Industrial Traction Equipment Market

Industrial Traction Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702493 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

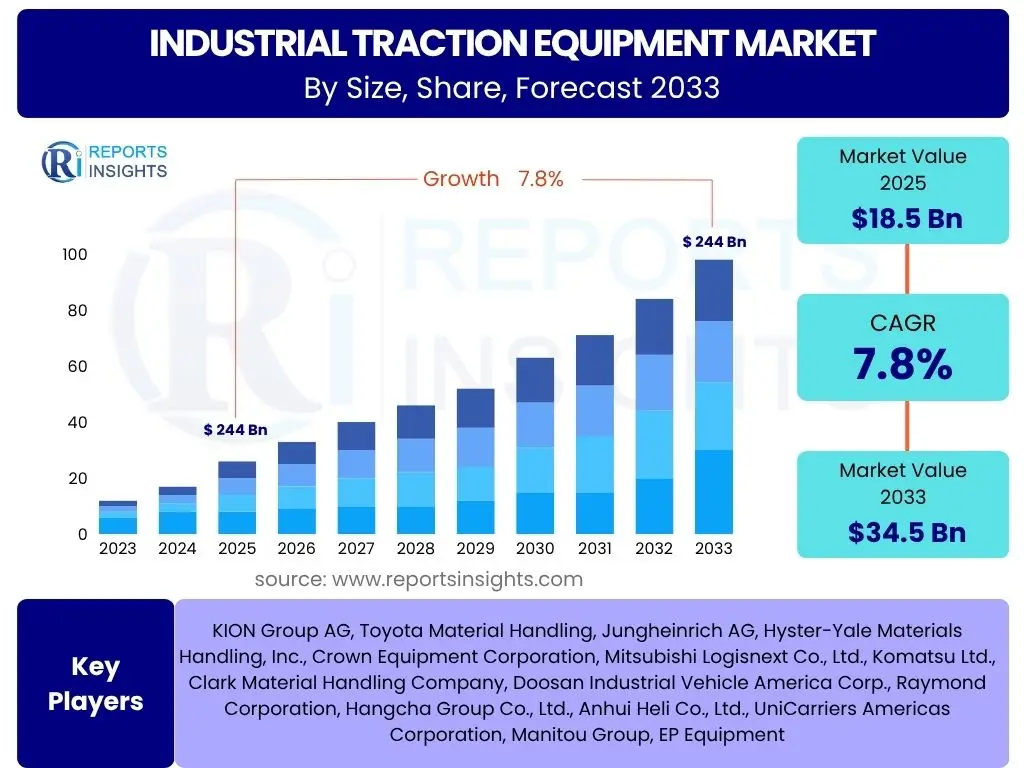

Industrial Traction Equipment Market Size

According to Reports Insights Consulting Pvt Ltd, The Industrial Traction Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 34.5 Billion by the end of the forecast period in 2033.

Key Industrial Traction Equipment Market Trends & Insights

The industrial traction equipment market is undergoing significant transformation, primarily driven by the imperative for enhanced operational efficiency, the widespread adoption of automation technologies, and a global shift towards sustainable industrial practices. End-users are increasingly seeking solutions that not only streamline material handling and logistics but also contribute to reduced operational costs, improved safety standards, and a smaller environmental footprint. The demand for robust, reliable, and intelligent equipment that can seamlessly integrate into complex operational ecosystems is a defining characteristic of current market dynamics. Furthermore, the expansion of e-commerce necessitates agile and high-capacity warehousing solutions, directly influencing the demand for advanced traction equipment.

Technological advancements are playing a pivotal role in shaping these trends, with innovations in power sources and connectivity leading the way. The push towards electrification, primarily through advanced battery technologies and the nascent adoption of hydrogen fuel cells, is reshaping fleet compositions. Simultaneously, the integration of smart technologies, such as the Internet of Things (IoT) and artificial intelligence (AI), is transforming equipment from standalone machines into interconnected data-generating assets, enabling predictive maintenance, optimized resource allocation, and real-time operational insights. This convergence of efficiency, sustainability, and technological sophistication defines the core trends within this evolving market.

- Growing adoption of electric and hydrogen fuel cell traction equipment, driven by environmental regulations and operational cost benefits.

- Increasing demand for autonomous guided vehicles (AGVs) and autonomous mobile robots (AMRs) to enhance automation in warehousing and logistics.

- Emphasis on energy efficiency and reduced carbon footprint in industrial operations, promoting the uptake of eco-friendly equipment.

- Integration of IoT, AI, and Big Data analytics for predictive maintenance, fleet optimization, and real-time performance monitoring.

- Shift towards customized and modular equipment solutions to meet specific industry and application requirements.

- Rising popularity of equipment as a service (EaaS) and rental models to reduce capital expenditure for businesses.

AI Impact Analysis on Industrial Traction Equipment

Artificial intelligence is poised to revolutionize the industrial traction equipment sector by enabling more intelligent, efficient, and autonomous operations. Common user questions related to AI's impact often revolve around how it enhances equipment capabilities, improves safety, and contributes to overall operational savings. AI-powered systems facilitate advanced predictive maintenance, utilizing machine learning algorithms to analyze real-time data from sensors on equipment. This capability allows operators to anticipate potential failures, schedule maintenance proactively, and significantly reduce unscheduled downtime, thereby extending the lifespan of machinery and ensuring continuous productivity. The precision and foresight offered by AI-driven diagnostics fundamentally transform equipment management from reactive to predictive.

Furthermore, AI is crucial in advancing the capabilities of autonomous vehicles, such as AGVs and AMRs, which are becoming integral to modern logistics and manufacturing. AI algorithms enable more sophisticated navigation, dynamic path planning, obstacle detection, and real-time decision-making in complex and dynamic industrial environments. This leads to safer operations, optimized material flow, and a reduction in human error. The integration of AI also extends to optimizing energy consumption in electric traction equipment by learning usage patterns and managing battery charging cycles efficiently. Consequently, AI not only enhances the autonomy and safety of industrial traction equipment but also drives substantial improvements in operational efficiency and resource utilization, making it a critical enabler for the future of industrial automation.

- Enhanced predictive maintenance capabilities, minimizing unscheduled downtime through data analysis and machine learning.

- Improved navigation, obstacle avoidance, and dynamic path optimization for autonomous guided vehicles (AGVs) and autonomous mobile robots (AMRs).

- Real-time operational data analysis for optimized energy consumption and extended battery life in electric equipment.

- AI-driven safety features, including advanced collision avoidance systems and operator assistance functionalities.

- Optimized fleet management and resource allocation through machine learning algorithms, leading to higher utilization rates.

- Automated quality control and inventory management within smart warehousing systems integrated with traction equipment.

Key Takeaways Industrial Traction Equipment Market Size & Forecast

The industrial traction equipment market is poised for robust and sustained growth through the forecast period, reflecting a significant transformation in global industrial and logistics operations. Common user questions about key takeaways often focus on the market's overall trajectory, the primary drivers of this expansion, and the most impactful technological shifts. The substantial projected Compound Annual Growth Rate (CAGR) from 2025 to 2033 underscores a dynamic market characterized by increasing investment in automation, a global pivot towards sustainable solutions, and the integration of advanced digital technologies. This growth is not merely incremental but represents a fundamental shift in how industries manage and move goods.

A critical takeaway is the accelerating demand for electric and autonomous equipment, driven by rising labor costs, environmental mandates, and the need for higher operational efficiency in e-commerce and manufacturing sectors. Stakeholders must recognize that innovation, particularly in AI, IoT, and battery technology, will be paramount for securing a competitive edge. The market is moving towards more intelligent, interconnected, and eco-friendly solutions, necessitating strategic investments in research and development, as well as the adaptation of business models to cater to evolving customer preferences for efficiency and sustainability. Understanding these core elements is crucial for capitalizing on the market's expansive potential.

- Significant market expansion expected through 2033, driven by a confluence of technological and operational imperatives.

- Electrification and automation are identified as the primary growth engines, profoundly reshaping equipment design and deployment.

- Strong and continuous demand from key end-use industries, including warehousing, logistics, and manufacturing sectors.

- Technological innovation, particularly in AI and IoT integration, is critical for market leadership and differentiation.

- Sustainability mandates and growing environmental consciousness are accelerating the adoption of eco-friendly traction equipment.

- The market is shifting towards solutions that offer enhanced productivity, reduced operational costs, and improved safety.

Industrial Traction Equipment Market Drivers Analysis

The industrial traction equipment market is primarily propelled by the exponential growth of the e-commerce sector, which necessitates highly efficient and automated warehousing and logistics operations globally. The surge in online retail demand has dramatically increased the volume and speed of goods movement, creating an urgent need for advanced material handling solutions that can manage vast inventories and expedite order fulfillment processes. This fundamental shift in consumer behavior directly drives investment in modern forklifts, pallet trucks, automated guided vehicles (AGVs), and autonomous mobile robots (AMRs) to keep pace with operational demands. Rapid industrialization and urbanization in emerging economies further escalate the demand for sophisticated material handling infrastructure, as these regions expand their manufacturing bases and logistical networks.

Additionally, stringent regulations promoting worker safety and environmental sustainability are driving the adoption of modern, ergonomic, and energy-efficient equipment. Governments and industries worldwide are imposing stricter emission standards and encouraging the transition to cleaner energy sources, making electric and hydrogen fuel cell traction equipment increasingly appealing. The increasing labor costs and scarcity of skilled labor in developed economies are also compelling businesses to invest heavily in automated traction equipment to maintain productivity levels and reduce reliance on manual operations. This confluence of factors, including regulatory pressures, labor market dynamics, and the expansion of the digital economy, provides a strong foundational impetus for market expansion. Furthermore, the global push towards Industry 4.0 and smart manufacturing initiatives underscores the importance of interconnected and intelligent industrial machinery, encouraging the integration of IoT, AI, and data analytics into traction equipment for enhanced capabilities.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| E-commerce & Logistics Sector Expansion | +1.5% | Global | Short to Medium Term (2025-2030) |

| Increasing Adoption of Automation & Industry 4.0 | +1.2% | North America, Europe, APAC | Medium to Long Term (2026-2033) |

| Electrification & Sustainability Mandates | +1.0% | Europe, North America, Global | Medium to Long Term (2027-2033) |

| Rising Labor Costs & Shortage Pressures | +0.8% | Developed Economies | Short to Medium Term (2025-2030) |

| Advancements in Battery Technology | +0.7% | Global | Medium Term (2026-2031) |

Industrial Traction Equipment Market Restraints Analysis

Despite significant growth potential, the industrial traction equipment market faces several notable restraints, most significantly the high initial capital investment required for acquiring advanced machinery, particularly automated and electric models. This substantial upfront cost can be a considerable barrier for small and medium-sized enterprises (SMEs) with limited financial resources, hindering their ability to upgrade to modern, more efficient equipment. Additionally, the complexity associated with integrating new, sophisticated equipment into existing operational infrastructures can deter adoption, often requiring significant training for personnel, extensive system overhauls, and potential disruptions to current workflows. Concerns over the total cost of ownership (TCO), which includes not only the purchase price but also maintenance, spare parts, and energy consumption, also temper market expansion as businesses meticulously evaluate long-term financial commitments.

Furthermore, supply chain vulnerabilities, exacerbated by geopolitical instabilities and trade disputes, alongside the fluctuating costs of critical raw materials such as lithium, steel, and semiconductors, pose significant challenges to manufacturers. These factors can lead to increased production costs, longer lead times, and reduced profit margins, ultimately impacting equipment availability and affordability. The availability of adequate charging infrastructure for electric equipment, particularly in older industrial facilities or developing regions, remains a practical constraint that limits widespread adoption. Moreover, the lack of skilled personnel capable of operating, maintaining, and repairing complex modern traction equipment can hinder operational efficiency and increase reliance on expensive external support, thereby contributing to overall operational costs and slowing market momentum. Addressing these multifaceted restraints is crucial for unlocking the market's full potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -0.7% | Developing Regions, SMEs Globally | Short to Medium Term (2025-2029) |

| Supply Chain Disruptions & Volatile Material Costs | -0.5% | Global | Short Term (2025-2027) |

| Lack of Skilled Labor for Advanced Equipment | -0.4% | Developed Economies | Medium to Long Term (2027-2033) |

| Infrastructure Limitations for Electrification | -0.3% | Specific Regions (e.g., Older Industrial Zones) | Medium Term (2026-2031) |

| Integration Complexities with Existing Systems | -0.2% | Global | Short to Medium Term (2025-2028) |

Industrial Traction Equipment Market Opportunities Analysis

The industrial traction equipment market presents numerous opportunities driven by continuous technological innovation and evolving global market demands. A significant opportunity lies in the expansion into new application areas and industries beyond traditional warehousing and logistics, such as specialized manufacturing processes, agricultural applications, port operations, and recycling facilities. These sectors are increasingly recognizing the efficiency and safety benefits of modern traction equipment, opening up untapped revenue streams for manufacturers and service providers. The ongoing development of advanced battery technologies, including higher-density lithium-ion chemistries and the nascent potential of solid-state batteries, along with improvements in hydrogen fuel cell technology, promises to enhance performance, reduce charging times, and extend operational ranges. These advancements make electric and alternative-fuel equipment even more appealing and expand their potential deployment across a broader spectrum of demanding applications, addressing both environmental concerns and operational efficacy.

Furthermore, the growing demand for customization and modularity in equipment design represents a key opportunity. Manufacturers can offer tailored solutions that precisely fit specific operational requirements and integrate new functionalities more easily, enhancing customer satisfaction and market differentiation. The burgeoning demand for rental and leasing models for industrial equipment provides significant flexibility for businesses, lowers upfront capital outlays, and allows for easier adoption of the latest technologies without large capital expenditures. This shift appeals particularly to SMEs and companies managing fluctuating operational needs. Additionally, the increasing focus on data-driven services, such as predictive maintenance subscriptions, fleet optimization software, and equipment-as-a-service (EaaS) models, opens up new service-based revenue streams. These opportunities are vital for future market leadership, enabling companies to transition from pure equipment sales to comprehensive solution providers, fostering long-term customer relationships and sustainable growth in a competitive landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Battery & Fuel Cell Technologies | +1.0% | Global | Medium to Long Term (2028-2033) |

| Expansion into New Application & End-Use Industries | +0.9% | APAC, Latin America, Middle East & Africa | Medium Term (2026-2031) |

| Growth of Equipment Leasing & Rental Models | +0.7% | North America, Europe, Global | Short to Medium Term (2025-2029) |

| Integration with IoT, AI & Data Analytics for Value-Added Services | +0.6% | Global | Medium to Long Term (2027-2033) |

| Increased Focus on Customization & Modularity | +0.5% | Global | Short to Medium Term (2025-2030) |

Industrial Traction Equipment Market Challenges Impact Analysis

The industrial traction equipment market faces significant challenges, notably intense competition from both established global players and emerging technology firms, which often leads to price pressures and the continuous demand for innovation. This competitive landscape necessitates substantial investment in research and development to differentiate products and maintain market relevance. Rapid technological advancements, while offering opportunities, also create a challenge of keeping pace with the latest innovations, ensuring backward compatibility with legacy systems, and managing the potential for technological obsolescence of existing fleets. Manufacturers must constantly adapt their product portfolios and engineering capabilities to integrate new features like advanced automation, AI, and sustainable power sources, requiring significant resource allocation and strategic foresight.

Furthermore, the complexity of global supply chains, exacerbated by geopolitical instability, trade tensions, and unforeseen events such as pandemics, introduces unpredictability in component availability and costs of raw materials. This can lead to production delays, increased manufacturing expenses, and difficulties in meeting delivery schedules. Meeting diverse regional regulatory standards for emissions, safety, and energy efficiency adds layers of complexity for manufacturers operating internationally, requiring tailored product designs and certifications for different markets. Cybersecurity risks associated with increasingly connected and autonomous equipment also pose a growing challenge, requiring robust security measures to protect critical operational data, prevent unauthorized access, and mitigate the potential for malicious interference or system vulnerabilities. Effectively addressing these multifaceted challenges will be crucial for sustained growth, maintaining profitability, and securing a leading market position within this dynamic industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition & Price Pressure | -0.6% | Global | Short to Medium Term (2025-2030) |

| Raw Material Price Volatility & Geopolitical Risks | -0.5% | Global | Short Term (2025-2027) |

| Rapid Technological Obsolescence | -0.4% | Global | Medium to Long Term (2027-2033) |

| Cybersecurity Threats to Connected Equipment | -0.3% | Global | Medium to Long Term (2028-2033) |

| Adherence to Diverse Regional Regulations | -0.2% | Europe, North America, Asia Pacific | Ongoing |

Industrial Traction Equipment Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Industrial Traction Equipment Market, covering market size estimations, historical data, and forward-looking projections up to 2033. It examines critical market trends, drivers, restraints, opportunities, and challenges that are shaping the industry landscape. The scope also includes a detailed segmentation analysis, regional insights, and profiles of key market players, offering a holistic view of the market's current state and future potential. This structured assessment aims to equip stakeholders with actionable intelligence for strategic decision-making and understanding market dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 34.5 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | KION Group AG, Toyota Material Handling, Jungheinrich AG, Hyster-Yale Materials Handling, Inc., Crown Equipment Corporation, Mitsubishi Logisnext Co., Ltd., Komatsu Ltd., Clark Material Handling Company, Doosan Industrial Vehicle America Corp., Raymond Corporation, Hangcha Group Co., Ltd., Anhui Heli Co., Ltd., UniCarriers Americas Corporation, Manitou Group, EP Equipment |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial traction equipment market is extensively segmented based on various attributes to cater to diverse industrial requirements and operational scales, providing a granular understanding of market dynamics. These classifications enable a detailed analysis of demand patterns, technological preferences, and regional adoption rates, thereby facilitating the development of targeted market strategies. Key segmentation areas include the specific product type of equipment, its primary power source, carrying capacity, the specific application it serves within an industry, and the overarching end-use industry. This multi-faceted segmentation reflects the market's inherent complexity and its responsiveness to specialized needs across the global economy.

The product type segmentation differentiates between foundational material handling equipment like forklifts, pallet trucks, and stackers, and cutting-edge categories such as AGVs and AMRs, which represent the forefront of automation. The power source classification highlights the significant ongoing transition from conventional internal combustion engines to more sustainable electric and hydrogen fuel cell alternatives, a shift driven by environmental mandates and operational efficiency gains. Furthermore, the segmentation by application and end-use industry reveals how specific sectors, including e-commerce, automotive, and manufacturing, are driving the adoption of particular equipment types tailored to their unique logistical and production challenges. This comprehensive segmentation is crucial for understanding the nuanced needs of different market verticals and for identifying specific growth opportunities within each category.

- By Product Type: Includes Forklifts, Pallet Trucks, Stackers, Order Pickers, Tow Tractors, Reach Trucks, Automated Guided Vehicles (AGVs), Autonomous Mobile Robots (AMRs), and Other specialized equipment.

- By Power Source: Comprises Electric (Battery-powered, Fuel Cell), Internal Combustion Engine (ICE), and Hybrid options, reflecting diverse energy preferences.

- By Capacity: Categorized into Less than 5 Tons, 5-10 Tons, and More than 10 Tons, addressing a wide range of load requirements and operational scales.

- By Application: Encompasses Material Handling, Warehousing, Logistics, Manufacturing, Construction, Retail, and Other specific industrial uses.

- By End-Use Industry: Covers Automotive, Food & Beverage, Retail & E-commerce, Manufacturing, Logistics & Transportation, Pulp & Paper, Chemicals, Pharmaceuticals, and various Others, indicating sector-specific demands.

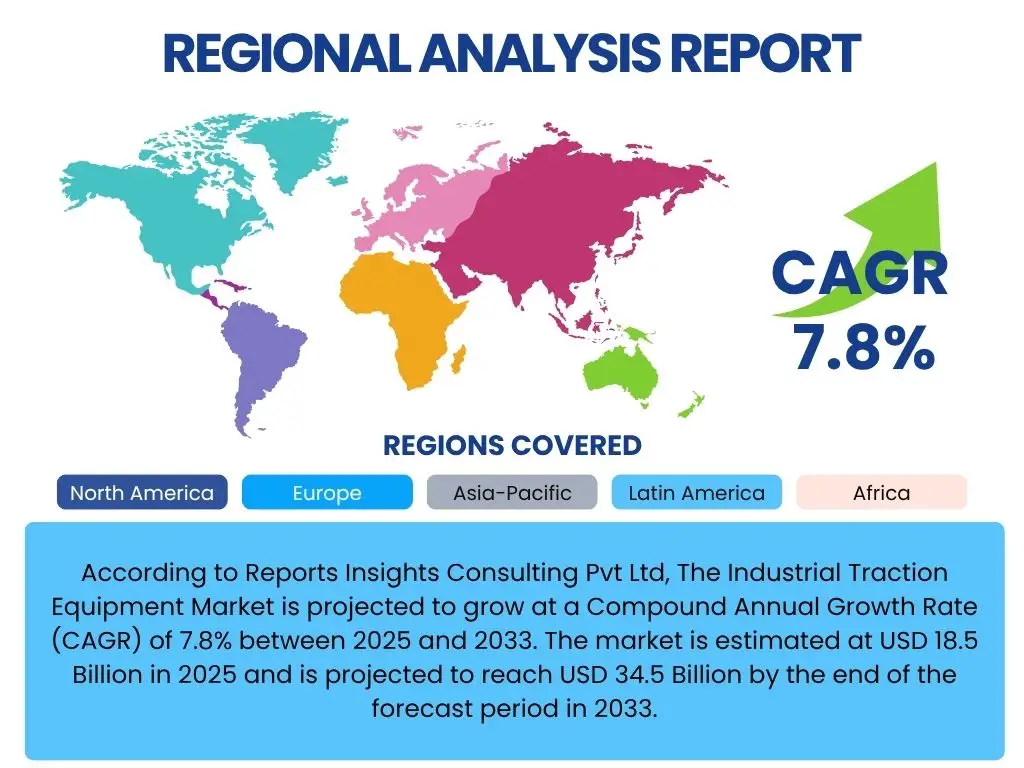

Regional Highlights

The industrial traction equipment market exhibits significant regional variations in terms of adoption rates, technological preferences, and growth trajectories, influenced by economic development, industrialization levels, and regulatory environments. North America and Europe stand as mature markets, characterized by high adoption rates of automation, stringent environmental regulations, and a strong emphasis on electric and autonomous solutions. These regions are early adopters of advanced technologies such as AI-integrated equipment and sophisticated fleet management systems, primarily driven by high labor costs and the imperative for efficiency gains in their established industrial sectors. Continuous investment in modernizing existing infrastructure and a robust demand for sustainable operational practices further underpin market expansion in these developed economies, with a focus on high-value, high-performance solutions.

In contrast, the Asia Pacific (APAC) region is projected to demonstrate the highest Compound Annual Growth Rate (CAGR) during the forecast period. This accelerated growth is fueled by rapid industrialization, the burgeoning e-commerce industries, and significant government and private sector investments in manufacturing and logistics infrastructure, particularly evident in economic powerhouses like China, India, Japan, and Southeast Asian countries. The increasing demand for efficient warehousing solutions to manage vast consumer bases and the rising adoption of automation to enhance productivity are key drivers across APAC. Latin America and the Middle East & Africa (MEA) regions are also showing nascent but steady growth, driven by ongoing infrastructure development projects, economic diversification efforts, and increasing foreign direct investment in manufacturing and logistics sectors. While these regions represent emerging opportunities for market expansion, they exhibit varying levels of technological readiness and regulatory frameworks, requiring tailored market approaches. Each region's unique economic and industrial landscape dictates the specific types of traction equipment in highest demand, from basic forklifts to advanced AGVs.

- North America: A mature market with high adoption of automation, electric, and AI-integrated solutions, propelled by elevated labor costs and the strong imperative for operational efficiency and safety.

- Europe: Characterized by a robust focus on sustainability, advanced material handling solutions, and comprehensive regulatory support for the widespread adoption of electrification in industrial settings.

- Asia Pacific (APAC): The fastest-growing region, driven by rapid industrialization, the booming e-commerce sector, and extensive infrastructure development, particularly in key countries like China, India, and Southeast Asia.

- Latin America: An emerging market experiencing growing demand influenced by industrial expansion, increasing trade activities, and ongoing infrastructure development projects.

- Middle East & Africa (MEA): Demonstrating gradual market development primarily influenced by economic diversification efforts, increasing investment in logistics hubs, and growing industrialization.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Traction Equipment Market.- KION Group AG

- Toyota Material Handling

- Jungheinrich AG

- Hyster-Yale Materials Handling, Inc.

- Crown Equipment Corporation

- Mitsubishi Logisnext Co., Ltd.

- Komatsu Ltd.

- Clark Material Handling Company

- Doosan Industrial Vehicle America Corp.

- Raymond Corporation

- Hangcha Group Co., Ltd.

- Anhui Heli Co., Ltd.

- UniCarriers Americas Corporation

- Manitou Group

- EP Equipment

- Liebherr Group

- Caterpillar Inc.

- Volvo Construction Equipment

- JLG Industries, Inc.

- Terex Corporation

Frequently Asked Questions

Analyze common user questions about the Industrial Traction Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What factors are driving the growth of the industrial traction equipment market?

The market's growth is primarily driven by the expansion of the e-commerce sector, the increasing demand for automation in logistics and manufacturing operations, rising labor costs, and the global shift towards sustainable and energy-efficient material handling solutions.

How is artificial intelligence (AI) impacting industrial traction equipment?

AI integration significantly enhances predictive maintenance capabilities, optimizes navigation for autonomous vehicles (AGVs/AMRs), improves fleet management efficiency, and enables real-time data analysis for operational insights and improved safety in industrial traction equipment.

What are the main challenges faced by the industrial traction equipment market?

Key challenges include high initial capital investment costs for advanced equipment, disruptions within the global supply chain, intense market competition leading to price pressures, the persistent need for skilled labor, and the rapid pace of technological obsolescence.

Which regions are showing the most significant growth in the industrial traction equipment market?

The Asia Pacific (APAC) region is projected to exhibit the highest growth rate, fueled by rapid industrialization and a booming e-commerce sector, while North America and Europe continue to be key mature markets for advanced equipment adoption.

What are the key segments within the industrial traction equipment market?

The market is comprehensively segmented by product type (e.g., forklifts, AGVs), power source (e.g., electric, internal combustion engine), capacity, specific application (e.g., warehousing, manufacturing), and the particular end-use industry (e.g., automotive, retail).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted