Wireless Infrastructure Market

Wireless Infrastructure Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703172 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

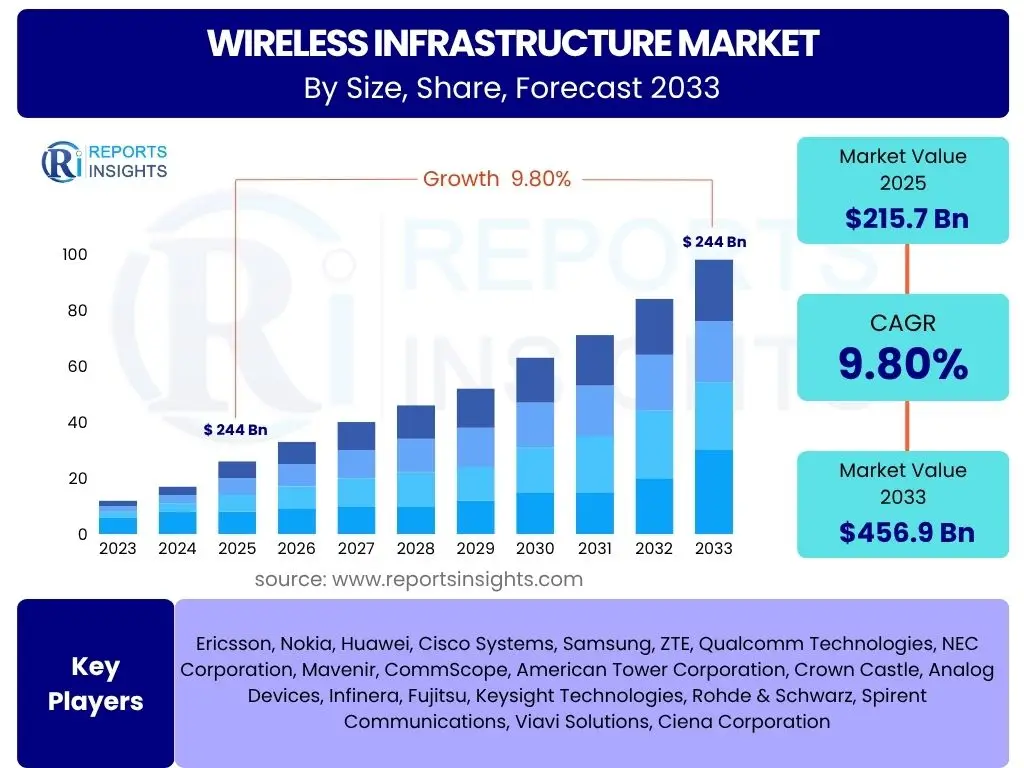

Wireless Infrastructure Market Size

According to Reports Insights Consulting Pvt Ltd, The Wireless Infrastructure Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 215.7 Billion in 2025 and is projected to reach USD 456.9 Billion by the end of the forecast period in 2033.

Key Wireless Infrastructure Market Trends & Insights

User inquiries frequently highlight the dynamic evolution of the Wireless Infrastructure market, focusing on the rapid deployment of next-generation technologies and the expansion of connectivity solutions. A significant trend is the global rollout of 5G networks, which demands substantial upgrades to existing infrastructure, including denser cell sites, massive MIMO antennas, and advanced backhaul solutions. This foundational shift is not merely about speed but enabling new use cases like augmented reality, virtual reality, and mission-critical communications across various sectors. The focus extends to ensuring robust, low-latency, and high-capacity networks that can support an increasingly interconnected world.

Another area of keen interest revolves around the adoption of Open Radio Access Networks (Open RAN) and the virtualization of network functions, signifying a move towards more open, interoperable, and software-defined architectures. This trend is driven by a desire for reduced vendor lock-in, increased innovation, and greater flexibility in network deployment and management. Furthermore, the proliferation of Internet of Things (IoT) devices across consumer, industrial, and smart city applications necessitates a ubiquitous and resilient wireless infrastructure capable of handling diverse connectivity requirements, from low-power wide-area networks to ultra-reliable low-latency communications. These trends collectively underscore a market moving towards greater intelligence, efficiency, and adaptability.

- Accelerated global deployment of 5G and preparations for 6G technologies.

- Increasing adoption of Open RAN and network virtualization solutions.

- Expansion of private wireless networks for enterprise and industrial applications.

- Growing integration of edge computing capabilities with wireless networks.

- Rising demand for satellite-based communication solutions for ubiquitous coverage.

- Focus on sustainable and energy-efficient network infrastructure.

- Emphasis on network densification and small cell deployment.

AI Impact Analysis on Wireless Infrastructure

User queries regarding AI's impact on wireless infrastructure frequently revolve around its potential to optimize network performance, enhance operational efficiency, and introduce autonomous capabilities. There is considerable interest in how Artificial intelligence (AI) can move beyond reactive network management to predictive analytics, enabling proactive identification and resolution of issues before they affect service quality. Users are keen to understand how AI-driven insights can lead to more efficient resource allocation, reduced energy consumption, and improved customer experience by dynamically adapting network parameters to changing traffic patterns and user demands. This includes the application of machine learning algorithms to analyze vast datasets generated by network elements, identifying anomalies, and forecasting future network requirements.

Furthermore, concerns and expectations are high concerning AI's role in security, where advanced algorithms can detect and mitigate cyber threats in real-time within complex wireless environments. The concept of self-optimizing networks (SON) and ultimately self-healing networks, empowered by AI, is a significant draw, promising to minimize human intervention and operational costs while maximizing uptime and reliability. There is also an expectation that AI will be instrumental in the planning and design phases of network deployment, optimizing site selection, antenna placement, and overall network architecture for optimal coverage and capacity. The convergence of AI with wireless infrastructure is viewed as a critical enabler for the next generation of intelligent, resilient, and highly efficient communication systems.

- Enhanced network optimization and dynamic resource allocation through AI algorithms.

- Predictive maintenance and fault detection for improved network reliability.

- Automated network operations, including self-healing and self-organizing capabilities.

- Advanced cybersecurity threat detection and prevention in wireless networks.

- Optimized network planning and design using AI-driven simulation and analytics.

- Improved energy efficiency in network components through AI-controlled power management.

- Personalized user experiences and service provisioning based on AI insights.

Key Takeaways Wireless Infrastructure Market Size & Forecast

Common user questions regarding key takeaways from the Wireless Infrastructure market size and forecast consistently point towards an eagerness to understand the core growth drivers, the pace of technological evolution, and the long-term investment landscape. Users are primarily seeking clarity on why the market is expanding at its projected CAGR, often linking this to the foundational role of connectivity in global digital transformation. The rapid advancements in communication technologies, particularly 5G and the nascent stages of 6G, are recognized as primary catalysts for market expansion, necessitating continuous infrastructure upgrades and expansions globally.

The insights reveal a market characterized by substantial capital expenditure, driven by both public and private sector investments aiming to bridge the digital divide and support innovative applications from smart cities to industrial automation. Moreover, the shift towards open, virtualized, and software-defined networks is a critical strategic takeaway, indicating a move towards more flexible and cost-efficient deployment models. The sustained growth trajectory is underpinned by an increasing global demand for high-speed, reliable, and ubiquitous connectivity, positioning wireless infrastructure as an indispensable component of the modern economy. This sustained demand, coupled with technological innovation, ensures the market's robust future, attracting continued investment and fostering competitive development.

- Robust market growth driven by global 5G expansion and future 6G preparations.

- Significant investment flowing into network densification and fiber optic backhaul.

- Technological advancements like Open RAN are reshaping network architectures.

- Increasing enterprise adoption of private wireless networks for critical applications.

- Ubiquitous connectivity demand from IoT and emerging digital services.

- Market evolution towards more intelligent, software-defined, and energy-efficient networks.

Wireless Infrastructure Market Drivers Analysis

The Wireless Infrastructure market is experiencing significant growth propelled by several robust drivers. The pervasive demand for high-speed, low-latency connectivity, especially in the wake of escalating mobile data consumption and the proliferation of connected devices, stands as a fundamental catalyst. The global push for 5G network deployment is paramount, requiring extensive investments in new base stations, small cells, massive MIMO antennas, and upgraded core networks to support its capabilities. This foundational shift is creating a sustained demand for advanced infrastructure components and services. Furthermore, the rapid growth of the Internet of Things (IoT) across various sectors, from smart homes and cities to industrial automation, necessitates a robust and pervasive wireless backbone capable of supporting billions of diverse connections. This expansion drives the need for enhanced network capacity, coverage, and reliability.

Beyond technological imperatives, governmental initiatives and regulatory frameworks also play a crucial role in market expansion. Policies aimed at improving digital inclusion, fostering innovation, and allocating spectrum efficiently encourage significant infrastructure investments. The increasing adoption of cloud services and edge computing architectures further accelerates the demand for robust wireless connectivity, as data processing moves closer to the source to reduce latency and improve performance. Additionally, the emergence of new revenue streams through private networks and network slicing is incentivizing telecommunication companies and enterprises to invest in advanced wireless infrastructure, tailored to specific industry needs and use cases. These combined factors create a compelling environment for sustained market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global 5G Network Deployment | +2.5% | North America, Asia Pacific, Europe | 2025-2033 |

| Proliferation of IoT Devices & Applications | +1.8% | Global, particularly developed economies | 2025-2033 |

| Increasing Mobile Data Traffic & Cloud Adoption | +1.5% | Global | 2025-2033 |

| Government Initiatives for Digital Connectivity | +1.2% | Emerging Economies, specific national policies | 2025-2030 |

| Rise of Private Wireless Networks | +1.0% | Industrialized Nations, Enterprise Sector | 2026-2033 |

Wireless Infrastructure Market Restraints Analysis

Despite the strong growth drivers, the Wireless Infrastructure market faces several significant restraints that could temper its expansion. One of the primary challenges is the substantial capital expenditure required for deploying and upgrading network infrastructure, especially for dense 5G networks and fiber optic backhaul. The high upfront investment, coupled with potentially long return on investment periods, can deter smaller players and limit the pace of expansion, particularly in regions with less mature telecommunications markets. Additionally, regulatory complexities and delays in obtaining permits for site acquisition and tower construction pose considerable hurdles. Diverse zoning laws, environmental regulations, and local community resistance can significantly slow down deployment timelines and increase project costs, creating bottlenecks in network rollout.

Another major restraint is the scarcity and high cost of spectrum licenses, which are essential for wireless communication. Limited available spectrum and the competitive bidding processes for new bands can drive up operational costs for mobile network operators, directly impacting their ability to invest further in infrastructure. Furthermore, increasing concerns regarding cybersecurity threats and data privacy present a growing challenge. As networks become more complex and interconnected, the attack surface expands, requiring significant investment in advanced security measures. The global supply chain volatility, skilled labor shortages, and rising energy costs for operating network equipment also contribute to the restraints, creating an intricate landscape that necessitates strategic planning and innovation to overcome these limiting factors and ensure sustained market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and ROI Concerns | -1.5% | Global, particularly developing regions | 2025-2033 |

| Complex Regulatory & Permitting Processes | -1.2% | Global, country-specific variances | 2025-2033 |

| Spectrum Scarcity and Cost | -1.0% | Global, highly competitive markets | 2025-2030 |

| Cybersecurity Threats & Data Privacy Concerns | -0.8% | Global | 2025-2033 |

| Skilled Labor Shortage & Supply Chain Issues | -0.7% | Global, localized impact | 2025-2029 |

Wireless Infrastructure Market Opportunities Analysis

The Wireless Infrastructure market is ripe with opportunities driven by technological advancements and evolving connectivity demands. The burgeoning interest in Open Radio Access Networks (Open RAN) presents a significant opportunity by promoting vendor diversity, fostering innovation, and potentially reducing network deployment and operational costs. This shift towards disaggregated and software-defined architectures allows for greater flexibility and customization, opening doors for new entrants and specialized solution providers. Furthermore, the expansion of private 5G networks for industrial campuses, smart factories, and enterprise environments offers a lucrative niche, as businesses seek dedicated, secure, and highly reliable connectivity tailored to their specific operational needs. This segment allows for monetization beyond traditional consumer services, tapping into vast industrial and commercial applications.

Another substantial opportunity lies in the development and deployment of satellite-based communication systems, particularly Low Earth Orbit (LEO) constellations. These systems promise to extend broadband connectivity to underserved and remote areas globally, complementing terrestrial networks and addressing the digital divide. The increasing focus on network densification through small cell deployments in urban and suburban areas also provides an ongoing opportunity, as these solutions are crucial for managing escalating data traffic and improving indoor coverage for 5G. Additionally, the integration of Artificial Intelligence (AI) and Machine Learning (ML) for network automation, optimization, and predictive maintenance creates avenues for developing and deploying intelligent infrastructure solutions that enhance efficiency, reliability, and security. These opportunities collectively highlight a dynamic market poised for innovative solutions and strategic growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Open RAN Architectures | +1.7% | North America, Europe, Asia Pacific | 2026-2033 |

| Expansion of Private 5G Networks | +1.5% | Industrialized Nations, Enterprise Sector | 2025-2033 |

| Growth of Satellite Communication (LEO) | +1.3% | Global, underserved and remote areas | 2027-2033 |

| Network Densification via Small Cell Deployments | +1.0% | Urban and densely populated areas globally | 2025-2033 |

| AI/ML Integration for Network Automation | +0.9% | Global, particularly advanced markets | 2025-2033 |

Wireless Infrastructure Market Challenges Impact Analysis

The Wireless Infrastructure market, while experiencing significant growth, is not without its challenges. One prominent challenge is the increasing energy consumption of network infrastructure, especially with the densification of 5G networks and the proliferation of data centers. The rising cost of energy and growing environmental concerns necessitate a significant shift towards more energy-efficient equipment and renewable energy sources, which often require substantial initial investments. Another critical challenge is ensuring seamless interoperability between various network components and vendors, particularly with the rise of Open RAN and disaggregated architectures. Achieving true interoperability requires rigorous testing and standardization efforts, without which network fragmentation and operational inefficiencies can arise, hindering wider adoption.

Cybersecurity threats represent a persistent and escalating challenge for wireless infrastructure. As networks become more complex, software-defined, and interconnected, they become more vulnerable to sophisticated attacks, including denial-of-service, data breaches, and ransomware. Protecting critical infrastructure from these evolving threats requires continuous investment in advanced security solutions, real-time monitoring, and highly skilled personnel. Furthermore, the rapid pace of technological evolution poses a challenge in terms of future-proofing investments. Operators and enterprises must constantly balance immediate deployment needs with the imperative to build flexible and scalable infrastructure that can adapt to future innovations, such as 6G and advanced AI applications, without becoming obsolete too quickly. These challenges demand innovative solutions, collaborative efforts, and strategic foresight to maintain market momentum and ensure network resilience.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Energy Consumption & Sustainability Pressure | -1.0% | Global | 2025-2033 |

| Interoperability and Standardization Issues | -0.8% | Global, particularly for Open RAN | 2025-2030 |

| Evolving Cybersecurity Threats & Network Vulnerabilities | -0.7% | Global | 2025-2033 |

| Rapid Technological Obsolescence & Future-Proofing | -0.6% | Global, highly innovative markets | 2025-2033 |

| Right-of-Way and Site Acquisition Difficulties | -0.5% | Dense urban areas, specific countries | 2025-2033 |

Wireless Infrastructure Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Wireless Infrastructure market, detailing its current size, historical performance, and future growth projections through 2033. It encompasses a thorough examination of key market trends, significant drivers, restraining factors, emerging opportunities, and critical challenges shaping the industry landscape. The report delivers a granular segmentation analysis across various components, technologies, applications, and deployment models, offering detailed insights into each segment's contribution and growth potential. Furthermore, it highlights regional dynamics and competitive landscapes, profiling leading market players to provide a holistic view of the market's structure and competitive intensity.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 215.7 Billion |

| Market Forecast in 2033 | USD 456.9 Billion |

| Growth Rate | 9.8% CAGR |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ericsson, Nokia, Huawei, Cisco Systems, Samsung, ZTE, Qualcomm Technologies, NEC Corporation, Mavenir, CommScope, American Tower Corporation, Crown Castle, Analog Devices, Infinera, Fujitsu, Keysight Technologies, Rohde & Schwarz, Spirent Communications, Viavi Solutions, Ciena Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Wireless Infrastructure market is comprehensively segmented to provide a detailed understanding of its diverse components, technologies, applications, and deployment models. This granular segmentation helps in identifying specific growth pockets, understanding regional nuances, and recognizing the interplay between various market elements. The market is primarily divided by component, reflecting the physical and virtual aspects of network architecture, including hardware essential for connectivity, software for network intelligence and management, and a wide array of services necessary for the entire lifecycle of wireless networks. Understanding these components is critical for stakeholders looking to invest in specific areas of the infrastructure value chain.

Further segmentation by technology highlights the ongoing evolution from legacy 2G/3G systems to the dominant 4G/LTE, and critically, the rapidly expanding 5G networks, alongside specialized technologies like Wi-Fi and satellite communications. This technological breakdown illustrates the shift towards more advanced, high-capacity, and low-latency communication standards. Application-based segmentation reveals how wireless infrastructure serves various end-user sectors, from residential and commercial use to critical industrial and public safety applications, demonstrating the pervasive impact of robust connectivity. Finally, deployment models differentiate between indoor and outdoor, and public versus private networks, reflecting the varied architectural approaches tailored to different environments and user requirements. Each segment holds unique growth potential and is influenced by specific market dynamics, making this analysis vital for strategic planning.

- By Component:

- Hardware: Antennas, Base Stations, Small Cells, Core Network Equipment, Optical Fibers, Others

- Software: Network Management, Orchestration, Security

- Services: Installation, Maintenance, Consulting, Professional Services

- By Technology:

- 2G/3G

- 4G/LTE

- 5G

- Wi-Fi

- Satellite

- Others (LoRaWAN, NB-IoT)

- By Application:

- Residential

- Commercial

- Industrial

- Public Safety

- Smart Cities

- Defense

- By Deployment:

- Indoor

- Outdoor

- Public

- Private

Regional Highlights

- North America: The region is a pioneer in 5G adoption and network virtualization, exhibiting high investments in advanced wireless infrastructure, particularly in urban densification and enterprise private networks. Strong presence of key market players and robust R&D activities contribute to its leading position.

- Europe: Characterized by significant 5G rollout across member states and increasing focus on Open RAN initiatives. Regulatory support for digital transformation and smart city projects drives infrastructure development, though spectrum allocation remains a key focus.

- Asia Pacific (APAC): Represents the largest and fastest-growing market due to massive subscriber bases, aggressive 5G deployments in countries like China, India, and South Korea, and burgeoning demand from industrial IoT and smart urban development. Government-led digital infrastructure projects are a major catalyst.

- Latin America: Experiencing growing demand for high-speed internet and mobile connectivity, leading to increasing investments in 4G and nascent 5G infrastructure. Policy efforts to expand digital access and reduce the digital divide are driving market expansion.

- Middle East and Africa (MEA): Marked by substantial infrastructure development efforts, particularly in the Middle East with ambitious smart city projects and high mobile penetration. Africa is focusing on expanding basic connectivity and improving network coverage in underserved areas, driven by population growth and digital inclusion initiatives.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wireless Infrastructure Market.- Ericsson

- Nokia

- Huawei

- Cisco Systems

- Samsung

- ZTE

- Qualcomm Technologies

- NEC Corporation

- Mavenir

- CommScope

- American Tower Corporation

- Crown Castle

- Analog Devices

- Infinera

- Fujitsu

- Keysight Technologies

- Rohde & Schwarz

- Spirent Communications

- Viavi Solutions

- Ciena Corporation

Frequently Asked Questions

What is driving the growth of the Wireless Infrastructure Market?

The Wireless Infrastructure Market's growth is primarily driven by the global deployment of 5G networks, the exponential rise in mobile data traffic, the widespread proliferation of IoT devices, and governmental initiatives aimed at enhancing digital connectivity. Additionally, the increasing adoption of cloud services and the emergence of private wireless networks are significant contributors to market expansion.

How is Artificial Intelligence (AI) impacting wireless infrastructure?

AI is profoundly impacting wireless infrastructure by enabling advanced network optimization, predictive maintenance, and autonomous operations. It enhances efficiency in resource allocation, improves network security through intelligent threat detection, and facilitates smarter network planning, ultimately leading to more reliable, energy-efficient, and self-managing communication systems.

What are the key technological trends shaping the market?

Key technological trends include the accelerated global rollout of 5G and early preparations for 6G, the increasing adoption of Open Radio Access Networks (Open RAN) for more flexible architectures, and the deep integration of edge computing. The market is also seeing a surge in demand for private wireless networks and the expansion of satellite communication solutions for broader coverage.

What challenges does the Wireless Infrastructure Market face?

The market faces several challenges, including the substantial capital expenditure required for network upgrades, complex regulatory environments, and the scarcity of affordable spectrum. Other challenges include persistent cybersecurity threats, the high energy consumption of dense networks, and the rapid pace of technological evolution requiring continuous adaptation and investment.

Which regions are key contributors to the Wireless Infrastructure Market?

Asia Pacific is the largest and fastest-growing market due to extensive 5G deployments and high subscriber numbers. North America leads in innovation and early adoption of advanced technologies, while Europe focuses on 5G rollout and Open RAN. Latin America and MEA are experiencing growth through infrastructure development and efforts to bridge the digital divide.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted