Insulated Metal Panel Market

Insulated Metal Panel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700133 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

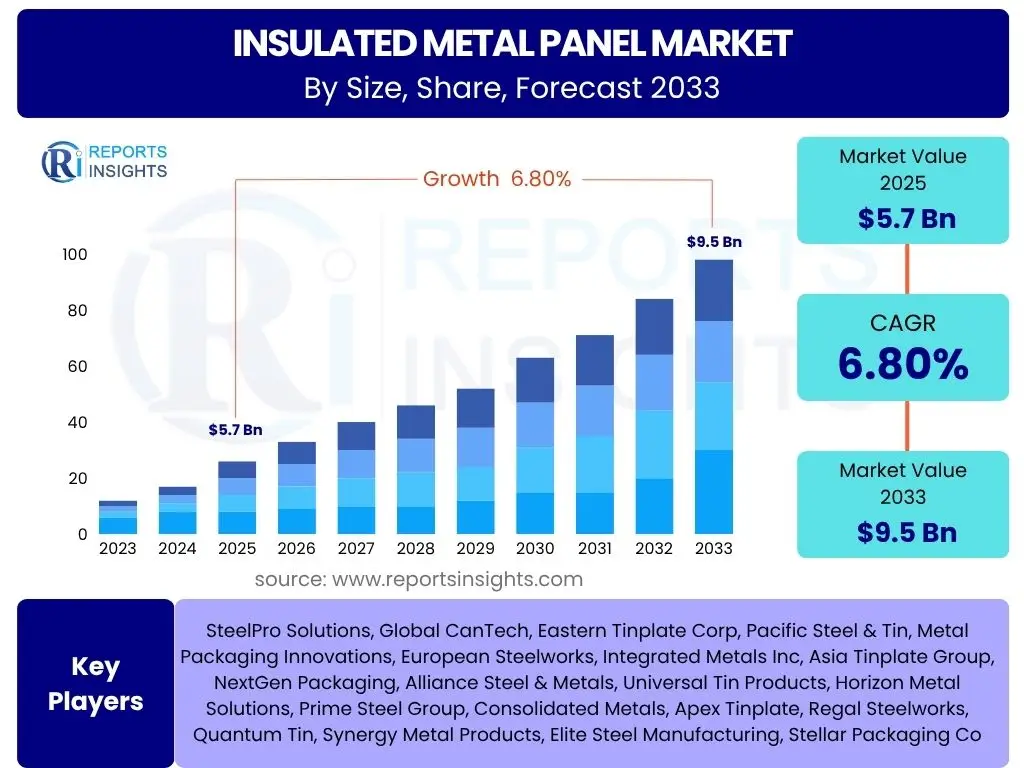

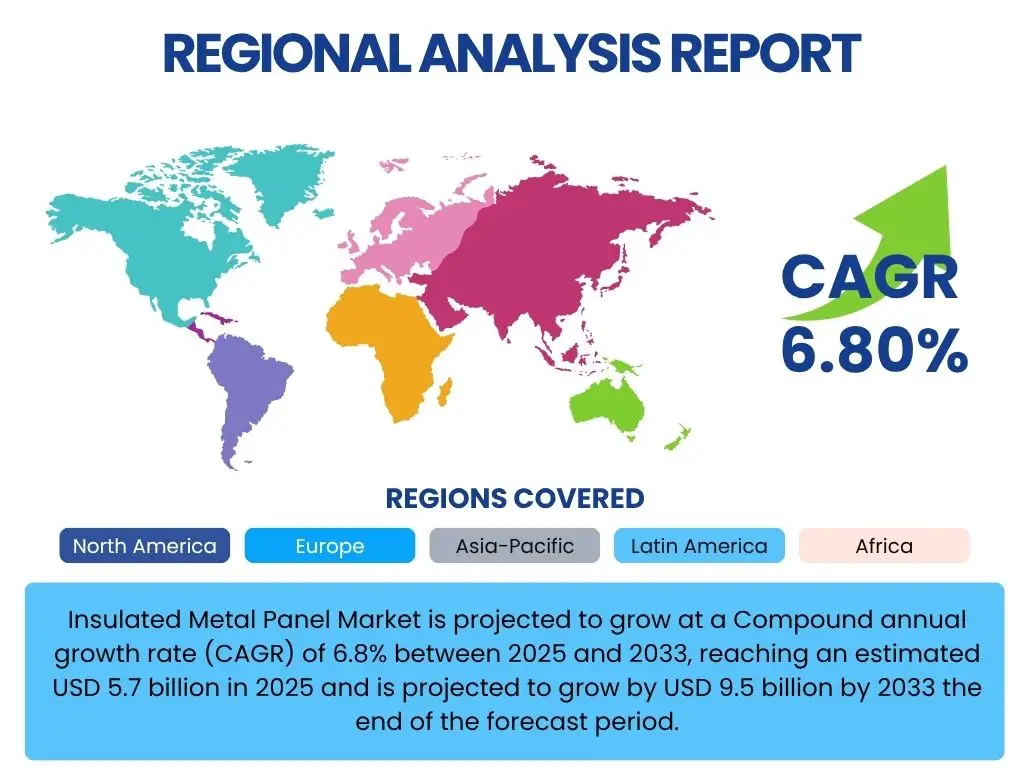

Insulated Metal Panel Market is projected to grow at a Compound annual growth rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 5.7 billion in 2025 and is projected to grow by USD 9.5 billion by 2033 the end of the forecast period.

Key Insulated Metal Panel Market Trends & Insights

The Insulated Metal Panel (IMP) market is currently shaped by a confluence of evolving building codes, a heightened focus on energy efficiency, and a growing appreciation for sustainable construction materials. Architectural design trends are increasingly favoring lightweight, high-performance envelopes that offer accelerated construction schedules and superior thermal performance. This demand is driving innovation in panel design, core materials, and connection systems, leading to more versatile and aesthetically pleasing solutions for a diverse range of building types. Furthermore, the imperative to reduce operational energy consumption in both new and existing structures is making IMPs a preferred choice due to their inherent insulation properties and air-tightness capabilities. The market also observes a steady shift towards modular and prefabricated construction techniques, where IMPs play a critical role in expediting project timelines and ensuring consistent quality. This trend is complemented by advancements in digital design and manufacturing, allowing for greater customization and precision in panel fabrication. The increasing adoption of green building certifications globally further reinforces the market's trajectory towards high-performance, environmentally responsible materials.

- Rising demand for energy-efficient building solutions.

- Increasing adoption of green building certifications and sustainable construction practices.

- Growth in cold storage and controlled environment agriculture facilities.

- Technological advancements leading to enhanced panel performance and aesthetics.

- Accelerated construction timelines driven by prefabrication and modular building trends.

- Urbanization and infrastructure development projects driving commercial and industrial construction.

- Renovation and retrofitting of existing structures to improve thermal performance.

AI Impact Analysis on Insulated Metal Panel

Artificial intelligence (AI) is poised to revolutionize various aspects of the Insulated Metal Panel (IMP) market, from design and manufacturing to supply chain management and onsite installation. In the design phase, AI-powered generative design tools can rapidly optimize panel configurations, material usage, and thermal performance based on specific project requirements, leading to more efficient and cost-effective solutions. Predictive analytics, driven by AI, can enhance raw material procurement by forecasting demand and supply chain disruptions, thereby minimizing lead times and inventory costs for manufacturers. During the manufacturing process, AI can be integrated into quality control systems, using computer vision to detect defects in real-time, ensuring higher product consistency and reducing waste. Furthermore, AI algorithms can optimize production schedules and machinery maintenance, improving overall operational efficiency and reducing downtime. On the construction site, AI-driven robotics may assist in precise panel installation, enhancing safety and accelerating project completion. The integration of AI in building information modeling (BIM) can also facilitate seamless coordination between IMP manufacturers, architects, and contractors, streamlining the entire project lifecycle and reducing potential errors.

- AI-driven optimization of panel design and material selection for enhanced thermal performance.

- Predictive maintenance for manufacturing equipment, reducing downtime and improving efficiency.

- AI-powered quality control systems ensuring consistent panel integrity and defect detection.

- Optimized supply chain logistics and inventory management through demand forecasting.

- Enhanced project planning and scheduling, integrating IMP installation into BIM models.

- Potential for robotic assistance in precise and rapid on-site panel installation.

- Data analytics for market trend identification and customer preference analysis.

Key Takeaways Insulated Metal Panel Market Size & Forecast

- The global Insulated Metal Panel (IMP) market is projected to expand significantly, driven by stringent energy efficiency regulations and a rising emphasis on sustainable construction.

- The market is expected to grow from approximately USD 5.7 billion in 2025 to USD 9.5 billion by 2033, indicating a robust Compound Annual Growth Rate (CAGR) of 6.8%.

- North America and Europe are currently dominant markets, characterized by advanced building codes and a strong focus on green initiatives, while Asia Pacific is emerging as the fastest-growing region due to rapid urbanization and infrastructure development.

- Growth is particularly strong in the commercial, industrial, and cold storage sectors, where IMPs offer superior thermal performance and rapid construction benefits.

- Key opportunities lie in retrofitting existing buildings for energy efficiency and the increasing adoption of prefabricated and modular construction techniques.

- Challenges such as raw material price volatility and high initial investment costs remain, yet ongoing technological advancements and increasing awareness of long-term benefits are expected to mitigate these factors.

Insulated Metal Panel Market Drivers Analysis

The Insulated Metal Panel (IMP) market is experiencing significant growth propelled by several key drivers, primarily centered around global efforts towards energy conservation and sustainable development. Increasingly stringent building codes and regulations across various regions mandate higher thermal performance standards for both new constructions and renovations, making IMPs an attractive solution due to their superior insulation properties. The rising awareness among building owners and developers about the long-term operational cost savings associated with energy-efficient envelopes further fuels demand. Beyond energy efficiency, the inherent advantages of IMPs, such as their lightweight nature, high strength-to-weight ratio, and rapid installation capabilities, contribute to reduced construction timelines and labor costs, which are critical factors in accelerating project completion and improving return on investment. Furthermore, the expanding industrial and commercial sectors, including the burgeoning cold chain logistics and controlled environment agriculture industries, require precise temperature control, for which IMPs are optimally suited. The market also benefits from the growing trend towards aesthetically versatile building materials that offer a clean, modern appearance while ensuring structural integrity and environmental performance. These combined factors create a compelling case for the widespread adoption of IMPs across diverse construction applications, driving their market expansion globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Energy-Efficient Buildings | +2.5% | Global, particularly North America, Europe, and developed APAC economies | Long-term (2025-2033) |

| Growth in Cold Storage & Controlled Environment Facilities | +1.8% | Global, with strong growth in Asia Pacific and emerging economies | Medium to Long-term (2025-2033) |

| Accelerated Construction Timelines & Prefabrication Trends | +1.2% | North America, Europe, and rapidly urbanizing regions in APAC | Medium-term (2025-2029) |

| Adoption of Green Building Codes and Certifications | +1.0% | Europe, North America, and increasingly in emerging markets | Long-term (2025-2033) |

| Renovation and Retrofitting of Existing Structures | +0.8% | Developed economies with aging infrastructure (North America, Western Europe) | Long-term (2025-2033) |

Insulated Metal Panel Market Restraints Analysis

Despite robust growth, the Insulated Metal Panel (IMP) market faces certain restraints that could temper its expansion. One significant hurdle is the relatively high initial capital cost associated with IMPs compared to conventional building materials. While IMPs offer substantial long-term energy savings and reduced construction timelines, the upfront investment can be a deterrent for budget-constrained projects or developers seeking the lowest immediate expenditure. Another key restraint is the volatility in raw material prices, particularly for steel, aluminum, and insulation core materials like polyisocyanurate (PIR) or mineral wool. Fluctuations in these commodity prices can impact manufacturing costs and, consequently, the final price of IMPs, affecting market stability and profitability for manufacturers. Additionally, the complexity of installation for certain architectural designs or highly customized IMP applications can require specialized labor and expertise, potentially limiting widespread adoption in regions with less developed construction capabilities or skilled workforce shortages. While IMPs offer superior performance, the lack of widespread awareness or established distribution channels in some emerging markets also acts as a restraint, requiring significant investment in market education and infrastructure development. Addressing these cost, supply chain, and skill-related challenges will be crucial for the sustained and accelerated growth of the IMP market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Cost Compared to Traditional Materials | -1.5% | Global, particularly sensitive in price-conscious emerging markets | Long-term (2025-2033) |

| Volatility in Raw Material Prices (Steel, Aluminum, Insulation Cores) | -1.0% | Global, impacts manufacturers and end-users | Medium-term (2025-2029) |

| Lack of Awareness and Established Distribution Channels in Developing Regions | -0.7% | Latin America, Middle East, and parts of Asia Pacific and Africa | Long-term (2025-2033) |

| Skilled Labor Requirements for Complex Installations | -0.5% | Global, particularly in regions with labor shortages | Medium to Long-term (2025-2033) |

Insulated Metal Panel Market Opportunities Analysis

The Insulated Metal Panel (IMP) market is brimming with promising opportunities that are set to drive its future growth and innovation. A significant avenue for expansion lies in the increasing global focus on retrofitting existing commercial, industrial, and institutional buildings to enhance their energy efficiency and meet modern sustainability standards. IMPs offer an ideal solution for upgrading aging building envelopes, providing superior thermal performance with minimal disruption and rapid installation, thus reducing the operational carbon footprint of older structures. The expanding scope of applications beyond traditional commercial and industrial buildings presents another substantial opportunity. This includes the growing adoption of IMPs in residential construction, particularly for high-performance homes and modular housing, where their benefits of quick erection, consistent quality, and energy efficiency are highly valued. Furthermore, technological advancements in IMP manufacturing, such as the development of smarter panels with integrated sensors for building performance monitoring or enhanced fire-resistant core materials, open new market segments and improve product value propositions. The ongoing global trend towards urbanization and the development of new infrastructure projects, particularly in emerging economies, provide fertile ground for IMP market penetration, as these panels support rapid, sustainable, and cost-effective construction methodologies. Embracing digitalization in design (BIM), manufacturing, and supply chain management will also unlock efficiencies and customization capabilities, further expanding the market's reach.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Retrofitting and Renovation of Existing Buildings for Energy Efficiency | +1.8% | Developed economies (North America, Europe, Japan) | Long-term (2025-2033) |

| Expansion into New Applications (e.g., Residential, Agricultural, Data Centers) | +1.5% | Global, particularly in rapidly evolving economies | Medium to Long-term (2025-2033) |

| Technological Advancements in Panel Design and Materials | +1.2% | Global, driven by R&D in leading manufacturing hubs | Long-term (2025-2033) |

| Increased Infrastructure Development in Emerging Economies | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long-term (2025-2033) |

Insulated Metal Panel Market Challenges Impact Analysis

While opportunities abound, the Insulated Metal Panel (IMP) market also navigates several challenges that demand strategic responses from industry players. One significant challenge is the intense competition from alternative building materials that, while perhaps not offering the same thermal performance, may be perceived as more cost-effective for certain applications. This necessitates continuous innovation and value communication from IMP manufacturers to highlight the long-term benefits and total cost of ownership. Another prevailing challenge is the fluctuating regulatory landscape and varying building codes across different regions and countries. Adhering to diverse standards for fire safety, structural integrity, and environmental performance can add complexity and cost to manufacturing and distribution. Furthermore, disruptions in the global supply chain, exacerbated by geopolitical tensions or unforeseen events, can impact the availability and pricing of critical raw materials, leading to production delays and increased costs. The need for specialized installation techniques and skilled labor also presents a challenge, as a shortage of trained professionals can hinder project timelines and quality. Overcoming these challenges will require robust supply chain management, adaptability to regulatory changes, and investments in installer training and technological advancements to streamline production and installation processes, ensuring the sustained competitiveness and growth of the IMP market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Alternative Building Materials (e.g., Tilt-up Concrete, Masonry) | -0.8% | Global, especially in cost-sensitive segments | Long-term (2025-2033) |

| Varying Regulatory Standards and Building Codes Across Regions | -0.6% | Global, particularly challenging for international expansion | Long-term (2025-2033) |

| Global Supply Chain Disruptions and Logistics Challenges | -0.4% | Global, impacting manufacturing and delivery | Short to Medium-term (2025-2027) |

| Perception of High Initial Cost vs. Long-Term Value | -0.3% | Global, requires market education | Long-term (2025-2033) |

Insulated Metal Panel Market - Updated Report Scope

The updated report scope for the Insulated Metal Panel (IMP) market provides a comprehensive analysis of the industry's historical performance, current landscape, and future growth trajectories. This detailed study encompasses crucial market dynamics, including key trends, drivers, restraints, opportunities, and challenges that shape the market's evolution. It offers in-depth segmentation analysis across various parameters such as core material, facing material, end-use application, and building type, providing granular insights into the market's structure and potential. The report also highlights regional performance, identifying key growth hubs and their contributing factors. A thorough examination of the competitive landscape, featuring profiles of leading market players, offers strategic insights into market positioning, innovations, and collaborative initiatives. This robust research serves as an invaluable resource for stakeholders, enabling informed decision-making and strategic planning within the rapidly expanding insulated metal panel sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.7 Billion |

| Market Forecast in 2033 | USD 9.5 Billion |

| Growth Rate | 6.8% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Panel Systems, Advanced Building Solutions, Thermal Envelope Specialists, Construction Composites Inc., Insul-Core Innovations, Premier Panel Manufacturers, Eco-Build Systems, Structa Panels, Metl-Span Solutions, VersaPanel, Zenith Building Envelopes, Integrated Panel Products, ColdGuard Panels, GreenSpan Technologies, Future Building Materials, Architectural Panel Group, Superior Thermal Panels, Element Building Solutions, Dynamic Panel Systems, Insulated Structures Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Insulated Metal Panel (IMP) market is meticulously segmented to provide a granular view of its diverse applications and material compositions, offering stakeholders a clear understanding of specific growth drivers and trends within each category. This comprehensive segmentation allows for targeted strategic planning and product development, addressing the unique requirements of various end-use sectors and construction typologies. The market’s structure is defined by key attributes such as the core insulation material, the external facing material, the specific end-use application within a building, and the overall building type, each presenting distinct market dynamics and opportunities.- By Core Material: This segment analyzes the market based on the type of insulating material forming the core of the panel. The choice of core material significantly impacts the panel's thermal performance, fire resistance, and cost-effectiveness, catering to different project specifications and regulatory requirements.

- Polyisocyanurate (PIR): Recognized for its excellent thermal insulation properties and superior fire performance compared to other foam insulants.

- Polyurethane (PUR): Offers good thermal efficiency and structural integrity, widely used in various applications.

- Mineral Wool: Valued for its non-combustible nature, high fire resistance, and acoustic insulation properties, often preferred in fire-sensitive applications.

- Expanded Polystyrene (EPS): A lightweight and cost-effective option providing good thermal insulation, commonly used in less demanding applications.

- Others (e.g., Phenolic Foam): Includes emerging or niche core materials offering specialized properties like enhanced fire resistance or unique thermal characteristics.

- By Facing Material: This segment examines the market by the type of material used for the exterior and interior skins of the IMP, which determine the panel's durability, aesthetics, and resistance to environmental factors.

- Steel (e.g., Galvanized Steel, Stainless Steel): The most common facing material, offering strength, durability, and a wide range of finishes, with galvanized steel providing corrosion resistance and stainless steel offering superior hygiene and aesthetics for specific applications.

- Aluminum: Chosen for its lightweight properties, excellent corrosion resistance, and aesthetic appeal, often used in architectural applications.

- Fiberglass Reinforced Plastic (FRP): Provides high moisture resistance, chemical resistance, and ease of cleaning, making it ideal for hygiene-sensitive environments like food processing plants and cleanrooms.

- Others (e.g., PVC): Includes other specialized facing materials used for specific performance or aesthetic requirements.

- By End-Use Application: This segmentation focuses on where the IMPs are functionally utilized within a construction project, highlighting their versatility across different structural components.

- Walls: The primary application, covering exterior and interior partition walls in various building types.

- Roofs: Used for roofing systems, offering thermal insulation, weather protection, and structural support.

- Ceilings: Applied in suspended or integrated ceiling systems, particularly in cleanrooms and cold storage facilities.

- Cold Storage: A critical application where IMPs provide precise temperature control and energy efficiency for refrigerated warehouses and freezers.

- Cleanrooms: Utilized for sterile environments requiring strict control over temperature, humidity, and airborne particles.

- Architectural Facades: Employed for their aesthetic appeal, design flexibility, and performance in modern building envelopes.

- By Building Type: This segment categorizes the market based on the overall function and design of the structures where IMPs are installed, reflecting the diverse market segments they serve.

- Commercial Buildings (e.g., Offices, Retail, Healthcare): Includes a broad spectrum of commercial structures that benefit from IMPs' energy efficiency, rapid construction, and aesthetic versatility.

- Industrial Buildings (e.g., Manufacturing Plants, Warehouses): A significant segment driven by the need for durable, thermally efficient, and quickly erected structures for various industrial operations.

- Cold Storage Facilities: A highly specialized and growing segment where IMPs are indispensable for maintaining low temperatures and minimizing energy consumption.

- Agricultural Buildings: Used for barns, processing facilities, and storage sheds, providing insulation and durability for agricultural operations.

- Residential Buildings (e.g., Modular Homes): An emerging segment, particularly for modular and prefabricated housing, where IMPs offer speed of construction and high energy performance.

- Institutional Buildings: Includes schools, universities, government buildings, and other public facilities benefiting from IMPs' longevity and energy efficiency.

Regional Highlights

The global Insulated Metal Panel (IMP) market exhibits distinct regional dynamics, influenced by varying construction trends, regulatory frameworks, economic development, and climate conditions. Understanding these regional highlights is crucial for market participants to identify growth opportunities and formulate tailored strategies. Each region presentsa unique landscape shaped by its specific drivers and challenges.- North America: This region is a mature yet consistently growing market for Insulated Metal Panels, driven by stringent energy efficiency codes and a strong emphasis on sustainable building practices. The United States and Canada lead the adoption due to a high demand for high-performance building envelopes in commercial, industrial, and cold storage sectors. The trend towards net-zero energy buildings and the increasing popularity of modular and prefabricated construction techniques further bolster IMP demand. Renovation and retrofitting of aging infrastructure also contribute significantly to market growth. Investment in data centers and cold chain logistics facilities specifically boosts the requirement for IMPs due to their superior thermal properties.

- Europe: Europe represents a leading market for IMPs, propelled by ambitious climate targets, robust green building standards, and a focus on reducing carbon emissions from the built environment. Countries such as Germany, the UK, France, and the Nordic nations are at the forefront of adopting energy-efficient construction materials. The "Renovation Wave" strategy, aimed at improving the energy performance of existing buildings, provides a significant opportunity for IMP manufacturers. Industrial and commercial construction, coupled with specialized applications like food processing and logistics, drives consistent demand. The region's strong regulatory push for fire safety also favors mineral wool core IMPs.

- Asia Pacific (APAC): The Asia Pacific region is the fastest-growing market for Insulated Metal Panels, fueled by rapid urbanization, significant infrastructure development, and a burgeoning construction sector, particularly in countries like China, India, Japan, and Australia. The increasing awareness of energy conservation, coupled with rising disposable incomes and changing lifestyles, is leading to a demand for modern, efficient building solutions. Investments in industrial parks, manufacturing facilities, and cold chain infrastructure to support growing populations and expanding economies are major catalysts. While the market in some parts of APAC is still emerging, the sheer scale of construction activity and a gradual shift towards sustainable practices present immense growth potential.

- Latin America: This region is experiencing steady growth in the IMP market, driven by expanding industrial and commercial sectors, particularly in Brazil, Mexico, and Argentina. Increased foreign investment in manufacturing facilities, growth in the food and beverage industry, and the development of modern retail infrastructure are key factors. While regulatory frameworks for energy efficiency are still evolving, the long-term benefits of IMPs in terms of reduced operational costs and faster construction timelines are increasingly recognized. The demand for modern cold storage facilities to support agricultural exports and food distribution networks is a significant market driver.

- Middle East and Africa (MEA): The MEA region is a dynamic market for Insulated Metal Panels, characterized by ambitious construction projects, diversification efforts away from oil economies, and the need for energy-efficient solutions in extreme climates. Countries like UAE, Saudi Arabia, and Qatar are undertaking large-scale commercial, industrial, and hospitality developments that require advanced building materials. The hot climate necessitates superior thermal insulation to reduce air conditioning loads, making IMPs highly attractive. Investments in logistics hubs, food processing, and data centers further contribute to market growth. However, political stability and fluctuating oil prices can influence the pace of construction activity in certain areas.

Top Key Players:

The market research report covers the analysis of key stake holders of the Insulated Metal Panel Market. Some of the leading players profiled in the report include -- Global Panel Systems

- Advanced Building Solutions

- Thermal Envelope Specialists

- Construction Composites Inc.

- Insul-Core Innovations

- Premier Panel Manufacturers

- Eco-Build Systems

- Structa Panels

- Metl-Span Solutions

- VersaPanel

- Zenith Building Envelopes

- Integrated Panel Products

- ColdGuard Panels

- GreenSpan Technologies

- Future Building Materials

- Architectural Panel Group

- Superior Thermal Panels

- Element Building Solutions

- Dynamic Panel Systems

- Insulated Structures Inc.

Frequently Asked Questions:

What are Insulated Metal Panels (IMPs)?

Insulated Metal Panels (IMPs) are composite building materials comprising two outer metal facings, typically steel or aluminum, bonded to a rigid insulation core. This pre-engineered system provides a single-component solution for walls, roofs, and ceilings that offers superior thermal insulation, weather protection, and structural integrity. IMPs are manufactured in a controlled environment, ensuring consistent quality and enabling rapid, efficient installation on-site. They are highly valued for their energy efficiency, aesthetic versatility, and contribution to accelerated construction timelines across various building types.

What are the primary benefits of using Insulated Metal Panels?

The primary benefits of using Insulated Metal Panels include exceptional thermal performance, which significantly reduces heating and cooling costs over a building's lifespan, contributing to lower operational expenses and a smaller carbon footprint. Their lightweight yet strong construction allows for faster installation compared to traditional multi-component wall or roof systems, leading to reduced labor costs and quicker project completion. IMPs also offer excellent air and vapor barrier properties, minimizing infiltration and exfiltration. Furthermore, they provide durability, aesthetic appeal with various finishes and profiles, and in many cases, enhanced fire resistance and sound attenuation properties, making them a comprehensive and high-value building envelope solution.

In which industries or applications are Insulated Metal Panels most commonly used?

Insulated Metal Panels are most commonly used across a wide range of commercial and industrial applications where thermal performance, speed of construction, and durability are critical. Key industries include cold storage facilities and refrigerated warehouses, food processing plants, manufacturing facilities, and distribution centers, due to their ability to maintain precise temperature control and hygiene standards. They are also extensively utilized in commercial buildings such as offices, retail centers, and healthcare facilities for energy efficiency and modern aesthetics. Furthermore, IMPs are gaining traction in institutional buildings, agricultural structures, data centers, and increasingly in high-performance residential and modular construction projects, reflecting their versatility and efficiency.

What is the market outlook for Insulated Metal Panels?

The market outlook for Insulated Metal Panels is robust and positive, driven by a global emphasis on energy efficiency, sustainable construction, and accelerated building practices. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, expanding from an estimated USD 5.7 billion in 2025 to USD 9.5 billion by 2033. This growth is underpinned by increasing demand from cold storage, industrial, and commercial sectors, coupled with regulatory support for green building initiatives. Opportunities for market expansion exist in retrofitting existing structures and extending applications into new segments like residential and specialized agricultural buildings. While challenges such as raw material price volatility and high initial costs persist, the long-term value proposition of IMPs continues to drive their widespread adoption.

How do Insulated Metal Panels contribute to sustainable building practices?

Insulated Metal Panels contribute significantly to sustainable building practices primarily through their exceptional thermal performance, which drastically reduces a building's energy consumption for heating and cooling, thereby lowering its operational carbon emissions. Their single-component design and prefabrication minimize on-site waste and construction time, further reducing the environmental impact of building processes. Many IMPs utilize recycled content in their metal facings and are fully recyclable at the end of their lifespan, promoting circular economy principles. Furthermore, their durability and longevity contribute to a longer building life cycle, reducing the need for frequent material replacement. By improving building envelope integrity and energy efficiency, IMPs play a vital role in achieving green building certifications and fostering environmentally responsible construction.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted