Optical Communication and Networking Equipment Market

Optical Communication and Networking Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703455 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

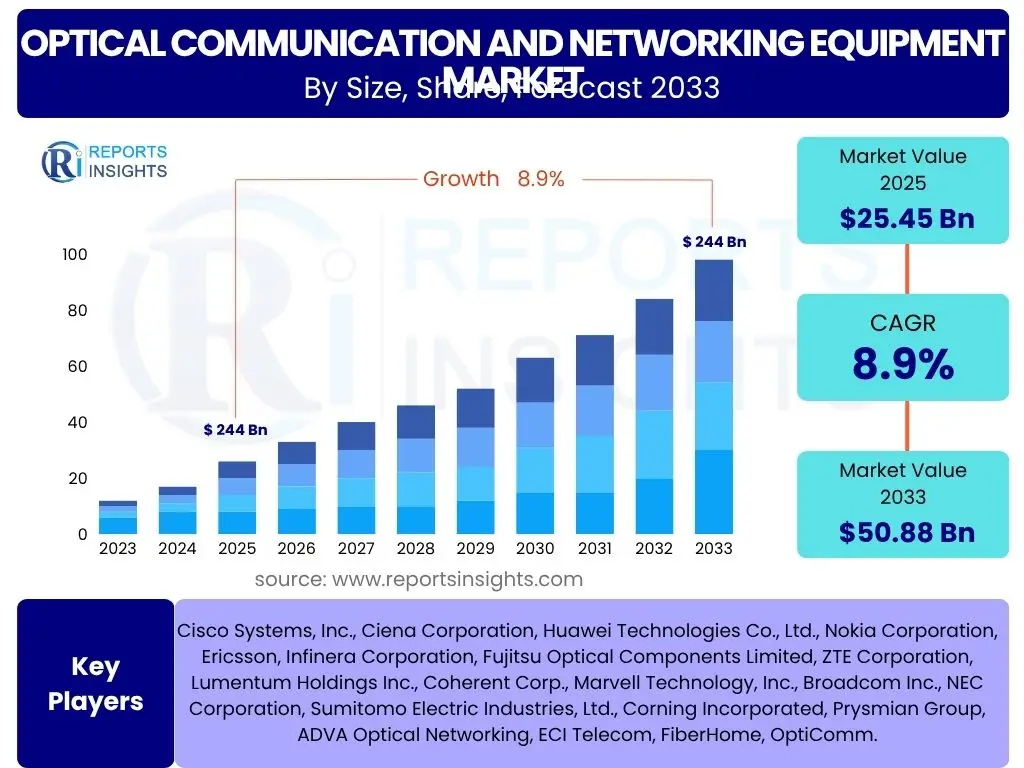

Optical Communication and Networking Equipment Market Size

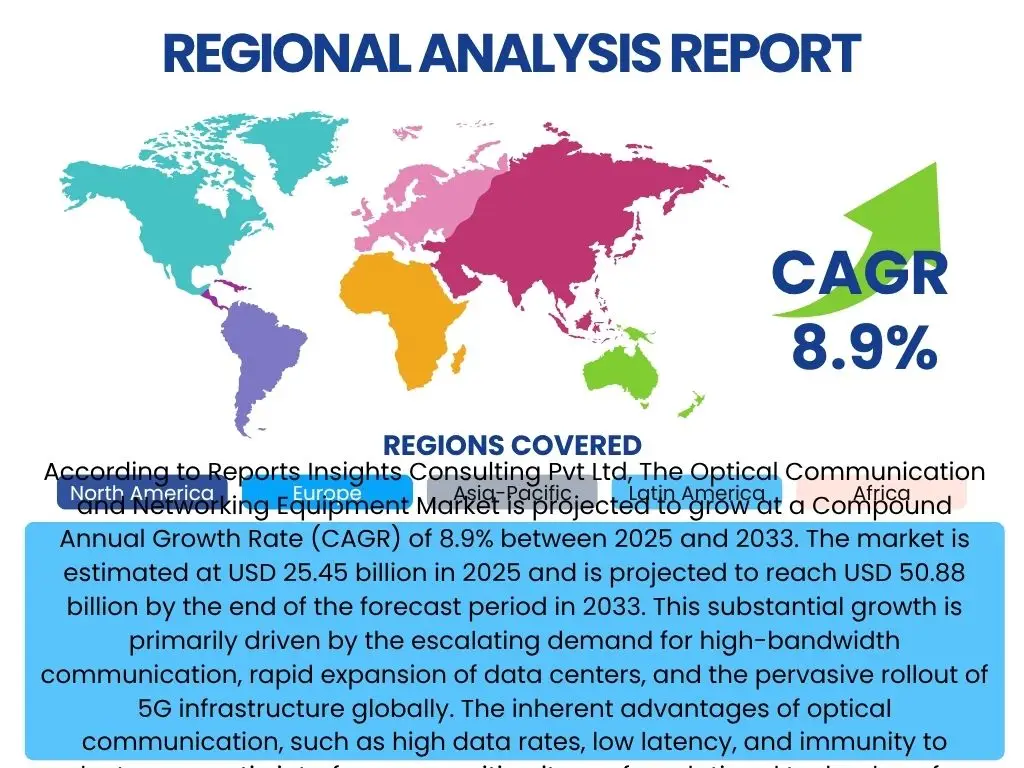

According to Reports Insights Consulting Pvt Ltd, The Optical Communication and Networking Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 25.45 billion in 2025 and is projected to reach USD 50.88 billion by the end of the forecast period in 2033. This substantial growth is primarily driven by the escalating demand for high-bandwidth communication, rapid expansion of data centers, and the pervasive rollout of 5G infrastructure globally. The inherent advantages of optical communication, such as high data rates, low latency, and immunity to electromagnetic interference, position it as a foundational technology for next-generation networks.

The market's expansion is further bolstered by continuous technological advancements, including the development of coherent optical technologies, disaggregated network architectures, and photonics integration. Investments in hyperscale data centers and the increasing adoption of cloud computing services necessitate robust and scalable optical network solutions. Governments and private entities worldwide are committing significant capital to upgrade existing communication infrastructures, particularly in emerging economies, to support digital transformation initiatives and bridge the digital divide. This concerted effort contributes significantly to the market's positive trajectory over the forecast period.

Key Optical Communication and Networking Equipment Market Trends & Insights

The optical communication and networking equipment market is currently experiencing dynamic shifts driven by several pivotal trends that users frequently inquire about. These trends revolve around the insatiable demand for bandwidth, the evolution of network architectures, and the integration of advanced technologies. Users are keen to understand how phenomena like the proliferation of 5G, the expansion of cloud services, and the push towards network automation are reshaping the industry, leading to more efficient, scalable, and intelligent optical networks. The focus is increasingly on achieving higher speeds, lower power consumption, and greater flexibility within optical infrastructures to support diverse and demanding applications.

Furthermore, there is significant interest in the transition towards open and disaggregated optical networks, which promise to reduce vendor lock-in and foster innovation through multi-vendor interoperability. Coherent optical technology continues to advance, enabling higher capacities over longer distances, while efforts in quantum networking are laying the groundwork for future secure communication paradigms. The convergence of wired and wireless networks, alongside the growing need for robust cybersecurity measures within optical layers, also represent critical areas of development and concern for market stakeholders and users alike.

- 5G Network Rollout: Extensive deployment of 5G infrastructure globally, requiring denser fiber optic networks and high-capacity backhaul solutions.

- Hyperscale Data Center Expansion: Continuous growth of cloud computing and AI workloads necessitating massive inter-data center and intra-data center optical connectivity.

- Coherent Optical Technology Advancements: Evolution of high-speed coherent modules (400GbE, 800GbE, and beyond) for enhanced spectral efficiency and reach.

- Network Disaggregation and Open Optical Networks: Shift towards open interfaces and separate hardware/software layers for greater flexibility, cost-effectiveness, and multi-vendor interoperability.

- Edge Computing Proliferation: Increased demand for optical connectivity at the network edge to support low-latency applications and distributed processing.

- Photonics Integration: Miniaturization and integration of optical components onto a single chip, leading to smaller, more power-efficient devices.

- Software-Defined Networking (SDN) and Network Function Virtualization (NFV): Adoption of software-centric approaches for dynamic network management and resource allocation in optical networks.

- Quantum Networking Research and Development: Early-stage exploration and development of quantum communication for ultra-secure data transmission.

AI Impact Analysis on Optical Communication and Networking Equipment

Users frequently inquire about the transformative potential of Artificial Intelligence (AI) within the optical communication and networking equipment sector. Common questions center on how AI can enhance network performance, automate complex operations, and improve resource utilization. The consensus among market observers is that AI is poised to revolutionize network management by enabling more proactive, self-optimizing, and resilient optical infrastructures. AI's capabilities in analyzing vast amounts of network data, identifying patterns, and predicting potential issues are critical for managing the increasing complexity and scale of modern optical networks, moving beyond traditional manual configurations.

The integration of AI is expected to lead to significant operational efficiencies, reduced human intervention, and improved service quality. While the benefits are substantial, users also express concerns regarding the initial investment in AI infrastructure, the need for specialized skills, and data privacy implications. Despite these challenges, the long-term vision for AI in optical networking involves creating truly autonomous networks that can intelligently adapt to changing demands, optimize traffic flow, and rapidly self-heal from disruptions, thereby minimizing downtime and enhancing the overall user experience.

- Automated Network Operations: AI-powered algorithms enable self-configuration, self-optimization, and self-healing capabilities in optical networks, reducing manual intervention and operational costs.

- Predictive Maintenance: AI analyzes network performance data to predict potential equipment failures or degradation, allowing for proactive maintenance and minimizing downtime.

- Intelligent Traffic Management: AI optimizes data routing and resource allocation in real-time, improving network efficiency, reducing congestion, and ensuring quality of service for diverse applications.

- Enhanced Network Security: AI identifies anomalous traffic patterns and potential cyber threats within the optical layer, bolstering security and protecting sensitive data.

- Resource Optimization: AI algorithms dynamically adjust power consumption, bandwidth allocation, and fiber utilization to maximize network efficiency and sustainability.

- Network Planning and Design: AI assists in simulating network scenarios and optimizing infrastructure design, leading to more robust and cost-effective deployments.

Key Takeaways Optical Communication and Networking Equipment Market Size & Forecast

Analysis of common user questions regarding the optical communication and networking equipment market size and forecast reveals a strong interest in understanding the underlying growth drivers, the longevity of the market's expansion, and the impact of technological evolution. Users seek clarity on why the market is projected for significant growth and what factors will sustain this trajectory through 2033. The key insights emphasize that the market's robust expansion is not merely a short-term surge but a sustained trend fueled by fundamental shifts in global digital consumption patterns and infrastructure requirements, particularly the escalating demand for high-speed, reliable connectivity across various sectors.

The market is poised for sustained expansion, driven by the indispensable role of optical networks in supporting critical global digital infrastructure. Key takeaways highlight the transformative impact of 5G, cloud computing, and advanced data center technologies as primary catalysts. Moreover, the report underscores the continuous innovation in optical technologies, such as coherent optics and photonics integration, which are crucial for meeting future bandwidth demands. These elements collectively paint a picture of a dynamic market offering significant investment opportunities and strategic importance for the global digital economy.

- Robust Growth Trajectory: The market is set for substantial growth, nearly doubling in value from 2025 to 2033, indicating a strong long-term demand for optical infrastructure.

- Foundation for Digital Economy: Optical communication is an essential backbone for the global digital economy, supporting 5G, cloud, AI, and IoT, ensuring continued relevance and investment.

- Bandwidth Demand as Primary Driver: The ever-increasing need for higher bandwidth and lower latency across all sectors is the core catalyst for market expansion.

- Technological Innovation is Key: Continuous advancements in coherent technology, network disaggregation, and photonics integration are critical for sustaining growth and addressing evolving challenges.

- Significant Investment Opportunities: The market presents lucrative opportunities for equipment manufacturers, service providers, and technology investors due to ongoing infrastructure upgrades and new deployments.

- Regional Growth Disparities: While global growth is strong, specific regions like Asia Pacific and North America are expected to lead in market expansion due to extensive 5G rollout and data center investments.

Optical Communication and Networking Equipment Market Drivers Analysis

The Optical Communication and Networking Equipment Market is significantly propelled by several key factors that underpin the global digital transformation. The exponential growth in data traffic, fueled by widespread internet usage, streaming services, and data-intensive applications, creates an urgent need for higher bandwidth and more efficient communication infrastructures. This surge in data necessitates the continuous upgrade and expansion of optical networks, which are inherently capable of transmitting vast amounts of information at light speed. Furthermore, the global deployment of 5G networks is a monumental driver, as 5G requires dense fiber optic backhaul and fronthaul to support its low-latency and high-throughput capabilities, pushing demand for advanced optical equipment.

The proliferation of cloud computing and the rapid expansion of hyperscale data centers are also paramount drivers. As businesses and individuals increasingly rely on cloud-based services for storage, processing, and application delivery, the need for robust, high-capacity optical interconnects between and within data centers becomes critical. Additionally, the growing adoption of the Internet of Things (IoT) devices generates massive data volumes, further stressing existing networks and driving the imperative for more scalable optical solutions. Government initiatives and investments in digital infrastructure, particularly in developing regions, also play a crucial role in accelerating market growth by funding fiber optic deployments and enhancing network connectivity.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Exponential Growth in Data Traffic | +2.5% | Global, particularly North America, Asia Pacific | Long-term (2025-2033) |

| Global 5G Network Deployments | +2.0% | Asia Pacific (China, South Korea, Japan), North America (US), Europe | Medium-term (2025-2030) |

| Rapid Expansion of Hyperscale Data Centers & Cloud Computing | +1.8% | Global, especially US, Ireland, Singapore, India | Long-term (2025-2033) |

| Increased Adoption of IoT and Connected Devices | +1.2% | Global | Medium-term to Long-term (2025-2033) |

| Government Initiatives and Investments in Digital Infrastructure | +1.0% | Emerging Economies (India, Brazil, African nations), Rural Areas | Long-term (2025-2033) |

Optical Communication and Networking Equipment Market Restraints Analysis

Despite the strong growth drivers, the Optical Communication and Networking Equipment Market faces several significant restraints that could temper its expansion. One of the primary inhibitors is the high initial capital expenditure required for deploying and upgrading optical network infrastructure. The cost of advanced optical fibers, transceivers, and networking equipment, coupled with the expenses associated with installation, right-of-way acquisition, and civil works, can be prohibitive for smaller service providers or developing regions. This substantial upfront investment often leads to longer payback periods, potentially deterring rapid network expansion.

Furthermore, the global supply chain disruptions, exacerbated by geopolitical tensions and unforeseen events, pose a constant challenge. Shortages of critical components, such as semiconductors and specialized optical materials, can delay manufacturing and deployment schedules, affecting market growth. Additionally, the industry requires a highly skilled workforce for the design, installation, and maintenance of complex optical networks. A persistent shortage of qualified engineers and technicians can hinder deployment timelines and increase operational costs. Lastly, the significant power consumption of high-capacity optical networking equipment, particularly in data centers, presents an environmental and economic challenge, pushing operators to seek more energy-efficient solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -1.5% | Global, particularly developing nations | Long-term (2025-2033) |

| Supply Chain Disruptions and Component Shortages | -1.0% | Global, especially regions reliant on specific manufacturing hubs (Asia) | Short-term to Medium-term (2025-2028) |

| Shortage of Skilled Workforce | -0.8% | Global, particularly developed regions with aging workforce | Long-term (2025-2033) |

| High Power Consumption of Network Equipment | -0.7% | Global, especially data centers and energy-conscious regions (Europe) | Medium-term to Long-term (2025-2033) |

Optical Communication and Networking Equipment Market Opportunities Analysis

The Optical Communication and Networking Equipment Market is ripe with opportunities stemming from emerging technological advancements and unmet connectivity needs. The ongoing expansion of rural broadband connectivity globally presents a significant opportunity. Many remote and underserved areas still lack high-speed internet access, creating a substantial demand for new fiber optic deployments and associated networking equipment. Governments and private enterprises are increasingly focusing on bridging this digital divide, driving investments in fiber-to-the-home (FTTH) and other last-mile optical solutions, thereby opening new market segments and revenue streams for equipment providers.

Another major opportunity lies in the continuous innovation within disaggregated and open optical networks. This paradigm shift, separating hardware from software and allowing multi-vendor interoperability, fosters greater flexibility, accelerates innovation cycles, and reduces total cost of ownership for network operators. This trend is creating new niches for specialized software vendors, system integrators, and component manufacturers who can offer modular and interoperable solutions. Furthermore, the burgeoning fields of virtual reality (VR), augmented reality (AR), and the metaverse, which demand ultra-low latency and immense bandwidth, are creating new use cases and driving the need for more advanced and high-capacity optical communication equipment, pushing the boundaries of current network capabilities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Rural Broadband Connectivity | +1.8% | Emerging Economies, Rural US, Europe, Australia | Long-term (2025-2033) |

| Development of Disaggregated and Open Optical Networks | +1.5% | Global, particularly Tier 1 service providers and hyperscalers | Medium-term to Long-term (2025-2033) |

| Emergence of New Applications (e.g., VR/AR, Metaverse) | +1.2% | Global, concentrated in technologically advanced regions | Long-term (2028-2033) |

| Advancements in Quantum Networking and Secure Communication | +0.8% | Research-focused nations (US, China, Europe) | Long-term (2030-2033) |

Optical Communication and Networking Equipment Market Challenges Impact Analysis

The Optical Communication and Networking Equipment Market encounters several complex challenges that demand continuous innovation and strategic responses. One significant hurdle is managing the escalating power consumption of networking equipment, particularly with the rise of high-capacity data centers and coherent optical systems. As data traffic grows exponentially, the energy demands of optical networks increase, leading to higher operational costs and environmental concerns. Developing more energy-efficient components and network architectures is crucial to addressing this challenge and ensuring sustainable growth within the industry.

Another key challenge involves ensuring interoperability across diverse vendor equipment and different technological standards. The transition to disaggregated and multi-vendor networks, while offering flexibility, also introduces complexities in ensuring seamless integration and compatibility between various components and software layers. This necessitates robust standardization efforts and collaborative industry initiatives to avoid fragmented ecosystems. Furthermore, the rapid pace of technological obsolescence in the optical domain means that existing infrastructure can quickly become outdated, requiring continuous investment in upgrades and replacements, posing a financial burden for network operators and necessitating careful long-term planning.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Power Consumption of Equipment | -1.0% | Global, especially developed markets with strict environmental regulations | Long-term (2025-2033) |

| Ensuring Interoperability Across Multi-Vendor Systems | -0.9% | Global, particularly for large network operators and hyperscalers | Medium-term (2025-2030) |

| Rapid Technological Obsolescence | -0.7% | Global | Long-term (2025-2033) |

| Evolving Cybersecurity Threats on Optical Layers | -0.5% | Global | Long-term (2025-2033) |

Optical Communication and Networking Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Optical Communication and Networking Equipment Market, covering historical data, current market dynamics, and future projections. The scope encompasses detailed segmentation across various components, technologies, applications, and end-use industries, offering granular insights into market performance and growth opportunities. It further provides a thorough regional analysis, highlighting key market trends and drivers specific to North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, ensuring a global perspective on market dynamics and strategic developments. The report aims to equip stakeholders with actionable intelligence for informed decision-making within this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.45 billion |

| Market Forecast in 2033 | USD 50.88 billion |

| Growth Rate | 8.9% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Cisco Systems, Inc., Ciena Corporation, Huawei Technologies Co., Ltd., Nokia Corporation, Ericsson, Infinera Corporation, Fujitsu Optical Components Limited, ZTE Corporation, Lumentum Holdings Inc., Coherent Corp., Marvell Technology, Inc., Broadcom Inc., NEC Corporation, Sumitomo Electric Industries, Ltd., Corning Incorporated, Prysmian Group, ADVA Optical Networking, ECI Telecom, FiberHome, OptiComm. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Optical Communication and Networking Equipment Market is meticulously segmented across various dimensions to provide a comprehensive understanding of its intricate structure and growth avenues. This segmentation is crucial for identifying specific market niches, understanding demand patterns, and formulating targeted strategies. The market is primarily broken down by component, encompassing the foundational elements that make up optical networks, from the fibers themselves to the complex transceivers and amplifiers that enable data transmission. Each component plays a vital role in network performance and capacity, with ongoing innovation driving advancements in speed, efficiency, and cost-effectiveness.

Further segmentation by technology highlights the diverse transmission methods employed in optical communication, such as Wavelength Division Multiplexing (WDM) and Passive Optical Networks (PON), which cater to different network architectures and bandwidth requirements. Application-based segmentation provides insights into where optical communication equipment is primarily utilized, ranging from large-scale data centers and telecommunication networks to enterprise solutions and last-mile connectivity. Lastly, the market is analyzed by end-use industry, showcasing the adoption of optical communication across sectors like IT, healthcare, and government, underscoring its indispensable role in modern digital infrastructure. This multi-faceted segmentation allows for a detailed assessment of market dynamics and future growth potential across different verticals.

- By Component:

- Fiber Optic Cables: Single-mode, Multi-mode

- Transceivers: SFP, SFP+, QSFP, CFP, OSFP, QSFP-DD

- Optical Amplifiers: EDFA (Erbium-Doped Fiber Amplifier), Raman Amplifier, SOA (Semiconductor Optical Amplifier)

- Optical Switches

- Optical Filters

- Wavelength Division Multiplexers (WDM)

- Connectors and Adapters

- Other Components (e.g., Optical Splitters, Attenuators)

- By Technology:

- Wavelength Division Multiplexing (WDM): DWDM (Dense WDM), CWDM (Coarse WDM)

- Synchronous Optical Networking/Synchronous Digital Hierarchy (SONET/SDH)

- Optical Transport Network (OTN)

- Passive Optical Network (PON): GPON (Gigabit PON), EPON (Ethernet PON), 10G-PON

- Ethernet over Fiber

- Coherent Optical Communication

- By Application:

- Data Center & Cloud Interconnects

- Telecommunication Networks: Long-haul, Metro, Access (FTTx)

- Enterprise Networks

- Fiber-to-the-x (FTTx): FTTH (Fiber-to-the-Home), FTTB (Fiber-to-the-Building), FTTC (Fiber-to-the-Curb)

- Submarine Communications

- Mobile Backhaul/Fronthaul

- By End-Use Industry:

- Telecom & Information Technology (IT)

- BFSI (Banking, Financial Services, and Insurance)

- Healthcare

- Government & Public Sector

- Media & Entertainment

- Education

- Manufacturing & Automation

- Defense & Aerospace

Regional Highlights

- North America: This region is a leading adopter of advanced optical communication technologies, driven by extensive data center growth, early 5G deployments, and significant investments in cloud infrastructure. The presence of major technology companies and a high demand for high-bandwidth applications fuel consistent market expansion, particularly in metro and data center interconnect segments.

- Europe: Characterized by strong government support for digital transformation initiatives and increasing fiber-to-the-home (FTTH) deployments, Europe is witnessing steady growth. Focus on sustainable networking solutions and smart city projects further boosts demand for energy-efficient optical equipment across the region.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, primarily due to massive 5G network rollouts in China, India, Japan, and South Korea, coupled with rapidly expanding internet penetration and data center infrastructure. Government initiatives to enhance digital connectivity in emerging economies within the region are significant growth catalysts.

- Latin America: This region is experiencing a gradual increase in optical communication deployments, driven by expanding broadband penetration and increasing investments in telecommunication infrastructure. Rural connectivity projects and the growing adoption of cloud services are key contributors to market development.

- Middle East and Africa (MEA): The MEA region is emerging as a promising market due to increasing investments in digital infrastructure, particularly in the Gulf Cooperation Council (GCC) countries and parts of Africa. Government-led smart city initiatives, data center construction, and efforts to improve broadband access are stimulating demand for optical networking equipment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Optical Communication and Networking Equipment Market.- Cisco Systems, Inc.

- Ciena Corporation

- Huawei Technologies Co., Ltd.

- Nokia Corporation

- Ericsson

- Infinera Corporation

- Fujitsu Optical Components Limited

- ZTE Corporation

- Lumentum Holdings Inc.

- Coherent Corp.

- Marvell Technology, Inc.

- Broadcom Inc.

- NEC Corporation

- Sumitomo Electric Industries, Ltd.

- Corning Incorporated

- Prysmian Group

- ADVA Optical Networking

- ECI Telecom

- FiberHome

- OptiComm

Frequently Asked Questions

What is optical communication and networking equipment?

Optical communication and networking equipment refers to devices and systems that use light to transmit data over optical fibers. This includes components like fiber optic cables, transceivers, amplifiers, and switches, forming the backbone for high-speed data transmission in telecommunications, data centers, and various other networks.

Why is the Optical Communication and Networking Equipment Market growing?

The market is growing rapidly due to the exponential increase in global data traffic, widespread deployment of 5G networks, expansion of hyperscale data centers, and the rising adoption of cloud computing and IoT. These factors collectively drive an insatiable demand for higher bandwidth and more efficient network infrastructure.

What are the key technologies driving this market?

Key technologies include Wavelength Division Multiplexing (WDM) for increased capacity, coherent optical communication for high-speed long-distance links, Passive Optical Networks (PON) for last-mile connectivity, and advancements in photonics integration, which enables smaller, more efficient optical components.

How does AI impact optical communication networks?

AI significantly impacts optical networks by enabling automated operations, predictive maintenance, intelligent traffic management, and enhanced security. AI-driven solutions optimize network performance, reduce operational costs, and facilitate the development of self-healing and self-optimizing networks.

What are the major challenges facing the market?

Major challenges include the high initial capital expenditure for network deployment, potential supply chain disruptions affecting component availability, the need for a highly skilled workforce, and the increasing power consumption of high-capacity optical networking equipment, which poses both economic and environmental concerns.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted