Industrial Oxygen Market

Industrial Oxygen Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704550 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

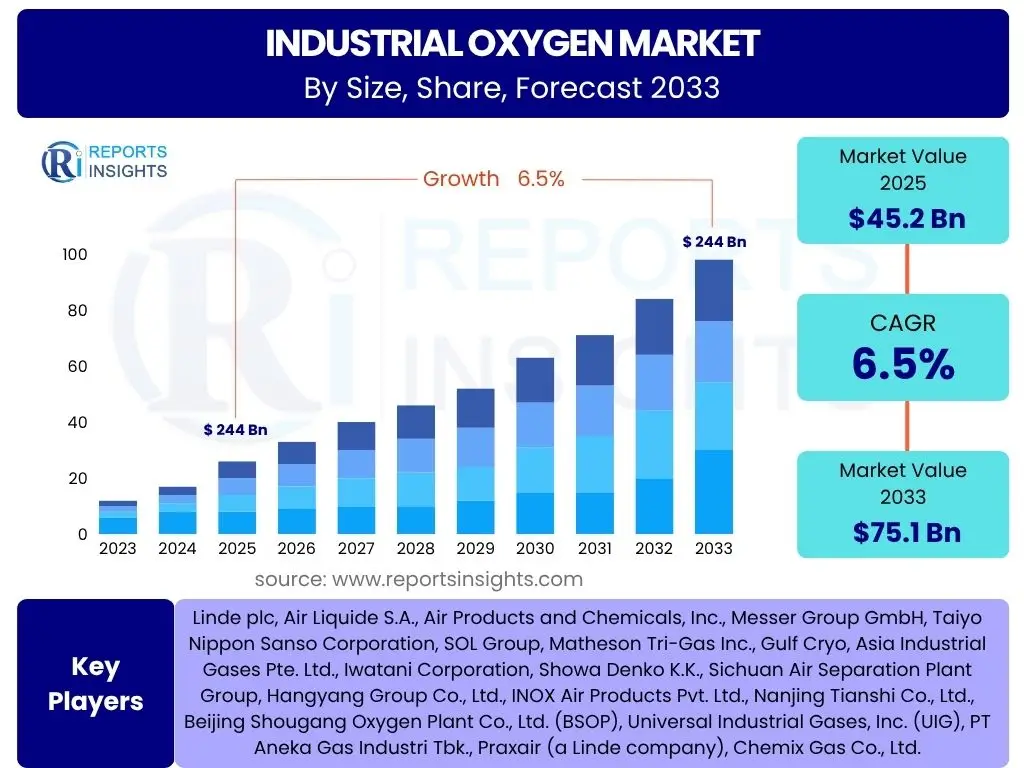

Industrial Oxygen Market Size

According to Reports Insights Consulting Pvt Ltd, The Industrial Oxygen Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 45.2 billion in 2025 and is projected to reach USD 75.1 billion by the end of the forecast period in 2033.

Key Industrial Oxygen Market Trends & Insights

The industrial oxygen market is currently witnessing a confluence of trends driven by global industrial expansion, particularly in emerging economies, and the increasing demand from critical sectors such as healthcare, metal fabrication, and chemical processing. A significant trend is the growing emphasis on efficiency and sustainability in oxygen production and consumption, leading to the adoption of advanced on-site generation technologies and improved supply chain logistics. Users are increasingly seeking information on how these trends will shape future market dynamics, especially concerning cost-effectiveness and environmental impact.

Another prominent insight revolves around the diversification of industrial oxygen applications. Beyond traditional uses in steelmaking and welding, there is a notable uptake in non-conventional areas like wastewater treatment, advanced electronics manufacturing, and clean energy initiatives, including hydrogen production and carbon capture technologies. This expansion indicates a broadening market base and new avenues for growth, requiring suppliers to adapt their product offerings and delivery models. The focus is shifting towards integrated solutions that not only provide oxygen but also optimize its utilization for specific industrial processes.

- Accelerated industrialization in emerging economies drives demand.

- Increased adoption of on-site oxygen generation to enhance efficiency and reduce logistics costs.

- Growing demand from the healthcare and medical sectors for various applications.

- Rising focus on sustainable practices and environmental regulations influencing production methods.

- Technological advancements in air separation units (ASUs) leading to higher purity and energy efficiency.

- Expansion of applications in wastewater treatment, electronics manufacturing, and energy sectors.

AI Impact Analysis on Industrial Oxygen

Users frequently inquire about the transformative potential of Artificial intelligence (AI) within the industrial oxygen sector, keen to understand how this technology can enhance operational efficiency, optimize production processes, and ensure supply chain resilience. The analysis reveals a strong user interest in AI's role in predictive maintenance for air separation units (ASUs), real-time process optimization to reduce energy consumption, and intelligent demand forecasting to prevent supply-demand imbalances. These capabilities are crucial for an industry heavily reliant on continuous, energy-intensive operations.

Furthermore, concerns and expectations extend to AI's ability to improve safety protocols, manage complex logistical networks for oxygen distribution, and contribute to overall cost reduction. There is a clear expectation that AI will move beyond simple data analytics to truly autonomous decision-making in production and delivery, leading to more agile and responsive industrial gas operations. The integration of AI is perceived as a critical step towards achieving higher levels of automation, precision, and sustainability in the industrial oxygen supply chain, addressing common challenges related to energy efficiency and operational uptime.

- Process Optimization: AI algorithms optimize air separation unit (ASU) operations for maximum efficiency and yield, reducing energy consumption.

- Predictive Maintenance: AI-driven analytics predict equipment failures in ASUs and distribution infrastructure, minimizing downtime and maintenance costs.

- Demand Forecasting: AI models analyze historical data and external factors to accurately forecast oxygen demand, optimizing production schedules and inventory.

- Supply Chain Management: AI enhances logistics, route optimization, and fleet management for oxygen delivery, ensuring timely and cost-effective distribution.

- Quality Control: AI-powered sensors and analytics monitor oxygen purity in real-time, ensuring compliance with stringent industry standards.

- Energy Efficiency: AI identifies patterns for energy conservation, leading to significant reductions in operational expenditure for oxygen production.

Key Takeaways Industrial Oxygen Market Size & Forecast

The primary insights derived from the industrial oxygen market size and forecast data point towards a robust and sustained growth trajectory, underpinned by the indispensable nature of oxygen in a vast array of industrial processes. A key takeaway for users is the market's resilience and its direct correlation with global industrial output, indicating that as manufacturing, healthcare, and infrastructure development expand, so too will the demand for industrial oxygen. The growth is not merely incremental but is being driven by fundamental shifts in industrial practices, including a greater emphasis on efficiency and environmental compliance, where oxygen plays a crucial role.

Another significant conclusion is the pronounced regional disparities in growth, with Asia Pacific emerging as the dominant and fastest-growing market, largely due to rapid industrialization and urbanization. This suggests that market participants should strategically focus their expansion and investment efforts in these high-growth geographies. Furthermore, the forecast highlights the increasing technological sophistication required in oxygen production and delivery, emphasizing that innovation in areas like on-site generation and energy efficiency will be critical determinants of competitive advantage and market share in the coming years. Users should note the twin drivers of industrial necessity and technological advancement shaping the market's future.

- The industrial oxygen market is set for consistent growth, driven by fundamental industrial demand.

- Asia Pacific remains the leading and fastest-growing region, fueled by rapid industrial expansion.

- Technological advancements, particularly in on-site generation, are pivotal for market evolution and efficiency.

- The healthcare and metal manufacturing sectors will continue to be primary demand drivers.

- Sustainability initiatives and stricter environmental regulations are influencing production methods and demand for cleaner industrial processes.

Industrial Oxygen Market Drivers Analysis

The expansion of the industrial oxygen market is predominantly driven by robust growth across various end-use industries globally. Sectors such as metal manufacturing and fabrication, which includes steel production, welding, and cutting, are significant consumers, with increasing infrastructure development and automotive production fueling their demand. The indispensable role of oxygen in enhancing combustion efficiency and improving product quality in these heavy industries continues to bolster its market trajectory. This steady demand from core manufacturing activities forms the backbone of the market's growth, ensuring a consistent need for industrial oxygen.

Furthermore, the healthcare and pharmaceutical sectors represent another critical growth driver. Industrial oxygen is vital for medical life support, oxygen therapy, and various pharmaceutical manufacturing processes. The global aging population, coupled with rising incidences of respiratory diseases and the expansion of healthcare infrastructure, particularly in developing countries, significantly increases the demand for medical-grade oxygen. Beyond these, the chemical and petrochemical industries rely heavily on oxygen for oxidation processes and synthesis, while environmental applications such as wastewater treatment and pulp & paper bleaching also contribute substantially to market growth by leveraging oxygen for efficient and cleaner operations.

Additionally, technological advancements and a global push towards cleaner industrial processes are indirectly driving the market. The adoption of oxy-fuel combustion in industries like glass and cement, aimed at reducing emissions and improving energy efficiency, necessitates a higher consumption of oxygen. Similarly, the burgeoning electronics industry, particularly semiconductor manufacturing, requires high-purity oxygen for critical processes. These diverse and expanding application areas collectively contribute to the sustained and positive momentum observed in the industrial oxygen market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Metal Manufacturing & Fabrication Industry | +1.2% | Global, especially Asia Pacific, North America | Long-term |

| Expansion of Healthcare & Pharmaceutical Sector | +1.0% | Global | Long-term |

| Increased Demand from Chemical & Petrochemical Industry | +0.9% | Asia Pacific, Middle East, North America | Mid-term |

| Rising Adoption in Wastewater Treatment | +0.8% | Europe, North America, developing Asia | Mid-term |

| Technological Advancements in Industrial Processes (e.g., Oxy-fuel Combustion) | +0.7% | Global | Mid-term |

| Growth in Electronics & Semiconductor Manufacturing | +0.6% | Asia Pacific, North America | Long-term |

Industrial Oxygen Market Restraints Analysis

Despite the positive growth trajectory, the industrial oxygen market faces several significant restraints that could impede its overall expansion. One primary concern is the substantial energy consumption involved in the production of industrial oxygen, particularly through cryogenic air separation units. The fluctuating and often high costs of electricity directly impact the operational expenditures of oxygen producers, making the final product more expensive and potentially reducing demand from cost-sensitive industries. This energy dependency creates a vulnerability to global energy market volatility and can constrain profitability margins for manufacturers.

Another notable restraint is the stringent regulatory landscape governing the production, storage, and transportation of industrial gases, especially for medical and high-purity applications. Compliance with numerous safety, quality, and environmental regulations requires significant capital investment in advanced production facilities and specialized transportation infrastructure. These regulatory burdens can increase operational complexities and costs for market players, particularly smaller enterprises, thereby limiting market entry and expansion opportunities. Adhering to diverse regional and national standards adds another layer of complexity to global market operations.

Furthermore, the logistical challenges associated with transporting and storing oxygen, which is often distributed in liquid form requiring cryogenic conditions, contribute to operational bottlenecks and higher costs. The increasing trend of on-site oxygen generation, while offering benefits to end-users, also poses a competitive threat to traditional bulk oxygen suppliers, potentially eroding their market share. This shift indicates a decentralization of supply, which could impact the business models of large industrial gas companies focused on centralized production and widespread distribution networks. These combined factors necessitate careful strategic planning by market participants to mitigate their adverse effects.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Energy Consumption in Production | -0.8% | Global | Long-term |

| Volatile Raw Material and Energy Prices | -0.7% | Global | Mid-term |

| Stringent Regulatory Landscape for Production & Transport | -0.6% | Europe, North America | Long-term |

| High Transportation and Storage Costs (Cryogenic) | -0.5% | Global | Mid-term |

| Increased Adoption of On-site Generation Facilities by End-users | -0.4% | North America, Europe, Developed Asia | Long-term |

Industrial Oxygen Market Opportunities Analysis

The industrial oxygen market is poised for significant opportunities driven by emerging applications and the global shift towards more sustainable industrial practices. A key opportunity lies in the burgeoning demand from the green steel production sector. As steel manufacturers worldwide aim to reduce their carbon footprint, the adoption of electric arc furnaces (EAFs) and hydrogen-based direct reduced iron (DRI) processes, both of which require substantial amounts of industrial oxygen, is set to increase. This transition offers a substantial new market segment for oxygen suppliers, aligning with global climate goals and creating a long-term demand driver.

Furthermore, advancements in healthcare and the increasing complexity of medical procedures present new avenues for oxygen applications beyond traditional life support. High-purity oxygen is becoming crucial for advanced medical devices, diagnostics, and specialized therapies, particularly in rapidly urbanizing regions with expanding healthcare infrastructure. This evolution of healthcare services, coupled with the increasing focus on patient care and advanced medical research, creates a sustained demand for industrial oxygen with stringent purity requirements, opening up lucrative niche markets for specialized suppliers.

Another significant opportunity stems from the global focus on environmental protection and resource efficiency. The use of oxygen in carbon capture, utilization, and storage (CCUS) technologies, as well as enhanced oil recovery (EOR) and advanced wastewater treatment processes, is gaining traction. As industries face stricter emissions regulations and pursue circular economy models, oxygen offers solutions for cleaner production and waste management. Moreover, the long-term potential for oxygen in future energy systems, such as in integrated gasification combined cycle (IGCC) power plants and hydrogen fuel cell production, positions the market for sustained growth in the evolving energy landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand from Green Steel Production & Hydrogen Production | +1.2% | Europe, Asia Pacific, North America | Long-term |

| Emerging Applications in Carbon Capture, Utilization, and Storage (CCUS) | +1.0% | North America, Europe, Asia Pacific | Long-term |

| Expansion of Advanced Healthcare & Medical Applications | +0.9% | Global, especially developing regions | Mid-term |

| Increased Utilization in Enhanced Oil Recovery (EOR) | +0.8% | Middle East, North America | Mid-term |

| Growth in Water & Wastewater Treatment Technologies | +0.7% | Global | Mid-term |

Industrial Oxygen Market Challenges Impact Analysis

The industrial oxygen market faces several inherent challenges that demand strategic responses from market participants. One significant challenge is the inherent capital intensity associated with setting up and maintaining large-scale air separation units (ASUs) and the extensive distribution networks required for oxygen supply. The initial investment in cryogenic plants, storage tanks, and specialized transportation vehicles is substantial, creating high barriers to entry for new players and requiring existing companies to continuously invest in infrastructure upgrades. This capital burden can strain financial resources and slow down market expansion, particularly in regions with limited investment capital.

Furthermore, maintaining a consistent and reliable supply chain for industrial oxygen presents considerable challenges, especially given the gas's cryogenic nature when transported as liquid oxygen. Disruptions caused by geopolitical events, natural disasters, or labor shortages can severely impact the availability and cost of oxygen, affecting critical end-use industries that depend on an uninterrupted supply. The need for specialized logistics and handling also adds to the operational complexity and cost, making the supply chain vulnerable to external shocks and increasing the risk of price volatility, which can deter long-term contracts from end-users.

Another challenge is the competitive pressure stemming from the increasing adoption of on-site oxygen generation technologies by large industrial consumers. While beneficial for specific high-volume users, this trend reduces the reliance on merchant suppliers, potentially impacting their revenue streams and market dominance. Additionally, the industry is perpetually challenged by the need to continuously innovate and improve energy efficiency in production processes to mitigate the impact of rising energy costs and environmental regulations. Balancing technological advancement with economic viability and regulatory compliance remains a persistent hurdle for market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Production Facilities | -0.7% | Global | Long-term |

| Complex Logistics & Transportation of Cryogenic Oxygen | -0.6% | Global | Mid-term |

| Intense Competition from On-Site Generation Solutions | -0.5% | North America, Europe | Long-term |

| Fluctuations in Energy Prices and Operating Costs | -0.5% | Global | Short-term |

| Environmental Regulations and Compliance Costs | -0.4% | Europe, North America | Mid-term |

Industrial Oxygen Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Industrial Oxygen Market, encompassing detailed insights into market dynamics, segmentation, regional landscapes, and competitive intensity. The scope covers historical trends from 2019 to 2023, offering a robust foundation for understanding past performance and influencing factors. The forecast period extends from 2025 to 2033, projecting future market growth, opportunities, and challenges across various industry verticals. This report is designed to assist stakeholders in making informed strategic decisions by delivering a clear understanding of market evolution and key influencing factors.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 45.2 Billion |

| Market Forecast in 2033 | USD 75.1 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Linde plc, Air Liquide S.A., Air Products and Chemicals, Inc., Messer Group GmbH, Taiyo Nippon Sanso Corporation, SOL Group, Matheson Tri-Gas Inc., Gulf Cryo, Asia Industrial Gases Pte. Ltd., Iwatani Corporation, Showa Denko K.K., Sichuan Air Separation Plant Group, Hangyang Group Co., Ltd., INOX Air Products Pvt. Ltd., Nanjing Tianshi Co., Ltd., Beijing Shougang Oxygen Plant Co., Ltd. (BSOP), Universal Industrial Gases, Inc. (UIG), PT Aneka Gas Industri Tbk., Praxair (a Linde company), Chemix Gas Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial oxygen market is highly segmented based on various critical parameters, allowing for a granular understanding of demand patterns, production methods, and application-specific requirements across different industries. This comprehensive segmentation helps to identify specific growth pockets and market dynamics within each category, from the physical state of oxygen to its ultimate end-use. Understanding these segments is crucial for market participants to tailor their product offerings, optimize production processes, and develop targeted marketing strategies.

- By Type: This segment differentiates between the physical forms in which industrial oxygen is supplied.

- Gaseous Oxygen

- Liquid Oxygen

- By Purity: Reflects the varying purity levels required for different industrial applications.

- High Purity

- Medium Purity

- Low Purity

- By Application: Categorizes oxygen consumption based on its specific use in various industrial processes.

- Metal Manufacturing & Fabrication: Includes steel production, welding & cutting, and non-ferrous metals processing.

- Chemical Processing: Encompasses oxidation reactions, ethylene oxide production, and hydrogen peroxide production.

- Healthcare & Medical: Covers life support systems, oxygen therapy, and applications in medical devices.

- Pulp & Paper: Utilized for bleaching and delignification processes.

- Water Treatment: Applied in aeration and ozone generation for purification.

- Electronics: Crucial for semiconductor manufacturing processes.

- Aerospace & Defense: Used in rocket propellants and life support systems.

- Glass Manufacturing: Enhances combustion efficiency in furnaces.

- Energy: Includes oxy-fuel combustion and gasification technologies.

- By End-Use Industry: Classifies market demand based on the primary industry consuming industrial oxygen.

- Manufacturing

- Healthcare & Pharmaceutical

- Food & Beverage

- Mining

- Construction

- Environmental Services

- Automotive

- By Production Method: Distinguishes between the technologies employed for oxygen generation.

- Cryogenic Air Separation

- Non-Cryogenic Air Separation: Includes Pressure Swing Adsorption (PSA), Vacuum Swing Adsorption (VSA), and Membrane Separation.

Regional Highlights

- Asia Pacific (APAC): Dominates the industrial oxygen market and is projected to be the fastest-growing region. This growth is primarily fueled by rapid industrialization, burgeoning manufacturing sectors in countries like China, India, and Southeast Asian nations, and substantial investments in infrastructure development, steel production, and electronics manufacturing. The expanding healthcare sector and increasing environmental regulations also contribute significantly to demand.

- North America: Represents a mature yet stable market for industrial oxygen, driven by established industries such as metal fabrication, chemical processing, and a highly developed healthcare sector in the United States and Canada. The region also exhibits increasing adoption of advanced on-site generation technologies and a growing focus on clean energy initiatives.

- Europe: A significant market characterized by stringent environmental regulations, advanced manufacturing processes, and a strong emphasis on sustainability. Demand is driven by the chemical industry, healthcare advancements, and a move towards greener industrial practices, particularly in Germany, France, and the UK. Investments in carbon capture and hydrogen production also contribute to market growth.

- Latin America: Expected to witness steady growth, primarily influenced by expanding industrial activities in Brazil and Mexico, particularly in mining, automotive manufacturing, and chemical production. Investments in healthcare infrastructure and resource exploration also contribute to the rising demand for industrial oxygen.

- Middle East and Africa (MEA): Emerging as a high-growth region due to significant investments in oil & gas, petrochemicals, and infrastructure development. Countries like Saudi Arabia and the UAE are expanding their industrial bases, leading to increased demand for industrial oxygen in refining, metal production, and water treatment applications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Oxygen Market.- Linde plc

- Air Liquide S.A.

- Air Products and Chemicals, Inc.

- Messer Group GmbH

- Taiyo Nippon Sanso Corporation

- SOL Group

- Matheson Tri-Gas Inc.

- Gulf Cryo

- Asia Industrial Gases Pte. Ltd.

- Iwatani Corporation

- Showa Denko K.K.

- Sichuan Air Separation Plant Group

- Hangyang Group Co., Ltd.

- INOX Air Products Pvt. Ltd.

- Nanjing Tianshi Co., Ltd.

- Beijing Shougang Oxygen Plant Co., Ltd. (BSOP)

- Universal Industrial Gases, Inc. (UIG)

- PT Aneka Gas Industri Tbk.

- Praxair (a Linde company)

- Chemix Gas Co., Ltd.

Frequently Asked Questions

What is industrial oxygen and how is it primarily used?

Industrial oxygen is a high-purity gas used in various manufacturing, healthcare, and environmental applications. Its primary uses include enhancing combustion in metal fabrication and steel production, supporting life in medical facilities, and serving as a chemical reactant in processes like wastewater treatment and petrochemical synthesis.

What are the key drivers of growth in the Industrial Oxygen Market?

Key growth drivers include rapid industrialization in emerging economies, expanding healthcare infrastructure and demand for medical oxygen, increased adoption in metal manufacturing and fabrication, and growing applications in environmental protection such as wastewater treatment and carbon capture technologies.

Which region holds the largest share in the Industrial Oxygen Market, and why?

The Asia Pacific region holds the largest market share due to its rapid industrial growth, significant investments in manufacturing and infrastructure, and the expansion of key end-use industries like steel, chemicals, and electronics in countries such as China and India.

What are the main challenges faced by the Industrial Oxygen Market?

Major challenges include high capital expenditure for production facilities, complex logistics and transportation of cryogenic oxygen, volatile energy prices impacting production costs, and increasing competition from on-site oxygen generation solutions adopted by large industrial consumers.

How is technological innovation impacting the Industrial Oxygen Market?

Technological innovations are enhancing market efficiency and sustainability by improving air separation unit (ASU) energy efficiency, enabling advanced on-site generation, and optimizing supply chain management through digitalization and AI, leading to higher purity and more cost-effective supply.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted