Industrial Ultrafast Lasers Market

Industrial Ultrafast Lasers Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678240 | Last Updated : July 21, 2025 |

Format : ![]()

![]()

![]()

![]()

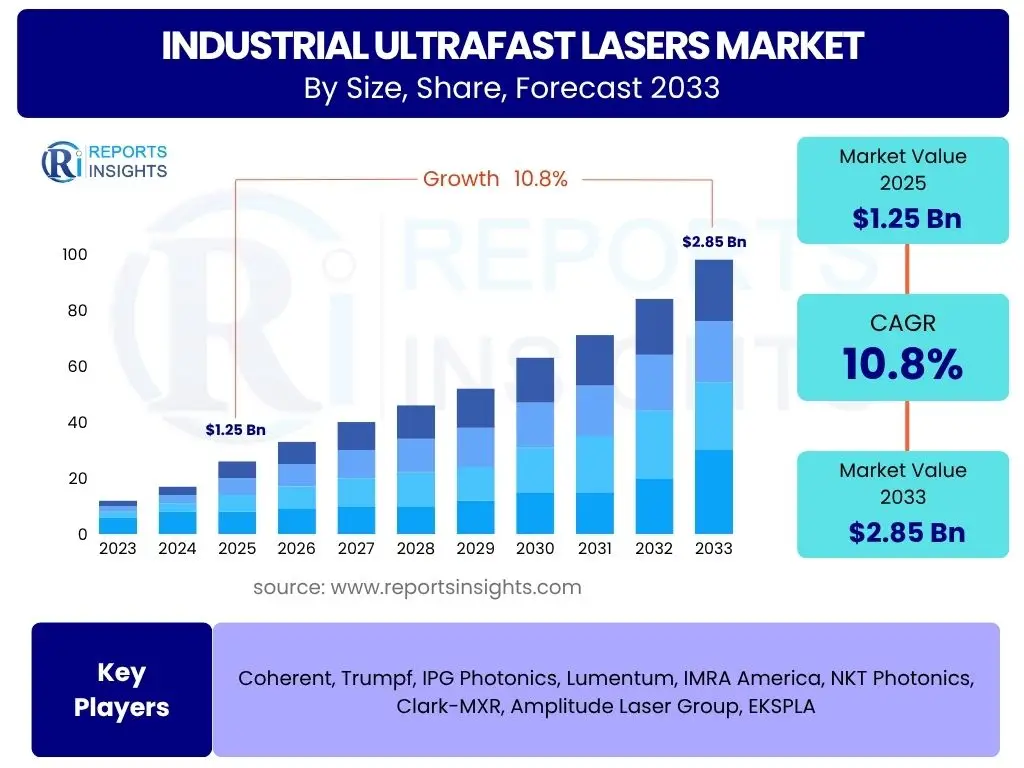

Industrial Ultrafast Lasers Market is projected to grow at a Compound annual growth rate (CAGR) of 10.8% between 2025 and 2033, valued at USD 1.25 Billion in 2025 and is projected to grow by USD 2.85 Billion by 2033 the end of the forecast period.

Key Industrial Ultrafast Lasers Market Trends & Insights

The industrial ultrafast lasers market is experiencing transformative growth driven by continuous technological advancements and expanding application across diverse sectors. Key trends include the ongoing miniaturization of laser systems, making them more accessible and integrable into compact production lines, coupled with a significant drive towards enhanced energy efficiency to reduce operational costs and environmental impact. There is also a notable shift towards greater automation and integration of these lasers into advanced manufacturing processes, such as additive manufacturing and micro-machining, to achieve unparalleled precision and speed. Furthermore, the market is witnessing increased demand for customizable solutions that can be tailored to specific material properties and processing requirements, fostering innovation in beam delivery and pulse shaping technologies. The convergence of ultrafast lasers with digital manufacturing paradigms, including Industry 4.0, is paving the way for smarter, more adaptable production systems globally.

- Miniaturization and compact system designs.

- Enhanced energy efficiency and reduced operational costs.

- Increased automation and integration into advanced manufacturing.

- Growing demand for customized and application-specific solutions.

- Convergence with Industry 4.0 and smart factory concepts.

- Expansion into new materials processing capabilities.

- Rise of hybrid laser processing techniques.

AI Impact Analysis on Industrial Ultrafast Lasers

Artificial Intelligence (AI) is poised to significantly revolutionize the industrial ultrafast lasers market by enhancing operational efficiency, optimizing process parameters, and enabling new application possibilities. AI algorithms can analyze vast datasets from laser processing, enabling real-time adjustments to achieve optimal material removal rates, surface quality, and structural integrity, thereby reducing material waste and improving throughput. Predictive maintenance capabilities powered by AI can forecast equipment failures, minimizing downtime and extending the lifespan of expensive laser systems. Furthermore, AI contributes to the development of autonomous laser processing systems, where machines can learn and adapt to different materials and complex geometries without constant human intervention, significantly improving scalability and reducing reliance on highly specialized operators. This integration also facilitates advanced quality control and defect detection, ensuring consistent high-precision results across production batches, which is critical for demanding industries like medical devices and consumer electronics.

- Optimization of laser processing parameters for precision and speed.

- Predictive maintenance to reduce downtime and extend equipment life.

- Enabling autonomous laser systems for adaptive manufacturing.

- Enhanced quality control and real-time defect detection.

- Accelerated material characterization and process development.

- Development of novel laser-material interactions through data analysis.

Key Takeaways Industrial Ultrafast Lasers Market Size & Forecast

- The Industrial Ultrafast Lasers Market is projected to achieve a robust CAGR of 10.8% from 2025 to 2033.

- Market valuation is set to increase from USD 1.25 Billion in 2025 to USD 2.85 Billion by 2033.

- Growth is primarily fueled by escalating demand for micro-machining and precision material processing across diverse industries.

- The medical device manufacturing and consumer electronics sectors are significant contributors to market expansion.

- Asia Pacific is anticipated to remain the dominant region, driven by extensive manufacturing activities and technological adoption.

- Technological advancements in fiber lasers and diode-pumped solid-state lasers are key enablers of market growth.

- The report provides an in-depth analysis of market dynamics, including drivers, restraints, opportunities, and challenges influencing market trajectory.

Industrial Ultrafast Lasers Market Drivers Impact Analysis

The industrial ultrafast lasers market is significantly propelled by several key drivers that underscore its critical role in modern manufacturing. The escalating global demand for high-precision manufacturing across various industries, including consumer electronics, automotive, and medical devices, is a primary catalyst. Ultrafast lasers offer unparalleled accuracy and minimal heat-affected zones, crucial for processing delicate or heat-sensitive materials without compromising integrity. This precision capability is particularly vital in the fabrication of miniaturized components for smartphones, advanced semiconductors, and intricate medical implants. Additionally, the rapid advancements in additive manufacturing, or 3D printing, are creating new avenues for ultrafast lasers, enabling the precise layering and fusion of materials to create complex geometries with superior surface finish. The ongoing development of electric vehicles (EVs) and advanced battery technologies also contributes substantially, as ultrafast lasers are essential for precise cutting, welding, and surface treatment of components in EV powertrains and battery packs, where conventional methods often fall short in terms of quality and efficiency. Furthermore, increasing automation in industrial processes globally mandates technologies that can be seamlessly integrated into smart factory environments, a role perfectly suited for ultrafast lasers due to their speed, reliability, and digital control capabilities. The continuous innovation in laser technology itself, leading to more robust, energy-efficient, and cost-effective systems, further lowers the barrier to adoption for small and medium-sized enterprises (SMEs) looking to upgrade their manufacturing capabilities.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Precision Manufacturing | +2.5% | Global, especially APAC (China, South Korea, Japan), Europe (Germany), North America (USA) | Long-term, ongoing |

| Growing Adoption in Consumer Electronics | +2.0% | APAC (China, South Korea), North America | Medium-term to Long-term |

| Expansion in Medical Device Manufacturing | +1.8% | North America, Europe, parts of Asia (Japan, Singapore) | Long-term, stable growth |

| Rise of Electric Vehicles (EVs) and Battery Technologies | +1.5% | Global, particularly APAC (China), Europe (Germany), North America (USA) | Medium-term to Long-term |

| Advancements in Additive Manufacturing | +1.2% | Global, particularly advanced manufacturing hubs | Medium-term |

Industrial Ultrafast Lasers Market Restraints Impact Analysis

Despite its significant growth potential, the industrial ultrafast lasers market faces several restraints that could temper its expansion. One of the most prominent challenges is the exceptionally high initial capital investment required for these sophisticated laser systems. Ultrafast lasers, especially those delivering high power and ultra-short pulses, involve complex optical components, precision control systems, and robust cooling mechanisms, all contributing to a substantial upfront cost that can be prohibitive for many small and medium-sized enterprises (SMEs) or businesses with limited capital budgets. This high cost often necessitates a strong return on investment justification, which can be difficult to quantify in diverse applications. Furthermore, the inherent technical complexity of operating and maintaining ultrafast laser systems demands highly skilled personnel. The specialized knowledge required for calibration, troubleshooting, and process optimization creates a talent gap, as there is a limited pool of engineers and technicians proficient in this niche field. This scarcity of skilled labor not only increases operational costs but also presents a barrier to widespread adoption, particularly in regions where advanced technical education is less prevalent. Another restraint involves the competition from established, more traditional laser processing techniques, such as continuous wave (CW) or nanosecond lasers. While ultrafast lasers offer superior precision for specific applications, their higher cost and complexity mean that for less demanding tasks, conventional lasers remain a more economically viable option, thus limiting the penetration of ultrafast lasers into certain segments of the market. Regulatory hurdles and safety concerns related to high-power laser operation also impose additional costs and complexity for businesses, requiring strict adherence to safety protocols and regular inspections, which can slow down adoption rates in some industrial environments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -1.5% | Global, more pronounced in developing economies | Long-term, ongoing |

| Technical Complexity and Skilled Labor Shortage | -1.0% | Global, particularly in regions with nascent industrial laser adoption | Medium-term |

| Competition from Traditional Laser Technologies | -0.8% | Global, especially in less precision-demanding applications | Medium-term |

| Stringent Regulatory and Safety Standards | -0.5% | Europe, North America | Short-term to Medium-term |

Industrial Ultrafast Lasers Market Opportunities Impact Analysis

The industrial ultrafast lasers market is ripe with substantial opportunities that promise to accelerate its growth trajectory. The ongoing trend of miniaturization across various electronic and medical components presents a significant opportunity, as ultrafast lasers are uniquely capable of precise material removal with minimal thermal impact, essential for fabricating tiny, intricate structures. This is particularly relevant in areas like microelectronics, where device features are constantly shrinking, and in biomedical applications, where non-invasive and highly precise surgical tools are in demand. Furthermore, the emergence of new and advanced materials, such as composites, ceramics, and specialized alloys, which are difficult to process with traditional methods, opens up new application frontiers for ultrafast lasers. Their ability to ablate virtually any material with high precision positions them as a key technology for future material processing challenges. The increasing focus on sustainability and eco-friendly manufacturing processes also creates an opportunity, as ultrafast lasers offer cleaner processing with less material waste and often lower energy consumption compared to conventional methods, aligning with global environmental regulations and corporate responsibility initiatives. Moreover, the significant potential for integration into fully automated and intelligent manufacturing lines, driven by Industry 4.0 paradigms, allows for more efficient, flexible, and responsive production systems. This enables industries to adopt customized mass production and rapid prototyping, catering to evolving consumer demands and accelerating product development cycles. Research and development initiatives, particularly in fields such as advanced optics, beam shaping, and fiber laser technology, continue to push the boundaries of ultrafast laser capabilities, leading to more powerful, versatile, and accessible systems, thereby creating new market niches and expanding existing ones.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization in Electronics and Medical Devices | +2.2% | Global, especially APAC (electronics), North America & Europe (medical) | Long-term, ongoing |

| Processing of New and Advanced Materials | +1.9% | Global, particularly in aerospace, automotive, and defense industries | Medium-term to Long-term |

| Integration with Industry 4.0 and Smart Manufacturing | +1.7% | Developed economies (Germany, USA, Japan), emerging manufacturing hubs | Medium-term |

| Development of More Robust and Cost-Effective Fiber Lasers | +1.5% | Global | Short-term to Medium-term |

| Expansion into Renewable Energy Component Manufacturing | +1.0% | Europe, Asia (China), North America | Long-term |

Industrial Ultrafast Lasers Market Challenges Impact Analysis

The industrial ultrafast lasers market, despite its promising outlook, faces several significant challenges that require strategic navigation. One primary challenge lies in the complex process optimization required for different materials and applications. Achieving the optimal balance of laser parameters—such as pulse energy, repetition rate, and spot size—to yield desired material modifications (e.g., cutting, ablation, structuring) while maintaining efficiency and preventing collateral damage can be highly intricate and time-consuming. This often necessitates extensive empirical testing and specialized expertise, adding to development costs and project timelines. Another hurdle is the integration of ultrafast laser systems into existing industrial workflows and production lines. Many manufacturers operate with legacy equipment, and the transition to high-precision ultrafast laser technology requires substantial redesign of processes, investment in compatible machinery, and retraining of the workforce. This can lead to resistance to adoption due to perceived disruption and the significant upfront effort involved in integration. Furthermore, the vulnerability of the global supply chain, particularly for highly specialized optical components and advanced electronics used in ultrafast laser manufacturing, poses a risk. Geopolitical tensions, trade disputes, and unforeseen global events can disrupt the supply of critical parts, leading to production delays and increased costs for laser manufacturers, ultimately impacting market availability and pricing for end-users. The highly competitive landscape, with continuous innovation from established players and emerging startups, means companies must constantly invest in research and development to maintain a technological edge. This intense competition can lead to pricing pressures and a shorter product lifecycle, demanding rapid adaptation and significant R&D expenditures to remain relevant in the market. Ensuring consistent quality and reliability of ultrafast laser systems, especially in demanding 24/7 industrial environments, also presents an ongoing engineering challenge, requiring robust designs and comprehensive testing protocols.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Process Optimization for Diverse Materials | -1.2% | Global, particularly for new and niche applications | Long-term, ongoing |

| Integration into Existing Manufacturing Infrastructures | -1.0% | Global, more challenging in industries with legacy systems | Medium-term |

| Supply Chain Vulnerabilities for Key Components | -0.7% | Global, impacting manufacturers and end-users alike | Short-term to Medium-term (event-driven) |

| High R&D Investment and Rapid Technological Obsolescence | -0.5% | Global, primarily affecting laser manufacturers | Long-term, ongoing |

Industrial Ultrafast Lasers Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Industrial Ultrafast Lasers Market, covering market size, growth forecasts, key drivers, restraints, opportunities, and challenges. It segments the market by type, application, end-use industry, and region, offering a holistic view of the market landscape and its projected evolution. The report includes profiles of leading companies, detailing their strategies, product portfolios, and market positions, enabling stakeholders to make informed decisions and identify lucrative growth avenues within this dynamic sector.

| Report Attributes | Report Details |

|---|---|

| Report Name | Industrial Ultrafast Lasers Market |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.85 Billion |

| Growth Rate | CAGR of 2025 to 2033 10.8% |

| Number of Pages | 280 |

| Key Companies Covered | Coherent, Trumpf, IPG Photonics, Lumentum, IMRA America, NKT Photonics, Clark-MXR, Amplitude Laser Group, EKSPLA |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

Market Product Type Segmentation:-- Titanium-sapphire Lasers

- Diode-pumped Lasers

- Fiber Lasers

- Mode-locked Diode Lasers

- Others

- Material Processing

- Others

Regional Highlights

- Asia Pacific (APAC): This region is expected to dominate the industrial ultrafast lasers market, primarily driven by its robust manufacturing base, particularly in countries like China, South Korea, Japan, and Taiwan. These nations are global leaders in consumer electronics, semiconductor manufacturing, and electric vehicle production, all of which are major end-users of ultrafast lasers for precision processing. Rapid industrialization, government support for advanced manufacturing technologies, and increasing R&D investments further propel the market in this region.

- North America: A significant market for industrial ultrafast lasers, characterized by early adoption of advanced manufacturing techniques and a strong presence of aerospace, medical device, and defense industries. The United States leads innovation in laser technology and applications, with substantial investment in R&D and a demand for high-value, high-precision components. Canada and Mexico also contribute to the regional growth through their manufacturing sectors.

- Europe: This region holds a substantial share of the market, with countries like Germany, France, and Switzerland being at the forefront of industrial automation, automotive manufacturing, and high-precision engineering. Europe's emphasis on Industry 4.0 initiatives and sustainable manufacturing practices drives the adoption of advanced laser technologies. Strong research capabilities and collaborations between academia and industry also foster innovation and market expansion.

- Latin America: Expected to witness steady growth, albeit from a smaller base, driven by increasing foreign investments in manufacturing and the modernization of industrial infrastructure, particularly in countries like Brazil and Mexico. The automotive and electronics sectors are key areas where ultrafast lasers are gaining traction.

- Middle East and Africa (MEA): This region is projected for gradual growth, influenced by diversification efforts from oil-dependent economies into manufacturing and technology sectors. Investments in smart city projects and developing industrial capabilities are creating nascent opportunities for advanced laser systems, though adoption rates may be slower due to economic and technological readiness levels.

Top Key Players:

The market research report covers the analysis of key stakeholders of the Industrial Ultrafast Lasers Market. Some of the leading players profiled in the report include -:- Coherent

- Trumpf

- IPG Photonics

- Lumentum

- IMRA America

- NKT Photonics

- Clark-MXR

- Amplitude Laser Group

- EKSPLA

Frequently Asked Questions:

What are industrial ultrafast lasers?

Industrial ultrafast lasers are advanced laser systems that emit extremely short pulses of light, typically in the picosecond (trillionths of a second) or femtosecond (quadrillionths of a second) range. These ultra-short pulses enable highly precise material processing with minimal heat impact, making them ideal for delicate or heat-sensitive applications in various industrial sectors.

What are the primary applications of industrial ultrafast lasers?

The primary applications of industrial ultrafast lasers include precision micro-machining, cutting, drilling, and surface modification of various materials. They are extensively used in consumer electronics for manufacturing components like smartphone displays and micro-LEDs, in medical device manufacturing for surgical instruments and implants, and in the automotive sector for EV battery production and lightweighting initiatives.

How do ultrafast lasers differ from traditional industrial lasers?

Ultrafast lasers differ from traditional industrial lasers (like continuous wave or nanosecond lasers) primarily in their pulse duration. Their ultra-short pulses deliver energy to materials so rapidly that there is no time for heat to diffuse into the surrounding area. This "cold ablation" process results in extremely clean cuts, minimal or no heat-affected zones, and reduced material stress, leading to superior quality and precision compared to traditional methods.

What factors are driving the growth of the Industrial Ultrafast Lasers Market?

The key drivers for market growth include the increasing demand for high-precision manufacturing across industries, the rapid expansion of consumer electronics and medical device sectors, the growing adoption of ultrafast lasers in electric vehicle (EV) battery production, and advancements in additive manufacturing. Miniaturization trends and the ability to process new, challenging materials also significantly contribute to market expansion.

What are the future trends in the industrial ultrafast lasers market?

Future trends in the industrial ultrafast lasers market include increased integration with Artificial Intelligence (AI) for process optimization and predictive maintenance, continued miniaturization of laser systems for compact industrial integration, development of more energy-efficient and robust fiber-based ultrafast lasers, and wider adoption in Industry 4.0 enabled smart factories. Expansion into new material processing frontiers and customized application solutions are also significant trends.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted