Geopolymer Market

Geopolymer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702179 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Geopolymer Market Size

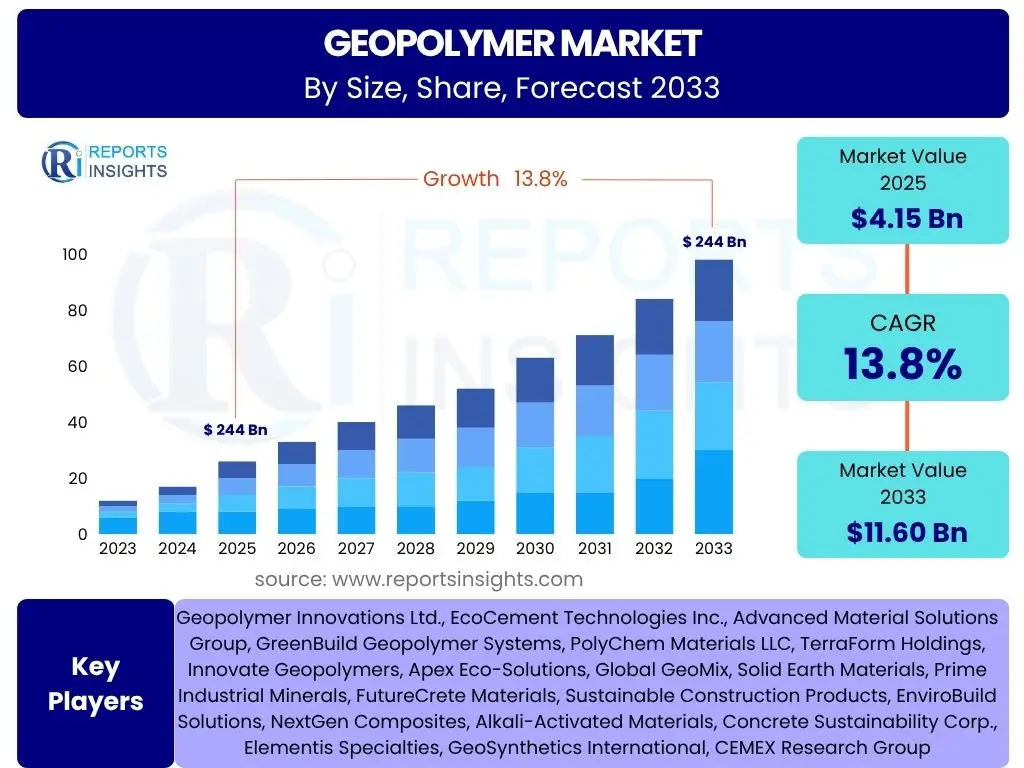

According to Reports Insights Consulting Pvt Ltd, The Geopolymer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.8% between 2025 and 2033. The market is estimated at USD 4.15 billion in 2025 and is projected to reach USD 11.60 billion by the end of the forecast period in 2033.

Key Geopolymer Market Trends & Insights

The Geopolymer market is experiencing significant evolution, driven by a global shift towards sustainable construction and industrial practices. Key user inquiries often revolve around the adoption rates of these eco-friendly materials, their performance benefits compared to traditional counterparts, and their integration into emerging technological fields. There is a strong interest in how geopolymers contribute to circular economy principles and waste valorization, especially concerning industrial by-products. Users frequently seek information on the latest advancements in raw material sourcing, synthesis techniques, and novel applications beyond conventional construction, highlighting a broader industry acceptance and innovation trajectory.

Furthermore, inquiries frequently address the scalability and commercial viability of geopolymer production, alongside the development of standardized practices and regulatory frameworks. The market is witnessing a trend towards specialized geopolymer formulations designed for specific high-performance applications, such as high-temperature resistance and chemical inertness. This indicates a growing recognition of geopolymers not just as a sustainable alternative but as a superior material in certain niche and demanding environments. The convergence of material science with digital technologies, including AI, is also a burgeoning area of interest, promising accelerated material discovery and optimization processes.

- Increasing adoption of sustainable and low-carbon building materials.

- Growing utilization of industrial by-products (fly ash, slag) as raw materials.

- Expansion into specialized applications like refractories, composites, and waste encapsulation.

- Advancements in synthesis methods leading to improved material properties.

- Focus on developing rapid-curing and ambient-curing geopolymer systems.

- Emergence of 3D printing applications for geopolymer-based structures.

- Rising research and development in alkali-activated materials for diverse uses.

- Integration into circular economy models for waste reduction and resource efficiency.

AI Impact Analysis on Geopolymer

Users frequently inquire about the transformative potential of artificial intelligence in accelerating the research, development, and commercialization of geopolymers. Common questions highlight how AI can optimize geopolymer mix designs, predict material properties, and streamline manufacturing processes. There is a significant interest in AI's role in discovering novel raw material sources and developing new geopolymer formulations with enhanced performance characteristics, thereby reducing reliance on traditional, energy-intensive materials. Concerns often include the accessibility of AI tools for smaller enterprises and the need for robust datasets to train effective AI models in this specialized field.

The integration of AI is anticipated to revolutionize the geopolymer sector by enabling more precise control over synthesis parameters, leading to consistent and high-quality material production. AI algorithms can analyze vast experimental data, identify complex relationships between raw material composition and final product performance, and simulate reaction kinetics, significantly cutting down on experimental trials and development timelines. Furthermore, AI can assist in predictive maintenance for geopolymer infrastructure, monitor structural integrity, and provide insights for material lifecycle management. This convergence of material science and advanced analytics is poised to unlock new possibilities for sustainable and high-performance material solutions.

- Accelerated discovery of new geopolymer compositions and raw materials.

- Optimization of mix designs and curing processes for enhanced performance.

- Predictive modeling of material properties and durability.

- Automated quality control and real-time process monitoring in manufacturing.

- Reduced development time and costs for novel geopolymer products.

- Enhanced understanding of complex reaction mechanisms.

- Facilitation of sustainable material design and resource efficiency.

- Potential for smart geopolymer structures with embedded sensors and AI analytics.

Key Takeaways Geopolymer Market Size & Forecast

The Geopolymer market is poised for robust growth, driven primarily by increasing environmental awareness, stringent regulations on carbon emissions, and the growing demand for sustainable construction materials. Key user questions frequently center on the underlying drivers of this growth, the specific applications demonstrating the most potential, and the overall trajectory of market expansion. The consistent double-digit CAGR projected through 2033 signifies a fundamental shift in material preferences across various industries, indicating that geopolymers are transitioning from a niche solution to a mainstream alternative in many applications. This growth is also underpinned by advancements in material science, making geopolymers more accessible and versatile.

Insights from the market forecast reveal that the construction and infrastructure sectors will remain the largest consumers, but significant growth is also anticipated in specialized segments like refractories, waste management, and even advanced manufacturing. The escalating market value by the end of the forecast period underscores the increasing investment in research and development, capacity expansion, and the broader acceptance of geopolymer technology globally. User queries often highlight the importance of cost-effectiveness, scalability, and long-term durability as crucial factors influencing this market adoption. The market’s expansion is a clear indicator of its potential to address critical environmental and economic challenges facing industries worldwide.

- Substantial market expansion driven by sustainability mandates and green building initiatives.

- Consistent double-digit Compound Annual Growth Rate (CAGR) reflecting strong market adoption.

- Significant value increase projected from 2025 to 2033, demonstrating market maturity.

- Construction and infrastructure sectors remain primary growth engines, alongside specialized applications.

- Growing acceptance of geopolymers as viable alternatives to traditional cement and concrete.

- Increased focus on utilizing industrial waste for raw material sourcing, promoting circular economy.

Geopolymer Market Drivers Analysis

The global shift towards sustainable development and circular economy principles is a primary driver for the Geopolymer market. Industries are increasingly seeking alternatives to traditional materials like Portland cement, which has a significant carbon footprint. Geopolymers offer a compelling solution due to their ability to utilize industrial by-products such as fly ash, blast furnace slag, and other waste materials, thereby reducing landfill waste and conserving natural resources. This environmental benefit, coupled with the potential for lower embodied energy in production, aligns perfectly with global climate goals and corporate sustainability initiatives.

Beyond environmental advantages, geopolymers possess superior performance characteristics that are increasingly recognized across various applications. These include high early strength, excellent fire resistance, improved chemical resistance, and enhanced durability in harsh environments. Such properties make them highly attractive for critical infrastructure projects, waste encapsulation, and high-temperature applications where traditional materials fall short. Furthermore, evolving regulatory frameworks and government incentives aimed at promoting green construction and waste valorization are creating a favorable policy environment, further accelerating the adoption of geopolymer technology in both developed and developing economies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for sustainable building materials | +3.5% | Global, particularly Europe, Asia Pacific | Short to Long Term (2025-2033) |

| Increased utilization of industrial waste as raw materials | +2.8% | Asia Pacific (China, India), North America, Europe | Short to Medium Term (2025-2029) |

| Superior performance properties (fire/chemical resistance) | +2.0% | Global, specialized industries | Medium to Long Term (2027-2033) |

| Stringent environmental regulations & carbon emission targets | +1.5% | Europe, North America, Japan | Short to Medium Term (2025-2030) |

| Cost-effectiveness in certain applications | +1.2% | Developing economies, competitive markets | Medium to Long Term (2027-2033) |

Geopolymer Market Restraints Analysis

Despite the promising outlook, the Geopolymer market faces several significant restraints that could impede its growth. One primary challenge is the limited awareness and understanding of geopolymer technology among architects, engineers, and construction professionals. Traditional building practices are deeply entrenched, and there is often skepticism regarding the long-term performance and reliability of novel materials. This lack of familiarity necessitates extensive education and demonstration projects to build confidence and overcome industry inertia, which can be a slow and resource-intensive process.

Another crucial restraint is the lack of standardized design codes, material specifications, and regulatory frameworks specifically for geopolymers. Unlike Portland cement concrete, which has well-established standards globally, geopolymers currently rely on project-specific approvals, hindering widespread adoption and large-scale manufacturing. This absence of clear guidelines creates uncertainty for manufacturers and users, affecting quality control, product consistency, and market scalability. Furthermore, the variability in the chemical composition of industrial by-products used as raw materials can lead to inconsistencies in geopolymer performance, posing challenges for quality assurance and broad application, particularly in regions with diverse industrial outputs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of standardized codes and specifications | -2.0% | Global | Short to Medium Term (2025-2030) |

| Limited awareness and skepticism among end-users | -1.5% | Developing economies, conservative markets | Short to Medium Term (2025-2029) |

| Variability in raw material quality and supply | -1.0% | Regional dependent (e.g., coal-fired power plant locations) | Short to Long Term (2025-2033) |

| Higher initial material and production costs in some cases | -0.8% | Developing economies, cost-sensitive projects | Short to Medium Term (2025-2028) |

| Longer curing times for certain applications | -0.5% | Fast-paced construction environments | Short Term (2025-2027) |

Geopolymer Market Opportunities Analysis

The Geopolymer market is ripe with opportunities, particularly in the expansion of its application spectrum beyond conventional construction. Emerging fields such as 3D printing of construction materials, advanced composites for aerospace and automotive industries, and specialized applications in waste management for encapsulating hazardous materials present significant avenues for growth. The unique properties of geopolymers, such as their rapid setting times, high strength-to-weight ratio, and excellent bond strength, make them ideal candidates for these innovative applications. As these technologies mature, geopolymers are positioned to become a material of choice, driving demand and fostering new market segments.

Furthermore, significant opportunities lie in the development of new raw material sources and the optimization of existing ones. Research into alternative industrial wastes, agricultural by-products, and naturally occurring aluminosilicate materials is continuously expanding the feedstock options, potentially reducing reliance on specific industrial waste streams and ensuring more localized and sustainable production. Government initiatives and increased funding for green infrastructure projects globally also present a substantial opportunity, as these programs often prioritize innovative and environmentally friendly materials. Collaborations between academic institutions, industry players, and governmental bodies can accelerate R&D, bridge the gap between lab-scale innovation and commercialization, and unlock new market potential through policy support and standardization efforts.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into 3D printing and additive manufacturing | +2.5% | Global | Medium to Long Term (2027-2033) |

| Development of novel raw material sources (e.g., red mud, rice husk ash) | +1.8% | Asia Pacific, Africa, Latin America | Medium to Long Term (2028-2033) |

| Increased government funding for green infrastructure projects | +1.5% | North America, Europe, select APAC countries | Short to Medium Term (2025-2030) |

| Growing demand for high-performance specialty materials | +1.2% | Global, aerospace, automotive, marine sectors | Medium to Long Term (2027-2033) |

| Emergence of self-healing and smart geopolymer composites | +0.8% | Developed economies, R&D focused regions | Long Term (2030-2033) |

Geopolymer Market Challenges Impact Analysis

The Geopolymer market faces significant challenges, particularly concerning scaling up production to meet large-scale industrial demand. While laboratory and pilot-scale successes are numerous, transitioning to commercial mass production requires substantial capital investment, robust supply chain management for diverse raw materials, and consistent quality control processes. The inherent variability of industrial by-products, which form the base of many geopolymers, complicates standardization and can lead to batch-to-batch inconsistencies, posing a significant hurdle for manufacturers aiming for uniform product quality and performance across different regions and applications.

Another critical challenge is overcoming the ingrained skepticism and resistance to change within the well-established construction and manufacturing industries. Decision-makers often prioritize proven technologies and may be hesitant to adopt new materials without extensive long-term performance data, certifications, and strong regulatory backing. This necessitates considerable investment in educating the market, conducting long-term field studies, and demonstrating life-cycle cost benefits. Furthermore, the development of a skilled workforce familiar with geopolymer formulation, mixing, and application techniques is essential but currently lacking, posing a constraint on rapid adoption and efficient project execution. Addressing these multifaceted challenges will be crucial for the geopolymer market to realize its full potential and achieve widespread integration.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scaling up production for commercial viability | -1.8% | Global | Short to Medium Term (2025-2030) |

| Lack of standardized testing methods and certifications | -1.5% | Global | Short to Medium Term (2025-2029) |

| Competition from established traditional materials (e.g., Portland cement) | -1.2% | Global | Short to Long Term (2025-2033) |

| High initial investment for manufacturing facilities | -0.9% | Developing economies, new entrants | Short to Medium Term (2025-2028) |

| Limited availability of specialized expertise and skilled labor | -0.6% | Global | Short to Medium Term (2025-2030) |

Geopolymer Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Geopolymer market, examining its current landscape, future projections, and the underlying dynamics shaping its growth. It covers market size estimations, growth rate forecasts, and a detailed segmentation analysis across various types, applications, and end-use industries. The report also highlights key market trends, identifies major drivers, restraints, opportunities, and challenges, and assesses the competitive landscape by profiling leading market players. Furthermore, it offers regional insights, pinpointing growth opportunities and market specifics across key geographical segments to provide a holistic understanding of the global geopolymer ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.15 billion |

| Market Forecast in 2033 | USD 11.60 billion |

| Growth Rate | 13.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Geopolymer Innovations Ltd., EcoCement Technologies Inc., Advanced Material Solutions Group, GreenBuild Geopolymer Systems, PolyChem Materials LLC, TerraForm Holdings, Innovate Geopolymers, Apex Eco-Solutions, Global GeoMix, Solid Earth Materials, Prime Industrial Minerals, FutureCrete Materials, Sustainable Construction Products, EnviroBuild Solutions, NextGen Composites, Alkali-Activated Materials, Concrete Sustainability Corp., Elementis Specialties, GeoSynthetics International, CEMEX Research Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Geopolymer market is segmented across various dimensions, including type, application, and end-use industry, reflecting the diverse nature and growing adoption of these sustainable materials. Each segment plays a crucial role in the overall market dynamics, with distinct growth drivers and regional specificities. Understanding these segmentations is vital for stakeholders to identify key growth pockets and tailor their strategies to specific market needs. The market’s expansion is particularly notable in areas where geopolymers offer unique performance advantages or align with stringent environmental regulations.

The segmentation by type primarily categorizes geopolymers based on their precursor materials, such as fly ash, slag, and metakaolin. The prevalence of certain industrial by-products in different regions significantly influences the dominant type. Application-wise, the market sees extensive use in cement and concrete, precast products, and infrastructure, but also increasingly in specialized areas like refractories and waste management due to geopolymers' superior chemical and thermal resistance. End-use industries range from traditional building and construction to advanced sectors like automotive, aerospace, and industrial manufacturing, showcasing the material's versatility and potential for further market penetration.

- By Type:

- Fly Ash-based Geopolymer: Dominant segment due to abundant availability of fly ash from coal-fired power plants. Offers excellent mechanical properties and cost-effectiveness.

- Slag-based Geopolymer: Utilizes ground granulated blast-furnace slag, known for high strength development and durability, particularly in harsh environments.

- Metakaolin-based Geopolymer: Valued for its purity and consistent performance, often used in higher-value applications where specific properties are required.

- Others: Includes geopolymers made from red mud, rice husk ash, volcanic ash, and other aluminosilicate sources, catering to regional raw material availability and specific niche applications.

- By Application:

- Cement & Concrete: Largest application, driven by demand for green building materials and reduced carbon footprint.

- Precast Products: Favored for faster curing and high early strength, enabling efficient manufacturing of precast elements.

- Infrastructure (Roads, Bridges): Utilized for durable and resilient structures, especially in corrosive or high-temperature environments.

- Refractories: High-temperature resistance makes geopolymers ideal for furnace linings and other refractory applications.

- Waste Management (Stabilization & Solidification): Effective in immobilizing hazardous waste and heavy metals, offering environmental benefits.

- Ceramics: Used for producing durable and heat-resistant ceramic-like materials.

- Adhesives & Binders: Employed for their strong bonding properties in various industrial contexts.

- Others: Encompasses applications in composites, coatings, fire-resistant panels, and architectural elements.

- By End-Use Industry:

- Building & Construction: Core industry segment, driven by residential, commercial, and industrial construction projects.

- Industrial (e.g., Energy, Mining, Chemical): Uses geopolymers for specific industrial processes requiring chemical or thermal resistance.

- Waste Management: Growing segment due to increasing focus on environmental remediation and safe disposal of industrial by-products.

- Transportation: Includes applications in roads, railway sleepers, and tunnels, emphasizing durability and low maintenance.

- Arts & Heritage Restoration: Utilized for their aesthetic compatibility and durability in restoring historical structures.

- Automotive & Aerospace: Emerging segment for lightweight and high-strength components.

- Research & Development: Continuous innovation driving new applications and material advancements.

Regional Highlights

- North America: The region demonstrates significant growth in the Geopolymer market, primarily driven by increasing environmental regulations, growing demand for sustainable construction, and a strong emphasis on infrastructure development. The United States and Canada are leading the adoption, spurred by R&D investments and initiatives to utilize industrial waste. Innovation in high-performance applications and 3D printing also contributes to regional growth.

- Europe: Europe is at the forefront of geopolymer adoption due to stringent carbon emission targets, robust green building codes, and a circular economy focus. Countries like Germany, France, and the UK are actively investing in geopolymer research and commercialization. The region benefits from a well-developed industrial base for raw material sourcing and a strong regulatory push towards eco-friendly materials in construction and waste management.

- Asia Pacific (APAC): The APAC region represents the largest and fastest-growing market for geopolymers, fueled by rapid urbanization, massive infrastructure projects, and abundant availability of industrial by-products like fly ash and slag. China and India are major contributors, driven by the sheer scale of their construction activities and increasing environmental awareness. Japan, South Korea, and Australia are also making strides in advanced geopolymer applications and research.

- Latin America: This region is experiencing nascent but promising growth in the geopolymer market, driven by increasing awareness of sustainable construction and the need for durable infrastructure. Countries like Brazil and Mexico are exploring geopolymer technology for various applications, especially in areas with significant industrial waste generation. Economic development and a focus on cost-effective, environmentally sound solutions are key drivers.

- Middle East and Africa (MEA): The MEA region is witnessing emerging interest in geopolymers, particularly in the construction sector where extreme environmental conditions demand high-performance materials. Investments in infrastructure development and efforts to diversify economies away from fossil fuels are fostering the adoption of sustainable alternatives. Waste management and the utilization of local industrial by-products present significant opportunities in countries like UAE, Saudi Arabia, and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Geopolymer Market.- Geopolymer Technologies Inc.

- GreenCement Innovations

- Advanced Materials Solutions Corp.

- EcoBuild Systems

- Polymeric Geoconsultants

- TerraCycle Materials

- Innovate Earth Solutions

- Global Sustainable Products

- Solid State Composites

- Prime Eco-Materials

- Future Earth Technologies

- Sustainable Infrastructure Group

- EnviroChem Materials

- NextGen Construction Solutions

- Alkali-Activated Composites

- Concrete Innovations Ltd.

- Geosynthetics Advanced Materials

- Industrial Waste Conversion Co.

- Urban Green Builders

- Material Science Global

Frequently Asked Questions

What is a geopolymer and how does it differ from traditional cement?

A geopolymer is an inorganic polymer formed from the reaction of aluminosilicate-rich source materials (like fly ash or slag) with an alkaline activator solution. Unlike traditional Portland cement, which relies on calcination at high temperatures and produces significant CO2 emissions, geopolymers are synthesized at ambient or slightly elevated temperatures, resulting in a much lower carbon footprint and enhanced material properties such such as superior fire resistance, chemical resistance, and durability.

What are the primary applications of geopolymers?

Geopolymers are primarily used in the building and construction industry as an eco-friendly alternative to conventional concrete and cement, particularly for precast products, roads, and bridges. Their unique properties also make them suitable for specialized applications, including refractories (high-temperature furnace linings), waste encapsulation and solidification, fire-resistant coatings, and even emerging fields like 3D printing of construction components and advanced composites.

What are the environmental benefits of using geopolymers?

The key environmental benefits of geopolymers include a significantly reduced carbon footprint compared to Portland cement (up to 80% less CO2 emissions), the effective utilization and valorization of industrial waste by-products (e.g., fly ash, blast furnace slag), reduced energy consumption during production, and the potential for lower embodied energy in structures. Their durability also contributes to longer service life and reduced need for repairs, further minimizing environmental impact.

What are the main challenges hindering the widespread adoption of geopolymers?

The primary challenges for widespread geopolymer adoption include the lack of standardized design codes and specifications, which creates uncertainty for large-scale projects; limited awareness and skepticism among conventional construction professionals; variability in the quality and availability of precursor industrial waste materials; and the need for specific expertise in mix design and application. Overcoming these requires sustained research, education, and regulatory support.

What is the future outlook for the geopolymer market?

The future outlook for the geopolymer market is highly promising, projected for robust double-digit growth driven by increasing global demand for sustainable construction materials, stringent environmental regulations, and ongoing advancements in material science. Expansion into new applications, coupled with increasing investments in research and development and the potential for AI-driven optimization, will further accelerate market penetration and contribute to its significant growth by 2033.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted