Gemcitabine HCl Market

Gemcitabine HCl Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700859 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

Gemcitabine HCl Market Size

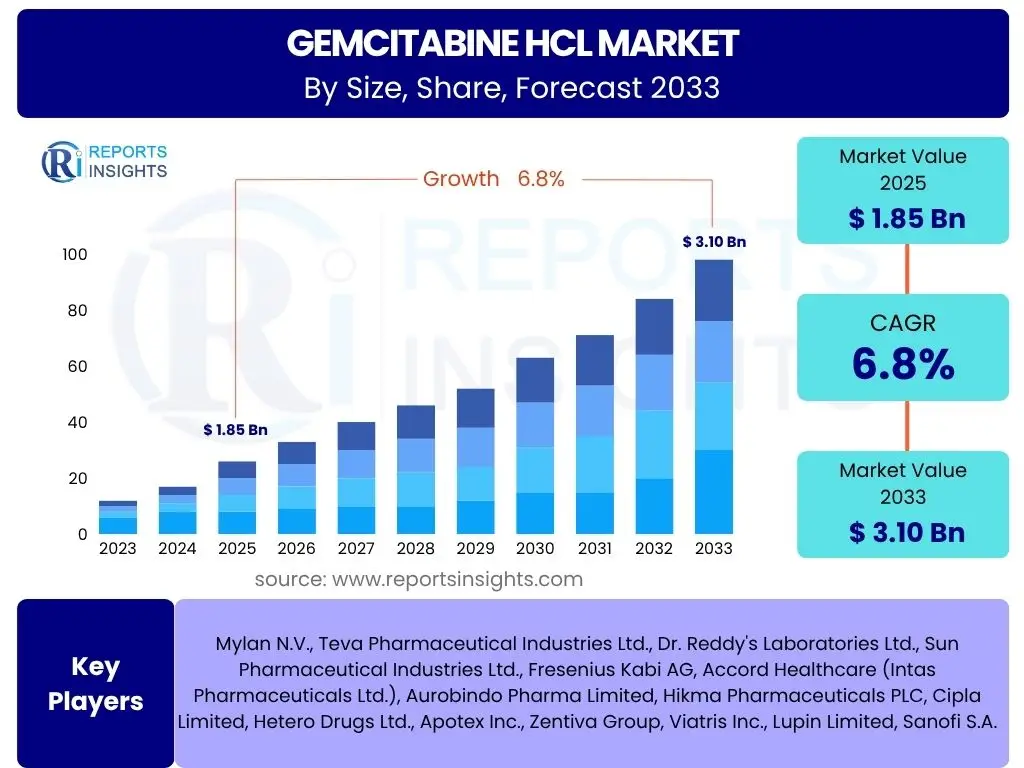

According to Reports Insights Consulting Pvt Ltd, The Gemcitabine HCl Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.85 billion in 2025 and is projected to reach USD 3.10 billion by the end of the forecast period in 2033.

Key Gemcitabine HCl Market Trends & Insights

The Gemcitabine HCl market is currently experiencing a dynamic shift driven by several converging factors. A significant trend is the increasing adoption of combination therapies, where Gemcitabine HCl is used alongside other chemotherapeutic agents or targeted therapies to enhance efficacy and overcome drug resistance in various cancer types. This approach not only broadens its applicability but also seeks to improve patient outcomes by targeting multiple pathways involved in cancer progression.

Another prominent trend involves advancements in drug delivery systems, aiming to improve the pharmacokinetic profile of Gemcitabine HCl, reduce systemic toxicity, and enhance drug concentration at tumor sites. Innovations such as liposomal formulations, nanoparticles, and sustained-release implants are under development, promising better therapeutic indices. Furthermore, the market is witnessing a rise in research and development activities focused on exploring new indications for Gemcitabine HCl beyond its traditional uses, as well as strategies to mitigate common side effects and improve patient compliance.

The increasing prevalence of various cancers globally, particularly pancreatic, lung, and bladder cancers where Gemcitabine HCl is a cornerstone treatment, continues to underpin market growth. Generic penetration, while posing pricing challenges, also contributes to wider accessibility and affordability, especially in developing regions. Telemedicine and digital health platforms are also indirectly influencing market dynamics by improving patient monitoring and adherence to treatment regimens, thereby supporting the continued use of established therapies like Gemcitabine HCl.

- Increasing prevalence of pancreatic, non-small cell lung, bladder, and breast cancers.

- Growing adoption of Gemcitabine HCl in combination therapies for enhanced efficacy.

- Advancements in novel drug delivery systems to improve therapeutic index.

- Expansion of generic formulations improving drug accessibility and affordability.

- Rising research and development efforts for new indications and reduced toxicity.

- Integration of personalized medicine approaches to optimize treatment protocols.

AI Impact Analysis on Gemcitabine HCl

Artificial intelligence (AI) is poised to significantly transform various facets of the Gemcitabine HCl market, primarily by accelerating drug discovery, optimizing clinical trials, and enhancing personalized treatment strategies. Users frequently inquire about how AI can identify novel biomarkers for Gemcitabine HCl responsiveness, predict patient outcomes more accurately, or even potentially redesign its molecular structure for improved efficacy and reduced toxicity. AI-driven predictive analytics can analyze vast datasets of patient genomic and proteomic information, helping clinicians determine which patients are most likely to respond favorably to Gemcitabine HCl, thereby minimizing ineffective treatments and reducing healthcare costs.

Furthermore, AI algorithms are being leveraged to streamline the drug development pipeline, from identifying potential drug synergies for combination therapies involving Gemcitabine HCl to automating preclinical data analysis, which can drastically cut down the time and cost associated with bringing new therapeutic regimens to market. In clinical trials, AI can assist in patient recruitment, monitor adverse events more efficiently, and analyze complex trial data to extract meaningful insights, leading to faster approvals and broader availability of optimized Gemcitabine HCl-based treatments. The integration of AI tools could lead to more precise dosing recommendations, improving the therapeutic window and patient quality of life.

Despite the immense potential, common user concerns also revolve around data privacy, the validation of AI models in clinical settings, and the ethical implications of AI-driven treatment decisions. There is a strong expectation that AI will help address the challenge of drug resistance, particularly in pancreatic cancer, by identifying novel targets or combination strategies that can circumvent resistance mechanisms. Overall, AI is seen as a powerful tool to augment human capabilities in oncology, leading to more efficient, precise, and personalized Gemcitabine HCl therapies.

- Accelerated drug discovery and repurposing of Gemcitabine HCl.

- Optimization of clinical trial design and patient stratification for Gemcitabine HCl.

- Enhanced personalized medicine, predicting patient response and tailoring dosages.

- Improved identification of biomarkers for Gemcitabine HCl efficacy and toxicity.

- Development of AI-driven predictive models for disease progression and treatment outcomes.

- Streamlined data analysis from research to real-world evidence for Gemcitabine HCl use.

- Potential for AI to identify novel combination therapies involving Gemcitabine HCl.

Key Takeaways Gemcitabine HCl Market Size & Forecast

The Gemcitabine HCl market is poised for steady growth through 2033, driven predominantly by the persistent global burden of cancer, particularly types responsive to this chemotherapy. Key takeaways from the market size and forecast analysis highlight a stable demand base, underpinned by its established efficacy as a first-line or adjunct treatment in multiple solid tumors. Stakeholders are keen to understand the balance between the increasing generic availability and the potential for new indications or improved formulations to sustain market value. The market's resilience is also attributed to its cost-effectiveness compared to some newer, more expensive therapies, ensuring its continued relevance in global healthcare systems.

A critical insight is the anticipated shift towards combination therapies and the integration of Gemcitabine HCl into more comprehensive treatment protocols, which is expected to be a primary growth propeller. Users are often concerned with how long the drug's patent life or market exclusivity will last for innovators and how generic competition will shape future pricing and access. While generic erosion might impact revenue for original manufacturers, it simultaneously expands the patient pool benefiting from the treatment globally, particularly in emerging markets. The forecast emphasizes that despite competition from novel agents, Gemcitabine HCl will retain its foundational role in oncology due to its proven track record and adaptability within evolving therapeutic landscapes.

Ultimately, the market forecast underscores the necessity for continuous innovation in drug delivery and combination strategies to maintain competitive edge and address unmet medical needs. The market is not merely growing in volume but also evolving in how Gemcitabine HCl is utilized, reflecting broader trends in precision oncology and patient-centric care. Investment in research that reduces side effects or improves patient compliance for long-term treatment is also seen as a crucial factor for sustained market viability and positive patient outcomes.

- Stable growth projected at a 6.8% CAGR, reaching USD 3.10 billion by 2033.

- Continued strong demand driven by high global cancer incidence.

- Combination therapy regimens are a significant growth catalyst.

- Generic proliferation expands market access but creates pricing pressure.

- Focus on improved formulations and new indications to enhance market value.

- Cost-effectiveness ensures Gemcitabine HCl remains a vital chemotherapy option.

Gemcitabine HCl Market Drivers Analysis

The increasing global incidence of various cancer types, including pancreatic, non-small cell lung cancer (NSCLC), bladder, and breast cancers, serves as a primary driver for the Gemcitabine HCl market. As these cancer diagnoses rise worldwide, particularly among an aging population, the demand for effective chemotherapeutic agents like Gemcitabine HCl, which is a cornerstone of treatment for these malignancies, naturally escalates. This demographic shift and the rising burden of chronic diseases contribute significantly to the consistent demand for established and efficacious oncology drugs.

Advancements in oncology research and the development of new combination therapies are further propelling market growth. Gemcitabine HCl is frequently used in multi-drug regimens, which have demonstrated improved efficacy and survival rates compared to monotherapy in several cancer indications. The ongoing exploration of synergistic effects with targeted therapies, immunotherapies, and other cytotoxic agents expands its therapeutic utility and reinforces its position as a versatile chemotherapeutic agent within complex treatment protocols. This continuous evolution in treatment paradigms ensures its relevance and continued adoption.

Improved healthcare infrastructure and accessibility to cancer treatments in emerging economies also act as significant drivers. As these regions expand their healthcare capabilities and increase awareness about early cancer diagnosis and treatment, the patient pool receiving chemotherapy, including Gemcitabine HCl, grows. Furthermore, the increasing affordability of generic Gemcitabine HCl formulations, following patent expirations, has made it more accessible to a broader patient population globally, particularly in resource-limited settings, thereby driving volume sales and overall market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Cancer Incidence Globally | +2.1% | Global (North America, Europe, Asia Pacific) | Short to Long Term (2025-2033) |

| Advancements in Combination Therapies | +1.8% | Global (Developed Markets Leading) | Medium to Long Term (2026-2033) |

| Improved Healthcare Infrastructure & Access | +1.5% | Emerging Economies (Asia Pacific, Latin America, MEA) | Medium to Long Term (2027-2033) |

| Aging Global Population | +1.0% | Global | Short to Long Term (2025-2033) |

| Increased Generic Availability & Affordability | +0.8% | Global (Especially Developing Markets) | Short to Medium Term (2025-2029) |

Gemcitabine HCl Market Restraints Analysis

The primary restraint affecting the Gemcitabine HCl market is the patent expiry and subsequent generic erosion, which leads to significant pricing pressure. Once the exclusivity of innovator drugs ends, generic versions flood the market, intensifying competition and driving down prices considerably. This not only impacts the revenue generation of original manufacturers but also influences the overall market value by reducing the average selling price of the drug, despite an increase in volume sales.

Another significant restraint is the severe side effect profile associated with Gemcitabine HCl, common with many traditional chemotherapeutic agents. Patients often experience myelosuppression (low blood cell counts), nausea, vomiting, fatigue, and flu-like symptoms, which can impact treatment adherence and quality of life. The management of these side effects often requires additional medical interventions, increasing the overall cost of treatment and potentially leading to treatment discontinuation in some patients, thus limiting its broader application.

The emergence of novel, targeted therapies and immunotherapies, which often offer more specific mechanisms of action, reduced systemic toxicity, and potentially improved efficacy in certain patient subsets, poses a competitive threat. While Gemcitabine HCl remains a standard, these newer agents can sometimes displace traditional chemotherapy as first-line options or reduce its market share in specific indications, particularly for patients with actionable mutations or those eligible for immunotherapy. This continuous innovation in oncology creates a challenging competitive landscape for established chemotherapies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Patent Expiry & Generic Competition | -1.5% | Global | Short to Medium Term (2025-2029) |

| Associated Side Effects & Toxicity Profile | -1.0% | Global | Long Term (2025-2033) |

| Emergence of Novel Therapies & Modalities | -0.8% | Developed Markets (North America, Europe) | Medium to Long Term (2027-2033) |

| Drug Resistance Development | -0.5% | Global | Medium to Long Term (2028-2033) |

Gemcitabine HCl Market Opportunities Analysis

Significant opportunities exist in exploring new indications and expanding the use of Gemcitabine HCl in less common or refractory cancer types. Research into its efficacy in rare cancers or as a component of salvage therapy for patients who have failed previous treatments could unlock new market segments. Furthermore, investigating its role in neoadjuvant or adjuvant settings for cancers where it is not currently standard practice could significantly broaden its application and patient base, offering pathways for sustained market growth beyond its traditional uses.

The development of novel drug delivery systems presents a substantial opportunity to enhance the therapeutic index of Gemcitabine HCl. Formulations such as liposomal encapsulations, nanoparticles, or albumin-bound versions could improve drug targeting to tumor cells, reduce systemic toxicity, and allow for higher drug concentrations at the site of action. These innovations not only address existing limitations but also potentially improve patient compliance and overall treatment outcomes, thereby revitalizing interest in Gemcitabine HCl and extending its market lifecycle.

Penetrating underserved and emerging markets represents another key opportunity. While generic versions have improved access, there remain vast patient populations in developing regions with increasing cancer incidence but limited access to standard chemotherapy. Strategic partnerships, local manufacturing, and tailored distribution channels can facilitate the wider adoption of Gemcitabine HCl in these high-growth areas. Additionally, research into predictive biomarkers that can identify patients most likely to respond to Gemcitabine HCl offers an opportunity for personalized medicine, optimizing treatment strategies and improving efficacy rates, ultimately boosting its clinical utility and market demand.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| New Indications & Expanded Therapeutic Use | +1.2% | Global | Medium to Long Term (2027-2033) |

| Novel Drug Delivery System Development | +1.0% | Global (Developed Markets Leading R&D) | Long Term (2028-2033) |

| Penetration in Emerging & Underserved Markets | +0.9% | Asia Pacific, Latin America, MEA | Short to Long Term (2025-2033) |

| Personalized Medicine & Biomarker Identification | +0.7% | Developed Markets | Long Term (2029-2033) |

Gemcitabine HCl Market Challenges Impact Analysis

A significant challenge in the Gemcitabine HCl market is the development of drug resistance, particularly in pancreatic cancer and non-small cell lung cancer, over the course of treatment. Cancer cells can develop mechanisms to evade the effects of chemotherapy, leading to disease progression despite continued administration of Gemcitabine HCl. This biological challenge necessitates the development of combination therapies or alternative treatment strategies, limiting the long-term efficacy and market potential of Gemcitabine HCl as a standalone agent.

Stringent regulatory approval processes and complex clinical trial requirements pose considerable hurdles for the introduction of new formulations or expanded indications of Gemcitabine HCl. The high costs and lengthy timelines associated with obtaining regulatory clearances, especially for oncology drugs, can deter investment in further development, thereby slowing down innovation within the market. This regulatory burden can restrict the timely availability of improved therapies or new applications, impacting market growth.

The intense competition from a burgeoning pipeline of novel oncology drugs, including targeted therapies, immunotherapies, and gene therapies, represents a continuous challenge. While Gemcitabine HCl remains a standard, these newer agents often offer advantages such as improved specificity, reduced systemic toxicity, or superior efficacy in certain patient populations. The need to demonstrate continued competitive effectiveness and cost-effectiveness against these innovative treatments is a constant pressure on the Gemcitabine HCl market, requiring ongoing clinical validation and strategic positioning to maintain market share.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Drug Resistance | -1.2% | Global | Medium to Long Term (2027-2033) |

| Stringent Regulatory Approval Processes | -0.9% | Global | Long Term (2028-2033) |

| Competition from Novel Oncology Drugs | -0.7% | Developed Markets | Medium to Long Term (2026-2033) |

| High Cost of R&D for New Formulations | -0.5% | Global | Long Term (2029-2033) |

Gemcitabine HCl Market - Updated Report Scope

This report offers a comprehensive analysis of the global Gemcitabine HCl market, detailing its current size, historical performance, and future growth projections from 2025 to 2033. It encompasses a deep dive into market dynamics, including key drivers, restraints, opportunities, and challenges influencing the industry. The scope also covers a detailed segmentation analysis by various factors such as application, end-user, and distribution channel, alongside a thorough regional assessment to provide a holistic view of the market landscape. Furthermore, the report identifies and profiles key industry players, offering insights into their strategic initiatives and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.10 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mylan N.V., Teva Pharmaceutical Industries Ltd., Dr. Reddy's Laboratories Ltd., Sun Pharmaceutical Industries Ltd., Fresenius Kabi AG, Accord Healthcare (Intas Pharmaceuticals Ltd.), Aurobindo Pharma Limited, Hikma Pharmaceuticals PLC, Cipla Limited, Hetero Drugs Ltd., Apotex Inc., Zentiva Group, Viatris Inc., Lupin Limited, Sanofi S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Gemcitabine HCl market is comprehensively segmented to provide granular insights into its diverse applications, end-users, and distribution channels. This segmentation allows for a detailed understanding of where and how the drug is predominantly utilized, highlighting key growth areas and niche markets. The primary application segments reflect the established efficacy of Gemcitabine HCl across various solid tumors, indicating its broad utility in oncology practice. Each segment is analyzed for its market size, growth trajectory, and contributing factors, offering a complete picture of the market structure.

The end-user segmentation reveals the primary healthcare settings where Gemcitabine HCl is administered, ranging from large hospitals to specialized cancer treatment centers and research institutions. This provides insights into the operational landscape and the preferred channels for drug procurement and administration. Furthermore, the distribution channel analysis clarifies the pathways through which Gemcitabine HCl reaches its end-users, from traditional hospital pharmacies to the expanding role of online pharmacies, reflecting evolving healthcare delivery models and supply chain dynamics. This detailed segmentation is crucial for stakeholders seeking to identify specific market opportunities and tailor their strategies effectively.

- By Application

- Pancreatic Cancer

- Non-Small Cell Lung Cancer (NSCLC)

- Bladder Cancer

- Breast Cancer

- Ovarian Cancer

- Other Applications (e.g., Head and Neck Cancer, Soft Tissue Sarcoma)

- By End User

- Hospitals

- Cancer Treatment Centers

- Specialty Clinics

- Research & Academic Institutions

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Direct Sales

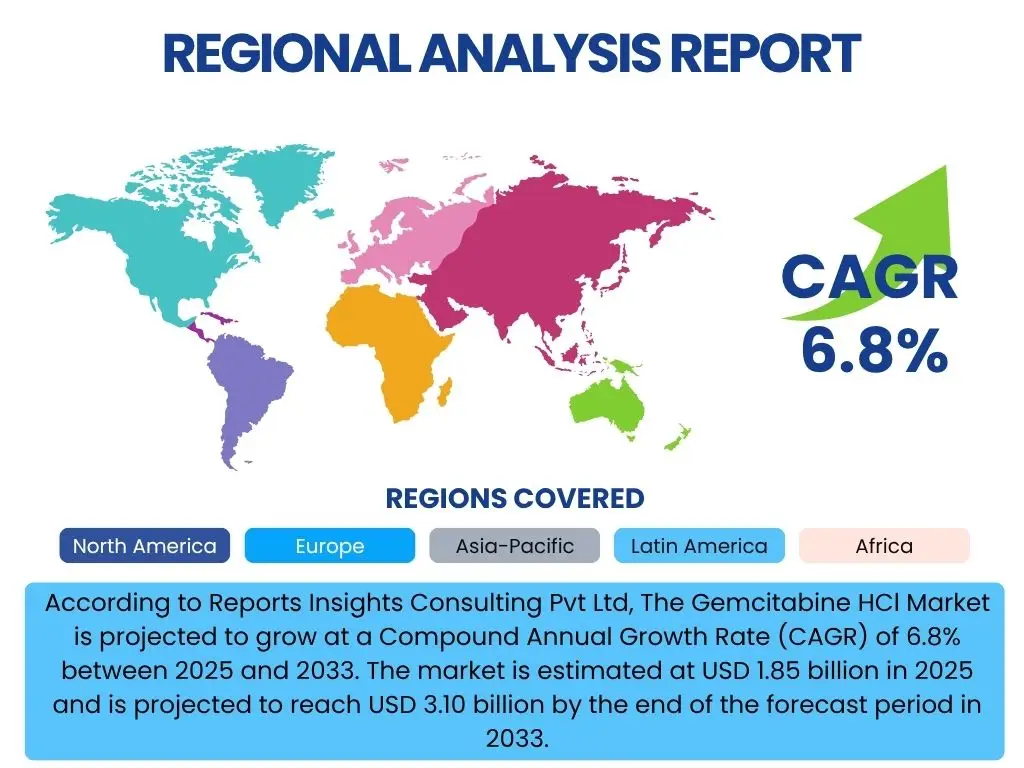

Regional Highlights

The Gemcitabine HCl market exhibits distinct dynamics across various geographical regions, influenced by factors such as cancer incidence rates, healthcare expenditure, regulatory frameworks, and access to advanced medical facilities. North America, particularly the United States, holds a significant market share due to its high prevalence of cancer, advanced healthcare infrastructure, strong R&D activities, and favorable reimbursement policies. The region also benefits from early adoption of novel combination therapies and a high awareness of cancer screening and treatment.

Europe represents another substantial market, driven by its aging population, increasing cancer diagnoses, and well-established healthcare systems. Countries like Germany, France, and the UK contribute significantly to the market, with ongoing clinical research and a growing emphasis on personalized medicine. The market in Europe is also influenced by the presence of major pharmaceutical companies and a strong generic market, ensuring broad access to Gemcitabine HCl.

Asia Pacific is projected to be the fastest-growing region, fueled by its large and rapidly aging population, increasing cancer incidence, improving healthcare infrastructure, and rising healthcare expenditure, particularly in emerging economies like China and India. The growing awareness about cancer, coupled with the increasing affordability and availability of generic Gemcitabine HCl formulations, is expanding the patient pool receiving treatment. Latin America and the Middle East & Africa regions are also expected to witness steady growth, driven by expanding healthcare access, government initiatives to combat cancer, and a rising medical tourism industry. However, these regions often face challenges related to healthcare disparities and limited resources compared to developed markets.

- North America: Dominant market share due to high cancer prevalence, advanced healthcare infrastructure, robust R&D, and favorable reimbursement.

- Europe: Significant market driven by an aging population, established healthcare systems, and increasing adoption of combination therapies.

- Asia Pacific (APAC): Fastest-growing region, propelled by large patient pool, improving healthcare infrastructure, and increasing generic accessibility in countries like China and India.

- Latin America: Steady growth attributed to improving healthcare access, increasing cancer awareness, and growing medical tourism.

- Middle East and Africa (MEA): Emerging market with growth driven by rising healthcare investments and efforts to enhance cancer treatment capabilities, albeit from a lower base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Gemcitabine HCl Market.- Mylan N.V.

- Teva Pharmaceutical Industries Ltd.

- Dr. Reddy's Laboratories Ltd.

- Sun Pharmaceutical Industries Ltd.

- Fresenius Kabi AG

- Accord Healthcare (Intas Pharmaceuticals Ltd.)

- Aurobindo Pharma Limited

- Hikma Pharmaceuticals PLC

- Cipla Limited

- Hetero Drugs Ltd.

- Apotex Inc.

- Zentiva Group

- Viatris Inc.

- Lupin Limited

- Sanofi S.A.

Frequently Asked Questions

Analyze common user questions about the Gemcitabine HCl market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Gemcitabine HCl primarily used for in cancer treatment?

Gemcitabine HCl is a chemotherapy drug primarily used to treat various solid tumors, including pancreatic cancer, non-small cell lung cancer, bladder cancer, and breast cancer. It is often used as a first-line treatment or in combination therapies.

How is the Gemcitabine HCl market projected to grow in the coming years?

The Gemcitabine HCl market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 3.10 billion by 2033, driven by increasing cancer incidence and advancements in combination therapies.

What are the main drivers of growth for the Gemcitabine HCl market?

Key drivers include the rising global incidence of various cancers, the increasing adoption of Gemcitabine HCl in combination therapy regimens, advancements in healthcare infrastructure in emerging economies, and the growing accessibility of generic formulations.

What are the major challenges facing the Gemcitabine HCl market?

Significant challenges include the development of drug resistance, intense competition from newer targeted therapies and immunotherapies, the stringent regulatory approval processes for new formulations, and the associated side effect profile of the drug.

How is AI impacting the development and use of Gemcitabine HCl?

AI is influencing the Gemcitabine HCl market by accelerating drug discovery, optimizing clinical trials, enhancing patient selection for personalized medicine, and identifying novel biomarkers, leading to more efficient and effective therapeutic strategies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted