Laboratory Centrifuge Market

Laboratory Centrifuge Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700241 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

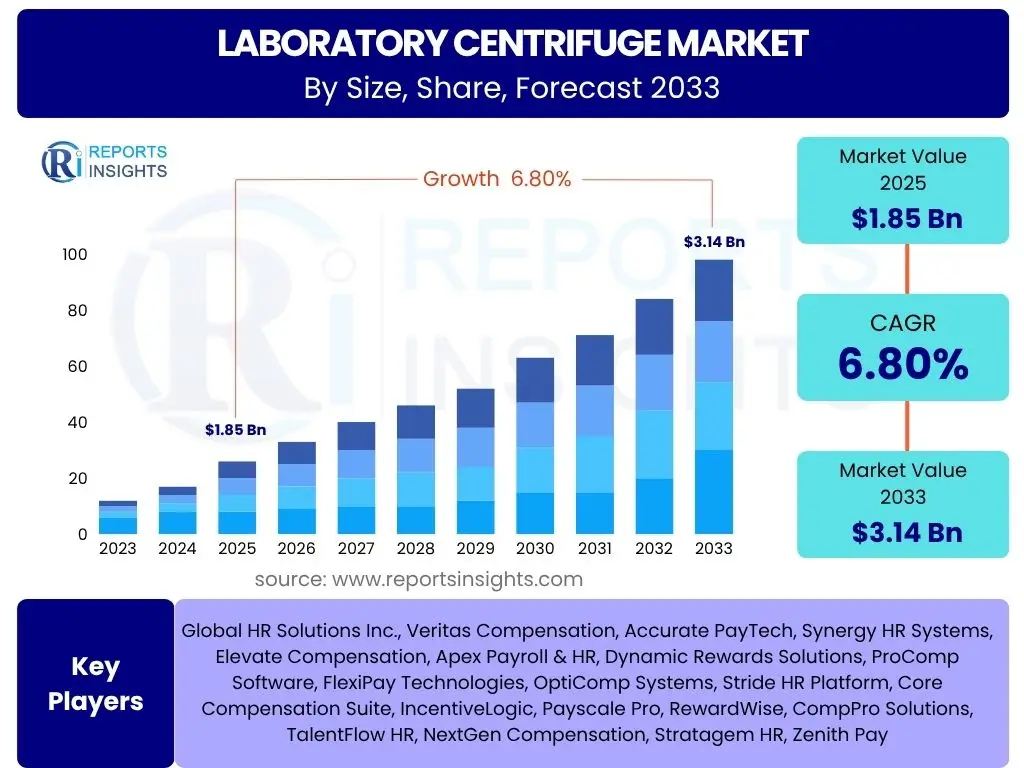

Laboratory Centrifuge Market is projected to grow at a Compound annual growth rate (CAGR) of 6.8% between 2025 and 2033, current valued at USD 1.85 billion in 2025 and is projected to reach USD 3.14 billion by 2033 at the end of the forecast period.

Key Laboratory Centrifuge Market Trends & Insights

The laboratory centrifuge market is experiencing dynamic shifts driven by several crucial trends. Advancements in automation and integration are enabling centrifuges to be seamlessly incorporated into larger laboratory workflows, reducing manual intervention and enhancing throughput. Miniaturization and portability are emerging trends, particularly for point-of-care diagnostics and field research, allowing for more flexible and decentralized laboratory operations. The focus on energy efficiency and sustainable designs is also gaining traction, aligning with global environmental initiatives and reducing operational costs for laboratories. Furthermore, the increasing demand for high-speed and ultra-centrifuges capable of handling diverse sample types, from DNA and RNA to viral particles and proteins, reflects the intensifying complexity of life science research. Finally, the integration of smart features and IoT capabilities is transforming centrifuges into intelligent devices that can be monitored remotely, predict maintenance needs, and provide real-time data for enhanced efficiency and reliability.

- Increasing integration of automation and robotics in laboratory processes.

- Growing demand for high-speed and ultra-centrifuges for advanced research.

- Emergence of portable and compact centrifuge designs for diverse applications.

- Focus on energy-efficient and sustainable laboratory equipment.

- Rising adoption of smart centrifuges with IoT capabilities for remote monitoring.

- Development of specialized rotors and accessories for niche applications.

- Shift towards digital data management and connectivity in laboratories.

- Emphasis on precision and reproducibility in sample separation.

- Expansion of biotechnology and pharmaceutical research activities.

- Innovations in material science leading to lighter and stronger centrifuge components.

AI Impact Analysis on Laboratory Centrifuge

Artificial Intelligence (AI) is set to significantly revolutionize the laboratory centrifuge market, moving beyond traditional mechanical functions to intelligent operations. AI algorithms can optimize centrifuge protocols by analyzing sample characteristics and desired separation outcomes, leading to more efficient and precise separations and reducing user error. Predictive maintenance, powered by AI, can monitor equipment performance in real-time, anticipate potential failures, and schedule maintenance proactively, thereby minimizing downtime and extending the lifespan of the instruments. Furthermore, AI can aid in data analysis generated from centrifugation processes, such as the purity and yield of separated components, providing deeper insights for research and quality control. This integration also paves the way for greater automation, with AI-driven systems autonomously handling sample loading, centrifugation, and unloading, enhancing throughput and reducing manual labor requirements in high-volume laboratories. The ability of AI to learn from vast datasets of experimental conditions and results will lead to increasingly optimized and customized centrifugation solutions, adapting to the complex and evolving needs of modern scientific research.

- AI-driven optimization of centrifugation protocols for enhanced efficiency and precision.

- Implementation of predictive maintenance using AI to minimize downtime and extend equipment life.

- Enhanced data analysis and interpretation of centrifugation results through AI algorithms.

- Automation of sample handling and processing, leading to higher throughput.

- Development of smart centrifuges with self-learning capabilities for adaptive operations.

- Improved quality control and error detection through AI-powered anomaly detection.

- Facilitation of remote monitoring and control of centrifuge operations.

- Personalized centrifugation solutions based on AI analysis of specific experimental needs.

Key Takeaways Laboratory Centrifuge Market Size & Forecast

- The global Laboratory Centrifuge Market is projected to grow from USD 1.85 billion in 2025 to USD 3.14 billion by 2033.

- The market is anticipated to exhibit a robust Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period from 2025 to 2033.

- Significant growth is attributed to increasing research and development activities in life sciences and biotechnology.

- Technological advancements, including automation and smart features, are key contributors to market expansion.

- Emerging economies are expected to offer substantial growth opportunities for market players.

Laboratory Centrifuge Market Drivers Analysis

The laboratory centrifuge market is primarily propelled by a confluence of factors, central among them being the escalating investment in life science research and development. This surge in R&D, particularly in biotechnology, pharmaceuticals, and diagnostics, necessitates advanced separation technologies to isolate and purify cells, proteins, nucleic acids, and other biological components critical for drug discovery, disease diagnosis, and vaccine development. Concurrently, the increasing prevalence of chronic and infectious diseases globally drives the demand for rapid and accurate diagnostic tests, many of which rely on centrifugation for sample preparation. Furthermore, continuous technological advancements in centrifuge design, such as higher speeds, greater capacity, improved energy efficiency, and integrated smart features, enhance their utility and broaden their application spectrum, making them indispensable tools in modern laboratories. The expansion of clinical laboratories and academic research institutions worldwide also directly translates into higher demand for these essential pieces of equipment, underpinning the market's consistent growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Investment in Life Science R&D | +1.5% | North America, Europe, Asia Pacific | Short-term to Long-term |

| Growth in Biotechnology and Pharmaceutical Industries | +1.2% | Global, particularly developed economies | Short-term to Long-term |

| Rising Prevalence of Chronic and Infectious Diseases | +1.0% | Global | Mid-term to Long-term |

| Technological Advancements in Centrifuge Design | +1.0% | Global | Short-term to Mid-term |

| Expansion of Clinical Diagnostic Laboratories and Academic Institutions | +0.8% | Emerging economies, developing regions | Mid-term to Long-term |

Laboratory Centrifuge Market Restraints Analysis

Despite the robust growth drivers, the laboratory centrifuge market faces certain restraints that could temper its expansion. One significant challenge is the high initial capital investment required for advanced and high-capacity centrifuges, which can be prohibitive for smaller laboratories, academic institutions with limited budgets, or facilities in developing regions. This high cost extends beyond procurement to include ongoing maintenance, specialized accessories, and energy consumption, contributing to the overall operational expenditure. Furthermore, the stringent regulatory landscape governing laboratory equipment, particularly in clinical and diagnostic applications, imposes significant compliance burdens on manufacturers, leading to extended product development cycles and higher costs. The increasing availability of alternative or complementary separation technologies, such as filtration, chromatography, and magnetic bead separation, could also present a competitive threat, offering solutions that may be more suitable or cost-effective for specific applications. Moreover, the demand for highly skilled personnel to operate and maintain sophisticated centrifuges, coupled with the potential for human error in sample handling, can also act as a limiting factor in certain settings.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment and Maintenance Costs | -0.9% | Developing regions, small and medium-sized laboratories globally | Short-term to Mid-term |

| Stringent Regulatory Landscape | -0.7% | North America, Europe | Short-term to Long-term |

| Availability of Alternative Separation Technologies | -0.5% | Global | Mid-term to Long-term |

| Need for Skilled Personnel and Potential for Human Error | -0.4% | Global | Short-term to Mid-term |

Laboratory Centrifuge Market Opportunities Analysis

Opportunities in the laboratory centrifuge market are abundant, driven by evolving scientific frontiers and global healthcare needs. The burgeoning field of personalized medicine, requiring precise separation of biological samples for targeted therapies and diagnostics, presents a significant avenue for growth, demanding specialized and high-precision centrifuges. The rapid expansion of life science research infrastructure in emerging economies, fueled by government investments and a growing scientific community, offers untapped market potential for manufacturers. Furthermore, the trend towards miniaturization and portability in laboratory equipment opens new markets in point-of-care testing, remote field research, and mobile diagnostic units, requiring compact and robust centrifuge solutions. The integration of advanced technologies like IoT, AI, and automation in centrifuges, leading to "smart centrifuges," can create new product categories and value propositions, enhancing operational efficiency and data management for laboratories. Finally, the increasing focus on cell and gene therapies, which critically depend on the efficient and gentle separation of delicate biological components, will further drive demand for specialized centrifuge technologies, fostering innovation and market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Personalized Medicine and Cell & Gene Therapy | +1.3% | North America, Europe, parts of Asia Pacific | Mid-term to Long-term |

| Growth in Emerging Economies and Developing Research Infrastructure | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Mid-term to Long-term |

| Development of Miniaturized and Portable Centrifuges | +0.9% | Global, especially for field and point-of-care applications | Short-term to Mid-term |

| Integration of IoT, AI, and Automation in Centrifuges | +0.8% | Developed markets initially, then global | Short-term to Mid-term |

Laboratory Centrifuge Market Challenges Impact Analysis

The laboratory centrifuge market faces several challenges that require strategic navigation by manufacturers and stakeholders. Supply chain disruptions, exacerbated by global events, can significantly impact the availability of raw materials and components, leading to production delays and increased costs. The intense market competition, characterized by numerous domestic and international players, exerts downward pressure on pricing and necessitates continuous innovation and differentiation to maintain market share. Meeting evolving regulatory standards, especially for devices used in clinical diagnostics and drug development, can be complex and time-consuming, requiring significant investment in compliance and quality control. Furthermore, the disposal of hazardous biological waste generated during centrifugation processes presents environmental and safety concerns, requiring adherence to strict guidelines and investment in proper waste management solutions. Ensuring product reliability and durability under demanding laboratory conditions, coupled with the need for after-sales support and service, also poses a continuous challenge for manufacturers aiming to build long-term customer trust and loyalty.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Raw Material Volatility | -0.6% | Global | Short-term |

| Intense Market Competition and Pricing Pressures | -0.5% | Global | Short-term to Mid-term |

| Adherence to Evolving Regulatory Standards | -0.4% | Developed markets (North America, Europe) | Mid-term to Long-term |

| Disposal of Hazardous Biological Waste | -0.3% | Global | Ongoing |

| Ensuring Product Reliability and Durability | -0.3% | Global | Ongoing |

Laboratory Centrifuge Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Laboratory Centrifuge Market, offering a detailed understanding of its current landscape, historical performance, and future growth trajectory. The report encompasses key market dynamics, including drivers, restraints, opportunities, and challenges, providing a holistic view for strategic decision-making. It features extensive segmentation analysis across various parameters, alongside a thorough regional breakdown to identify key growth pockets and emerging trends. The study also profiles leading market players, offering insights into their competitive strategies, product portfolios, and recent developments, ensuring a complete and actionable overview for industry stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.14 Billion |

| Growth Rate | 6.8% from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Danaher Corporation, Eppendorf AG, Thermo Fisher Scientific Inc, Sigma Laborzentrifugen GmbH, Kubota Corporation, Andreas Hettich GmbH & Co KG, NuAire Inc, HERMLE Labortechnik GmbH, Centurion Scientific Ltd, Scilogex LLC, Benchmark Scientific Inc, Labconco Corporation, Cole-Parmer Instrument Company LLC, QIAGEN N.V., Bio-Rad Laboratories Inc, Sartorius AG, Agilent Technologies Inc, Shimadzu Corporation, Hitachi Koki Co Ltd, Narang Medical Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global laboratory centrifuge market is meticulously segmented to provide a granular understanding of its diverse components and evolving demand patterns. This segmentation offers valuable insights into specific product preferences, application areas, and end-user requirements, enabling stakeholders to identify niche markets and tailor their strategies effectively. From the various product types, ranging from compact microcentrifuges essential for molecular biology to high-capacity floor-standing units used in large-scale bioproduction, each category caters to distinct laboratory needs. The market is also differentiated by rotor types, including fixed-angle for pelleting and swing-bucket for density gradient separations, reflecting varying procedural demands. Further segmentation by speed and capacity allows for a detailed analysis of equipment capabilities, while application-based divisions, spanning clinical diagnostics to advanced proteomics and genomics, highlight the critical role centrifuges play across the entire spectrum of life science research and healthcare. Finally, end-user segmentation provides clarity on demand drivers from hospitals, pharmaceutical companies, academic institutions, and blood banks, showcasing the broad utility of these instruments in various professional settings.

- By Product Type:

- Microcentrifuges: Small, high-speed centrifuges for small sample volumes.

- Benchtop Centrifuges: Compact, versatile centrifuges for various lab tasks, suitable for small to medium volumes.

- Floor-standing Centrifuges: Large, high-capacity centrifuges, often refrigerated, used for large sample volumes or high-speed applications.

- Ultracentrifuges: Extremely high-speed centrifuges used for separating macromolecules and subcellular components.

- Specialty Centrifuges: Includes specific designs such as Blood Bank Centrifuges, Cytocentrifuges for cell smear preparation, and Refrigerated Centrifuges for temperature-sensitive samples.

- By Rotor Type:

- Fixed-angle Rotors: Hold tubes at a fixed angle, ideal for pelleting.

- Swing-bucket Rotors: Tubes swing out to a horizontal position, good for density gradients and large volumes.

- Vertical Rotors: Tubes are aligned vertically, often used in ultracentrifugation for rapid separation.

- By Speed:

- Low-speed Centrifuges: Operate at relatively low RPMs, suitable for routine separations.

- Mid-speed Centrifuges: Offer moderate speeds for a broader range of applications.

- High-speed Centrifuges: Capable of higher speeds for finer separations.

- Ultra-speed Centrifuges: Reach very high speeds for molecular and subcellular separations.

- By Capacity:

- Low Capacity: Designed for small numbers of tubes or microplates.

- Medium Capacity: Accommodate a moderate number of tubes or bottles.

- High Capacity: Built for large-scale processing of many tubes or large volume bottles.

- By Application:

- Clinical Diagnostics: Sample preparation for blood tests, urinalysis, etc.

- Research and Academia: Used in basic and applied scientific research across various disciplines.

- Biotechnology and Pharmaceutical Production: For cell harvesting, protein purification, vaccine development.

- Blood Component Separation: Essential for separating plasma, serum, red blood cells, etc., in blood banks.

- Proteomics: Isolation and purification of proteins for study.

- Genomics: Separation of DNA/RNA and related components.

- Cell Culture: Separation of cells from culture media.

- Microbiology: Separation of bacteria, viruses, and other microorganisms.

- Other Applications: Includes environmental testing, food and beverage analysis, and forensic science.

- By End User:

- Hospitals and Diagnostic Laboratories: For routine clinical testing and specialized diagnostics.

- Pharmaceutical and Biotechnology Companies: Engaged in drug discovery, development, and production.

- Academic and Research Institutes: Universities and research centers conducting scientific studies.

- Blood Banks: For processing and preparing blood components.

- Contract Research Organizations (CROs): Provide research services to pharmaceutical and biotech industries.

- Others: Includes forensic labs, environmental testing labs, and industrial research facilities.

Regional Highlights

The global laboratory centrifuge market exhibits varied growth patterns and demand characteristics across different geographical regions, influenced by healthcare infrastructure, research funding, and industrial development.- North America: This region holds a significant share in the laboratory centrifuge market, driven by substantial investments in life science research, a robust biotechnology and pharmaceutical industry, and the presence of numerous well-established academic and clinical research institutions. The region's advanced healthcare infrastructure, high adoption rate of new technologies, and a strong emphasis on personalized medicine and genomics contribute to its leading position. The United States, in particular, dominates due to extensive R&D expenditures and a large number of diagnostic laboratories.

- Europe: Europe represents another major market, fueled by strong government support for scientific research, a mature pharmaceutical sector, and the presence of leading research universities. Countries like Germany, the UK, and France are key contributors, characterized by stringent quality standards and a focus on innovative healthcare solutions. The increasing prevalence of chronic diseases and an aging population also necessitate advanced diagnostic capabilities, thereby driving the demand for laboratory centrifuges.

- Asia Pacific (APAC): The Asia Pacific region is anticipated to be the fastest-growing market for laboratory centrifuges during the forecast period. This rapid growth is attributed to increasing healthcare expenditures, expanding biotechnology and pharmaceutical industries, and a surge in government funding for research and development activities in countries like China, India, Japan, and South Korea. The rising number of academic institutions and clinical diagnostic laboratories, coupled with a large patient pool, further propels market expansion. Economic development and improving healthcare access are key factors contributing to the region's dynamic growth.

- Latin America: This region demonstrates steady growth, driven by improving healthcare infrastructure, increasing awareness of chronic diseases, and a growing focus on biomedical research. Brazil and Mexico are leading countries in this region, with growing investments in the pharmaceutical and biotechnology sectors. However, budget constraints in public healthcare systems can sometimes moderate the adoption of high-end equipment.

- Middle East and Africa (MEA): The MEA region is witnessing gradual growth in the laboratory centrifuge market, primarily due to increasing government initiatives to modernize healthcare facilities and boost medical tourism. Investments in research and development, particularly in GCC countries, are also contributing to market expansion. However, the market's growth is often constrained by political instability, economic fluctuations, and less developed research infrastructure in some parts of the region.

Top Key Players:

The market research report covers the analysis of key stake holders of the Laboratory Centrifuge Market. Some of the leading players profiled in the report include -- Danaher Corporation

- Eppendorf AG

- Thermo Fisher Scientific Inc

- Sigma Laborzentrifugen GmbH

- Kubota Corporation

- Andreas Hettich GmbH & Co KG

- NuAire Inc

- HERMLE Labortechnik GmbH

- Centurion Scientific Ltd

- Scilogex LLC

- Benchmark Scientific Inc

- Labconco Corporation

- Cole-Parmer Instrument Company LLC

- QIAGEN N.V.

- Bio-Rad Laboratories Inc

- Sartorius AG

- Agilent Technologies Inc

- Shimadzu Corporation

- Hitachi Koki Co Ltd

- Narang Medical Limited

Frequently Asked Questions:

What is a laboratory centrifuge used for?

A laboratory centrifuge is a vital piece of equipment used to separate components of a liquid mixture based on density. It applies centrifugal force to rapidly spin samples, causing denser particles to settle at the bottom of the tube while lighter components remain in suspension or form layers above. This process is crucial for isolating cells, organelles, proteins, nucleic acids, and other biological or chemical components from complex mixtures, making it indispensable across various scientific disciplines.

What are the different types of laboratory centrifuges?

Laboratory centrifuges are categorized primarily by their speed and capacity. Common types include microcentrifuges for small sample volumes, benchtop centrifuges for general lab work, and floor-standing centrifuges for larger volumes or high-speed applications. Ultracentrifuges are used for extremely high-speed separations of macromolecules. Additionally, specialized centrifuges exist for specific applications, such as refrigerated centrifuges for temperature-sensitive samples, blood bank centrifuges for blood component separation, and cytocentrifuges for preparing cell smears.

What factors are driving the growth of the laboratory centrifuge market?

The growth of the laboratory centrifuge market is primarily driven by increasing investments in life science research and development, particularly in the biotechnology and pharmaceutical sectors. The rising prevalence of chronic and infectious diseases necessitates advanced diagnostic capabilities, further boosting demand. Continuous technological advancements, including the integration of automation and smart features, also enhance the utility and efficiency of centrifuges. Additionally, the expansion of clinical diagnostic laboratories and academic research institutions worldwide significantly contributes to market expansion.

How is AI impacting the laboratory centrifuge market?

Artificial Intelligence (AI) is transforming the laboratory centrifuge market by enabling more intelligent and efficient operations. AI algorithms can optimize centrifugation protocols for improved precision and throughput. They facilitate predictive maintenance, minimizing downtime by anticipating equipment failures. Furthermore, AI enhances data analysis from centrifugation processes, providing deeper insights for quality control and research. This integration also supports greater automation in sample handling, leading to reduced manual labor and higher laboratory efficiency.

What are the key regional markets for laboratory centrifuges?

The key regional markets for laboratory centrifuges include North America, Europe, and Asia Pacific. North America leads due to significant R&D investments and a mature biotechnology industry. Europe is a strong market driven by robust research funding and pharmaceutical sector growth. Asia Pacific is the fastest-growing region, propelled by increasing healthcare expenditures, expanding biotechnology industries, and growing government support for scientific research in countries like China and India. Latin America and the Middle East & Africa also show promising growth due to improving healthcare infrastructure.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted