maritime, aviation, energy, and agriculture, for applications like asset tracking, remote monitoring, and secure communications, is contributing substantially to market growth. Governments and defense organizations are also increasingly investing in LEO systems for enhanced national security, disaster response, and robust military communication networks, recognizing their resilience and global coverage.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Global Broadband Connectivity | +8.5% | Global, particularly Emerging Markets (Africa, LATAM, APAC) | Short to Long Term (2025-2033) |

| Technological Advancements in Satellite and Launch Systems | +7.0% | North America, Europe, Asia Pacific | Short to Medium Term (2025-2030) |

| Growing Adoption Across Enterprise and Government Sectors | +6.5% | North America, Europe, Middle East | Medium to Long Term (2026-2033) |

| Low Latency and High Throughput Capabilities of LEO Networks | +4.0% | Global, especially for real-time applications | Short to Long Term (2025-2033) |

| Government Initiatives and Funding for Satellite Communication | +2.5% | China, India, USA, EU Member States | Medium Term (2027-2032) |

LEO Satellite Communication Market Restraints Analysis

Despite its significant growth potential, the LEO satellite communication market faces several inherent restraints that could impact its expansion. One of the primary concerns is the substantial capital expenditure required for the initial deployment and ongoing maintenance of large LEO constellations. This includes the costs associated with satellite manufacturing, launch services, ground station infrastructure, and the development of user terminals. Such high investment thresholds can deter new entrants and put financial strain on existing players, potentially slowing down the pace of network expansion and service rollout, especially in price-sensitive markets. Furthermore, the complexity of managing thousands of interconnected satellites, ensuring their optimal performance, and mitigating operational risks adds to the financial burden and operational challenges.

Another significant restraint is the increasing issue of space debris and orbital congestion. The sheer number of LEO satellites being launched raises concerns about potential collisions, which could generate more debris and further exacerbate the problem, posing a threat to operational satellites and future missions. Regulatory bodies worldwide are grappling with establishing comprehensive and enforceable frameworks to manage orbital traffic and mitigate debris, but a lack of unified international policy could lead to inefficiencies or even unsafe conditions. Additionally, the intensive energy consumption of ground stations and the environmental impact of frequent rocket launches are drawing scrutiny, potentially leading to stricter environmental regulations that could increase operational costs and complexity for LEO service providers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Operational Costs | -3.5% | Global, particularly for new entrants | Short to Medium Term (2025-2030) |

| Increasing Space Debris and Orbital Congestion | -2.8% | Global, affecting all satellite operators | Medium to Long Term (2027-2033) |

| Regulatory Complexities and Spectrum Allocation Challenges | -2.0% | Global, varying by regional policies | Short to Medium Term (2025-2030) |

| Competition from Terrestrial and GEO Satellite Networks | -1.5% | Developed Markets (North America, Europe) | Short to Medium Term (2025-2030) |

| Cybersecurity Threats and Data Privacy Concerns | -1.0% | Global, impacting user adoption | Ongoing (2025-2033) |

LEO Satellite Communication Market Opportunities Analysis

The LEO satellite communication market presents numerous opportunities for substantial growth and innovation, particularly in expanding global internet access. The significant digital divide, especially in remote, rural, and developing regions, represents a vast untapped market for LEO broadband services. These areas often lack adequate terrestrial infrastructure, making LEO satellites a critical solution for bridging the connectivity gap and enabling economic and social development. As more of the world comes online, the demand for reliable and high-speed satellite internet will continue to escalate, providing a long-term growth trajectory for LEO service providers. Furthermore, the continued reduction in launch costs and satellite manufacturing expenses, coupled with advancements in terminal technology, will make these services more affordable and accessible to a wider demographic, broadening the market base considerably.

Beyond traditional internet connectivity, the burgeoning demand for specialized applications across various industries offers significant opportunities. The maritime, aviation, and logistics sectors require robust, always-on communication for operations, safety, and tracking, which LEO networks can uniquely provide at sea, in the air, and across remote land routes. The integration of LEO capabilities with 5G networks presents a tremendous opportunity for enhanced backhaul solutions, enabling comprehensive 5G coverage in areas where fiber deployment is unfeasible or cost-prohibitive. Moreover, the growth of the Internet of Things (IoT) and machine-to-machine (M2M) communication, requiring reliable connectivity for smart devices and sensors globally, creates a fertile ground for LEO satellite services. The development of direct-to-device (D2D) communication, bypassing the need for separate terminals, could further revolutionize mobile connectivity and unlock new market segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Bridging the Global Digital Divide in Remote Areas | +7.0% | Africa, Latin America, Southeast Asia, Rural North America | Long Term (2026-2033) |

| Integration with 5G Networks for Backhaul and Complementary Coverage | +6.0% | Global, particularly emerging 5G markets | Medium to Long Term (2027-2033) |

| Growth of IoT and M2M Communication Across Industries | +5.5% | Global, especially industrial, agriculture, logistics | Medium Term (2026-2031) |

| Direct-to-Device (D2D) Connectivity for Mobile Phones | +4.0% | Global Mobile Market | Medium to Long Term (2028-2033) |

| Emergence of Specialized Verticals (e.g., Maritime, Aviation, Defense) | +3.5% | Global specialized industries | Short to Medium Term (2025-2030) |

LEO Satellite Communication Market Challenges Impact Analysis

The LEO satellite communication market, while promising, faces several significant challenges that could impede its projected growth and widespread adoption. A prominent challenge is the intense competition and market saturation, particularly as numerous companies rush to deploy their own constellations. This crowded environment can lead to price wars, reduced profitability, and a struggle for market differentiation. Furthermore, the high upfront investment coupled with the long gestation period for returns can strain financial resources, especially for companies that may not achieve sufficient subscriber numbers quickly enough. The need for continuous innovation in satellite technology and service offerings to stay competitive also poses a substantial research and development challenge.

Another critical challenge revolves around regulatory complexities and the allocation of limited radio frequency spectrum. As more constellations are deployed, managing interference and ensuring equitable access to spectrum becomes increasingly difficult, requiring sophisticated international cooperation and robust regulatory frameworks. Additionally, the development and mass production of affordable, efficient, and user-friendly ground terminals represent a significant hurdle. These terminals need to be capable of tracking fast-moving LEO satellites and maintaining seamless connectivity, while also being cost-effective enough for widespread consumer adoption. Supply chain constraints for critical components and specialized manufacturing capabilities can also impact the timely deployment of both satellites and ground equipment, affecting overall market readiness and scalability. Cybersecurity threats, given the global and interconnected nature of LEO networks, pose an ongoing challenge requiring constant vigilance and robust protective measures.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Market Saturation | -3.0% | Global, affecting all operators | Short to Medium Term (2025-2030) |

| Development and Cost of Affordable User Terminals | -2.5% | Global, impacting consumer adoption | Short to Medium Term (2025-2030) |

| Regulatory and Spectrum Management Complexities | -2.0% | Global, requiring international cooperation | Ongoing (2025-2033) |

| Orbital Debris Mitigation and Space Sustainability | -1.8% | Global, affecting all space operations | Medium to Long Term (2027-2033) |

| Cybersecurity Risks and Network Vulnerabilities | -1.0% | Global, impacting trust and reliability | Ongoing (2025-2033) |

LEO Satellite Communication Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the LEO Satellite Communication market, covering current market dynamics, key trends, growth drivers, restraints, opportunities, and challenges. The scope extends to a detailed market size estimation and forecast, segmented by orbit type, application, end-user, and component, across major global regions and key countries. It offers strategic insights into the competitive landscape, profiling key market players and their recent developments, product portfolios, and strategic initiatives. The report also includes an impact analysis of artificial intelligence on the LEO satellite communication ecosystem and addresses frequently asked questions to provide a holistic view for stakeholders seeking to understand and capitalize on this rapidly evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.5 Billion |

| Market Forecast in 2033 | USD 121.3 Billion |

| Growth Rate | 28.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SpaceX (Starlink), OneWeb, Telesat, Amazon (Project Kuiper), Viasat, Eutelsat, Iridium Communications, Kepler Communications, AST SpaceMobile, Omnispace, SES S.A., Boeing, Thales Alenia Space, Airbus Defence and Space, China Satcom |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The LEO Satellite Communication market is meticulously segmented to provide a granular view of its diverse components, applications, and end-users, enabling a precise understanding of market dynamics and opportunities across various niches. This segmentation helps in identifying specific growth pockets and tailoring strategies for different market needs, ranging from the core satellite and ground infrastructure to the varied services delivered. Understanding these segments is crucial for stakeholders to pinpoint investment areas, develop targeted solutions, and anticipate future shifts in demand, ensuring a comprehensive market penetration strategy.

The market is primarily divided by component into Satellite, Ground Segment, and Services, reflecting the entire ecosystem from space-based assets to terrestrial infrastructure and the actual communication offerings. Further segmentation by orbit type differentiates between Narrowband LEO and Broadband LEO, each serving distinct application requirements. The application segment details the diverse uses, including critical areas like Backhaul, Broadband Internet, and IoT and M2M, highlighting the versatility of LEO technology. Finally, the end-user segmentation separates the market into Commercial (spanning various industries), Government and Defense, and Consumer segments, showcasing the broad adoption across different sectors and individual users.

- By Component: Satellite (Payload, Bus, Solar Panel, Battery, Propulsion System, Others), Ground Segment (Ground Station, Antenna, Transceiver, Network Management System), Services (Connectivity Services, Value-added Services, Managed Services).

- By Orbit Type: Narrowband LEO, Broadband LEO.

- By Application: Backhaul, Broadband Internet, IoT & M2M, Voice & Data Communication, Earth Observation, Navigation & Positioning, Others.

- By End User: Commercial (Maritime, Aviation, Energy, Agriculture, Logistics, Telecom), Government & Defense, Consumer.

Regional Highlights

North America stands as a dominant force in the LEO Satellite Communication market, driven by significant investments from private companies and robust government support. The region is home to several leading LEO constellation operators and boasts a strong ecosystem of aerospace manufacturers, technology developers, and launch service providers. High demand for advanced communication solutions across urban, rural, and remote areas, coupled with a proactive regulatory environment, fosters innovation and accelerated deployment. The increasing adoption of LEO services by the defense sector for secure and resilient communication, alongside growing commercial applications in sectors like agriculture, mining, and smart infrastructure, further solidifies its market leadership.

Europe is rapidly emerging as a key region in the LEO satellite communication market, propelled by strong governmental initiatives and increased private sector investment in next-generation space technologies. The European Union's focus on digital transformation and ubiquitous connectivity, exemplified by projects aimed at reducing the digital divide, creates a conducive environment for LEO service adoption. Countries like the UK, France, and Germany are at the forefront of satellite manufacturing and research, contributing significantly to technological advancements. The region's strong maritime and aviation sectors are also driving demand for LEO-based communication services, highlighting Europe's commitment to leveraging space for economic growth and strategic autonomy.

The Asia Pacific (APAC) region is projected to exhibit the highest growth rate in the LEO satellite communication market, driven by rapidly expanding economies, a vast population, and a significant digital divide in many countries. Governments across the region, particularly in China, India, and Southeast Asian nations, are heavily investing in space infrastructure and satellite communication to boost economic development, enhance connectivity in remote areas, and support smart city initiatives. The increasing adoption of IoT and M2M applications, coupled with growing demand for high-speed broadband in rural and island communities, presents immense opportunities. The region's expanding manufacturing capabilities and growing consumer base are also key factors contributing to its accelerated market expansion.

Latin America is a burgeoning market for LEO satellite communication, primarily due to the vast geographical expanses and challenging terrain that make terrestrial infrastructure deployment difficult and costly. The region's significant unserved and underserved populations represent a substantial market opportunity for LEO broadband providers aiming to bridge the connectivity gap and promote digital inclusion. Governments in countries like Brazil, Mexico, and Argentina are recognizing the transformative potential of satellite internet for education, healthcare, and economic development in remote areas. As LEO services become more affordable and accessible, Latin America is expected to witness substantial growth in both consumer and enterprise adoption, addressing critical connectivity needs across diverse sectors.

The Middle East and Africa (MEA) region offers a unique and compelling growth trajectory for the LEO satellite communication market, primarily due to large unserved populations, challenging geographies for terrestrial infrastructure, and ambitious national digitalization agendas. Countries in the Middle East, with substantial investments in technology and infrastructure, are exploring LEO solutions for smart city development, oil and gas operations, and defense applications. In Africa, LEO satellites present a transformative solution for bringing affordable internet to remote villages, supporting rural education, and enabling mobile backhaul in areas lacking fiber optic networks. The region's increasing mobile penetration and growing demand for digital services underscore the immense potential for LEO communication to catalyze economic growth and social development across the continent.

- North America: Market leader with strong investment, advanced R&D, and significant defense adoption.

- Europe: Rapid growth driven by government initiatives, digital inclusion efforts, and strong industrial base.

- Asia Pacific: Highest growth potential due to large underserved populations, government support, and increasing digitalization.

- Latin America: Emerging market with high demand for rural connectivity and digital inclusion.

- Middle East and Africa (MEA): Significant opportunities in unserved areas, smart city development, and critical infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the LEO Satellite Communication Market.- SpaceX (Starlink)

- OneWeb

- Telesat

- Amazon (Project Kuiper)

- Viasat

- Eutelsat

- Iridium Communications

- Kepler Communications

- AST SpaceMobile

- Omnispace

- SES S.A.

- Boeing

- Thales Alenia Space

- Airbus Defence and Space

- China Satcom

- Lynk Global

- Kineis

- Swarm Technologies (SpaceX Subsidiary)

- Inmarsat (Viasat Subsidiary)

- Gilat Satellite Networks

Frequently Asked Questions

Analyze common user questions about the LEO Satellite Communication market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is LEO satellite communication?

LEO satellite communication involves the use of satellites orbiting Earth at a low altitude (typically 160 to 2,000 kilometers) to provide telecommunication services. These satellites offer significantly lower latency compared to traditional geostationary satellites due to their closer proximity to Earth, making them ideal for high-speed internet, real-time data transfer, and applications requiring minimal delay.

How do LEO satellites provide internet connectivity?

LEO satellites provide internet connectivity by forming large constellations that blanket the Earth with coverage. User terminals on the ground communicate with the closest satellite, which then relays the data to a ground station connected to the internet backbone. The low altitude ensures a shorter signal path, leading to faster data transmission and a more responsive user experience for activities like streaming, gaming, and video conferencing.

What are the primary advantages of LEO satellite internet over traditional options?

The primary advantages of LEO satellite internet include significantly lower latency compared to geostationary satellites, higher bandwidth capabilities, and global coverage that can reach remote and underserved areas where terrestrial infrastructure is impractical. This enables reliable, high-speed internet access in locations that previously had limited or no connectivity, fostering digital inclusion and supporting diverse applications.

What are the main challenges facing the LEO satellite communication market?

The main challenges facing the LEO satellite communication market include the substantial capital expenditure required for constellation deployment and maintenance, the increasing concern over space debris and orbital congestion, regulatory complexities concerning spectrum allocation, and the need to develop cost-effective and efficient user terminals for widespread adoption. Intense competition among multiple operators also presents a significant hurdle.

How is AI impacting LEO satellite communication networks?

AI is significantly impacting LEO satellite communication networks by enabling enhanced network orchestration, dynamic resource allocation, and predictive maintenance. AI algorithms optimize traffic routing, manage beamforming, and identify potential failures, leading to improved network efficiency, reliability, and security. AI also supports automated constellation management and personalized service delivery, ultimately making LEO networks more intelligent and resilient.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted