Formaldehyde Market

Formaldehyde Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702601 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

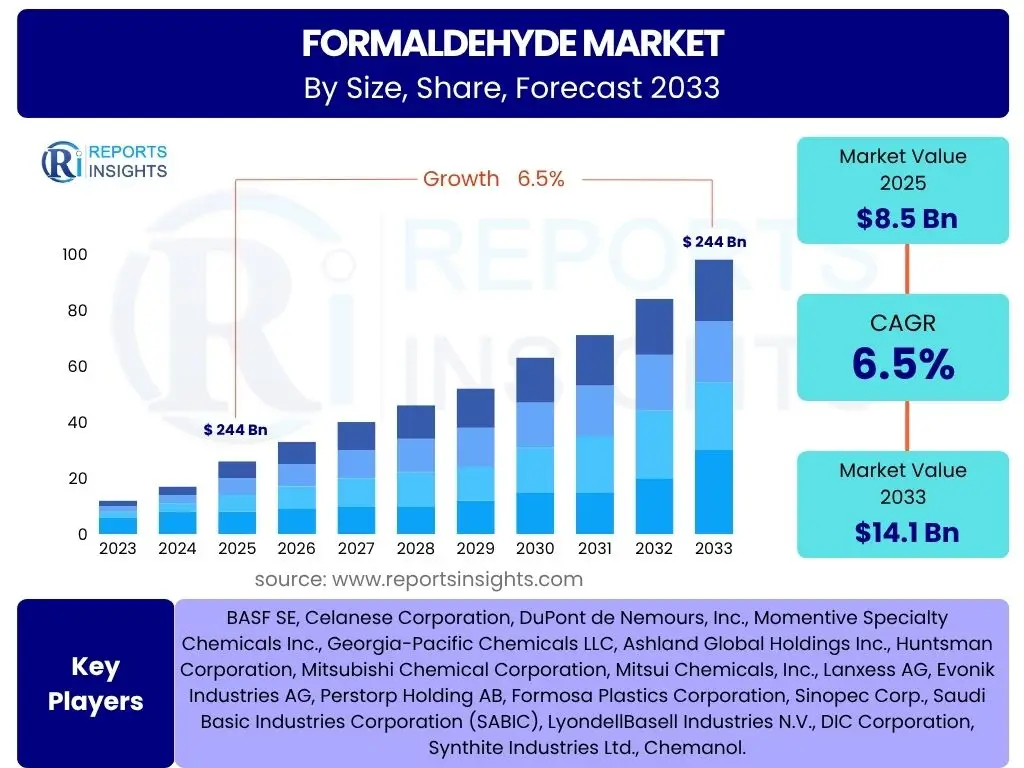

Formaldehyde Market Size

According to Reports Insights Consulting Pvt Ltd, The Formaldehyde Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 14.1 Billion by the end of the forecast period in 2033.

Key Formaldehyde Market Trends & Insights

The Formaldehyde market is undergoing significant transformation, driven by evolving regulatory landscapes, increasing demand from diverse end-use industries, and a growing emphasis on sustainable practices. Key trends indicate a shift towards lower-emission products and innovative applications, reflecting both environmental concerns and the versatile utility of formaldehyde derivatives. Manufacturers are increasingly investing in research and development to address health and safety concerns, leading to the emergence of advanced formulations and production technologies that minimize environmental impact.

Moreover, the market is witnessing robust growth in emerging economies, particularly in Asia Pacific, where industrialization and infrastructure development continue to drive demand for formaldehyde-based resins and chemicals. The construction and automotive sectors remain foundational consumers, while new avenues in specialty chemicals and healthcare are contributing to market diversification. This dynamic interplay of regulatory pressure, technological innovation, and expanding application scope defines the current trajectory of the formaldehyde market.

- Emphasis on developing low-emission and ultra-low-emission formaldehyde (ULEF) products to meet stringent environmental regulations.

- Growing demand for formaldehyde-based resins in the construction and furniture industries, especially for wood composites, laminates, and insulation.

- Increased adoption of formaldehyde derivatives in the automotive sector for lightweight materials and interior components.

- Rise in research and development activities focused on bio-based formaldehyde and sustainable production methods.

- Diversification of applications into specialty chemicals, agricultural products, and even certain medical applications.

- Shift in manufacturing processes towards higher energy efficiency and reduced waste generation.

AI Impact Analysis on Formaldehyde

Artificial Intelligence (AI) is poised to significantly influence the formaldehyde market by optimizing production processes, enhancing safety protocols, and accelerating research into novel applications and sustainable alternatives. Stakeholders are keen to understand how AI can improve operational efficiency, from predictive maintenance of manufacturing equipment to real-time quality control. The integration of AI algorithms can lead to more precise monitoring of reaction conditions, thereby reducing off-spec material production and minimizing waste, directly addressing concerns about cost-efficiency and environmental footprint.

Furthermore, AI and machine learning capabilities offer transformative potential in supply chain management for formaldehyde and its raw materials, enabling predictive analytics for demand forecasting and inventory optimization. This can mitigate the impact of volatile raw material prices and ensure consistent supply. In research and development, AI can rapidly screen molecular structures for new formaldehyde derivatives or identify safer alternatives, accelerating innovation and compliance with evolving regulatory requirements, ultimately driving the industry towards more sustainable and efficient practices.

- Process Optimization: AI-driven predictive analytics for reaction parameters, optimizing yield and reducing energy consumption in formaldehyde production.

- Predictive Maintenance: AI algorithms analyzing sensor data from manufacturing equipment to predict failures, minimizing downtime and maintenance costs.

- Supply Chain Efficiency: AI-powered demand forecasting and logistics optimization to manage raw material procurement and product distribution more effectively.

- Quality Control: AI-enhanced vision systems and analytical tools for real-time quality assurance, ensuring product consistency and reducing defects.

- R&D Acceleration: Machine learning used to accelerate the discovery of new formaldehyde applications or the development of bio-based or low-emission alternatives.

- Safety and Environmental Monitoring: AI for monitoring emissions, detecting leaks, and ensuring worker safety through real-time data analysis and anomaly detection.

Key Takeaways Formaldehyde Market Size & Forecast

The Formaldehyde market is anticipated to exhibit robust growth over the forecast period, driven primarily by sustained demand from established end-use sectors like construction and automotive, alongside the expansion into new, high-value applications. The market's resilience is underpinned by the essential role of formaldehyde derivatives in a wide array of industrial processes and consumer products. Despite regulatory pressures concerning health and environmental impacts, the industry continues to innovate, focusing on product reformulations and process improvements to ensure long-term viability and growth.

Geographically, Asia Pacific is expected to remain the dominant market, propelled by rapid industrialization and urbanization, while mature markets in North America and Europe will focus on premium, low-emission products and sustainable solutions. The projected market expansion underscores the ongoing necessity for formaldehyde as a versatile chemical building block, with market participants strategically investing in technologies that mitigate environmental concerns and enhance product safety, thus ensuring a positive outlook for the coming decade.

- Steady Growth Trajectory: The market is projected for significant expansion at a 6.5% CAGR, indicating stable demand and investment.

- Core Application Resilience: Strong and sustained demand from construction (adhesives, resins) and automotive sectors is a primary growth driver.

- Regional Dominance: Asia Pacific is set to remain the largest and fastest-growing market due to ongoing industrial and urban development.

- Sustainability Focus: Increasing emphasis on low-emission and bio-based formaldehyde products is crucial for regulatory compliance and market acceptance.

- Innovation Imperative: R&D investments in production efficiency, product safety, and alternative chemistries are vital for competitive advantage and market evolution.

Formaldehyde Market Drivers Analysis

The Formaldehyde market's growth is propelled by several key drivers, predominantly the robust demand from the construction and furniture industries. Formaldehyde is a crucial component in the production of various resins, such as urea-formaldehyde (UF), phenol-formaldehyde (PF), and melamine-formaldehyde (MF), which are extensively used in wood-based panels like plywood, particleboard, and medium-density fiberboard (MDF). The global surge in urbanization, infrastructural development, and residential construction activities directly fuels the consumption of these materials, consequently driving the demand for formaldehyde.

Beyond construction, the automotive sector significantly contributes to market expansion. Formaldehyde derivatives are integral to the manufacturing of interior components, coatings, and lightweight materials in vehicles, aligning with the automotive industry's continuous innovation in design and material efficiency. Furthermore, the burgeoning demand for specialized chemicals, including polyacetals and butanediol, where formaldehyde serves as a foundational chemical intermediate, opens up new avenues for market growth. These factors collectively underscore the indispensable role of formaldehyde in various industrial value chains, ensuring its sustained market momentum.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from construction and furniture industries | +2.5% | Asia Pacific (China, India), North America | Short to Medium Term |

| Increasing use in automotive applications for lightweight materials | +1.8% | Europe, Asia Pacific (Japan, South Korea) | Medium Term |

| Expansion of specialty chemicals and derivatives market | +1.5% | Global, particularly emerging economies | Medium to Long Term |

| Urbanization and industrialization trends globally | +1.2% | Asia Pacific, Latin America, Middle East & Africa | Long Term |

| Technological advancements in formaldehyde resin production | +0.5% | Global | Ongoing |

Formaldehyde Market Restraints Analysis

Despite its widespread utility, the Formaldehyde market faces significant restraints, primarily stemming from stringent health and environmental regulations. Formaldehyde is classified as a human carcinogen by several regulatory bodies, leading to increasingly strict limits on its emissions and exposure levels in various products and workplaces. These regulations, particularly in North America and Europe, necessitate substantial investments in low-emission technologies and reformulation efforts by manufacturers, which can increase production costs and potentially limit market expansion in certain applications.

Another major restraint is the volatility in raw material prices, specifically methanol, which is the primary feedstock for formaldehyde production. Fluctuations in crude oil and natural gas prices directly impact methanol costs, leading to unpredictable production expenses for formaldehyde manufacturers. This price instability can squeeze profit margins and create uncertainty in supply chain planning. Furthermore, growing consumer awareness and environmental concerns have driven a demand for "formaldehyde-free" alternatives in various products, posing a competitive challenge to traditional formaldehyde-based solutions and compelling the industry to innovate rapidly towards safer and more sustainable chemistries.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent health and environmental regulations | -2.0% | North America, Europe | Short to Medium Term |

| Volatile raw material (methanol) prices | -1.5% | Global | Ongoing |

| Increasing demand for formaldehyde-free alternatives | -1.0% | North America, Europe, select Asian markets | Medium to Long Term |

| Negative public perception regarding health risks | -0.8% | Global, particularly developed nations | Long Term |

| High capital expenditure for compliance and new technologies | -0.5% | Global | Short to Medium Term |

Formaldehyde Market Opportunities Analysis

The Formaldehyde market presents several significant opportunities, primarily driven by the development and adoption of low-emission and ultra-low-emission formaldehyde (ULEF) technologies. As regulatory landscapes evolve and environmental awareness grows, the demand for products with reduced formaldehyde emissions is creating a niche for manufacturers capable of developing and scaling these advanced formulations. This not only allows compliance with stricter standards but also caters to a growing segment of environmentally conscious consumers and industries, providing a competitive edge and fostering new market segments.

Furthermore, the diversification of applications into niche and high-value sectors offers substantial growth potential. Beyond traditional uses in construction and automotive, formaldehyde derivatives are finding increasing utility in specialty chemicals, advanced materials, and even certain medical and pharmaceutical applications. The expansion into emerging economies, particularly in Asia Pacific, Latin America, and the Middle East & Africa, where infrastructure development and industrialization are accelerating, represents another major opportunity. These regions offer untapped potential for formaldehyde consumption in various end-use industries, as their manufacturing bases continue to expand and modernize.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and adoption of low-emission formaldehyde (LEF) products | +1.8% | North America, Europe, key Asian markets | Short to Medium Term |

| Diversification into new high-value applications (e.g., specialty chemicals, medical) | +1.5% | Global | Medium to Long Term |

| Growth in emerging economies and industrialization projects | +2.0% | Asia Pacific (Southeast Asia), Latin America, MEA | Medium to Long Term |

| Investment in sustainable and bio-based formaldehyde production methods | +0.8% | Global | Long Term |

| Increasing demand for wood-based panels and composites in new construction | +0.4% | Global, especially urbanizing regions | Short Term |

Formaldehyde Market Challenges Impact Analysis

The Formaldehyde market is confronted by several significant challenges, with regulatory compliance remaining a paramount concern. Navigating the complex and often varying international regulations regarding formaldehyde emissions and exposure limits demands continuous monitoring, significant R&D investment for product reformulation, and adaptation of manufacturing processes. Non-compliance can lead to hefty fines, market restrictions, and reputational damage, making it a persistent operational and strategic challenge for market participants. This regulatory burden can disproportionately affect smaller players and impede market entry for new products.

Furthermore, the persistent negative perception and health concerns associated with formaldehyde among consumers and regulatory bodies pose a substantial challenge to market growth. Public apprehension often fuels the demand for "formaldehyde-free" labels, pushing manufacturers to seek alternative, often more expensive or less efficient, chemical solutions. This public sentiment can hinder market acceptance of traditional formaldehyde-based products, even those that comply with current safety standards. Coupled with the inherent technical complexities of producing formaldehyde safely and efficiently, and the need to manage waste effectively, these challenges necessitate constant innovation and proactive engagement from the industry to maintain its market position and ensure sustainable development.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adherence to evolving and stringent environmental regulations | -1.5% | Global, particularly developed markets | Ongoing |

| Managing public perception and health concerns | -1.0% | Global | Long Term |

| High energy consumption and production costs | -0.7% | Global | Ongoing |

| Waste management and safe disposal of by-products | -0.5% | Global | Ongoing |

| Competition from alternative binding agents and resins | -0.3% | North America, Europe | Medium Term |

Formaldehyde Market - Updated Report Scope

This comprehensive report offers an in-depth analysis of the global Formaldehyde market, providing detailed insights into its size, growth trajectory, key trends, drivers, restraints, opportunities, and challenges across various segments and major geographical regions. It encompasses a thorough examination of the market landscape from 2019 to 2033, projecting future growth based on current market dynamics, technological advancements, and evolving regulatory frameworks. The report aims to equip stakeholders with critical data and strategic recommendations to navigate the complexities and capitalize on the opportunities within the formaldehyde industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 14.1 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Celanese Corporation, DuPont de Nemours, Inc., Momentive Specialty Chemicals Inc., Georgia-Pacific Chemicals LLC, Ashland Global Holdings Inc., Huntsman Corporation, Mitsubishi Chemical Corporation, Mitsui Chemicals, Inc., Lanxess AG, Evonik Industries AG, Perstorp Holding AB, Formosa Plastics Corporation, Sinopec Corp., Saudi Basic Industries Corporation (SABIC), LyondellBasell Industries N.V., DIC Corporation, Synthite Industries Ltd., Chemanol. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Formaldehyde market is meticulously segmented to provide a granular understanding of its diverse applications and product types, enabling a comprehensive market analysis. This segmentation allows for the identification of specific growth pockets, demand patterns, and competitive landscapes within various industrial verticals. Understanding these segments is crucial for stakeholders to develop targeted strategies, allocate resources effectively, and capitalize on specific market opportunities.

The segmentation by product type reflects the chemical composition and primary use of formaldehyde derivatives, highlighting the dominance of resin forms. Application-based segmentation provides insight into the functional uses across industries, ranging from adhesives and binders to advanced chemical intermediates. Finally, the end-use industry segmentation categorizes consumption by the final sector, such as construction, automotive, or agriculture, demonstrating the widespread utility and foundational role of formaldehyde in the global economy. Each segment plays a distinct role in the market's overall dynamics and growth trajectory.

- By Product Type:

- Urea-Formaldehyde (UF)

- Phenol-Formaldehyde (PF)

- Melamine-Formaldehyde (MF)

- Polyacetal

- Others (e.g., Pentaerythritol, MDI)

- By Application:

- Resins

- Adhesives

- Binders

- Molding Compounds

- Coatings

- Chemicals

- Polyols

- Butanediol

- Isocyanates

- Other Chemical Intermediates

- Laminates

- Plywood & Particleboard

- Insulation Materials

- Fertilizers

- Others (e.g., Pharmaceuticals, Dyes)

- Resins

- By End-Use Industry:

- Construction

- Automotive

- Furniture & Wood Products

- Consumer Goods

- Agriculture

- Medical & Healthcare

- Others (e.g., Textile, Electrical & Electronics)

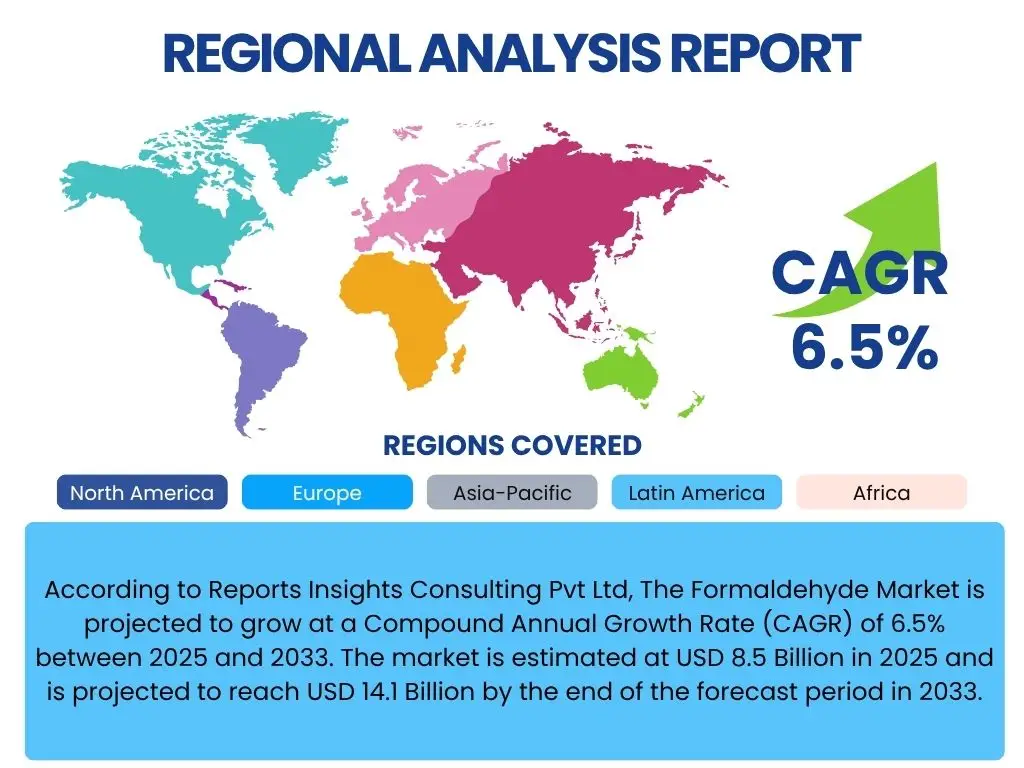

Regional Highlights

Geographical analysis of the Formaldehyde market reveals significant disparities in growth, consumption patterns, and regulatory frameworks across different regions. These regional dynamics are influenced by varying levels of industrialization, infrastructure development, economic growth, and the stringency of environmental regulations. Understanding these regional nuances is essential for market participants to tailor their strategies, optimize supply chains, and identify promising investment opportunities.

Asia Pacific remains the powerhouse of formaldehyde consumption, driven by massive construction projects, expanding automotive manufacturing, and rapid industrial growth in countries like China, India, and Southeast Asian nations. This region’s less stringent environmental regulations compared to developed markets, coupled with a booming population and urbanization, contribute significantly to its market dominance. In contrast, North America and Europe, while mature markets, are characterized by a strong emphasis on sustainability, low-emission product development, and innovation in specialty applications, reflecting their advanced regulatory environments and consumer preferences for eco-friendly solutions. Latin America and the Middle East & Africa are emerging as growth regions, fueled by increasing industrial investments and diversifying economies, though their market sizes are currently smaller compared to APAC.

- Asia Pacific (APAC): Dominant market share and highest growth rate, driven by rapid industrialization, urbanization, and robust growth in construction, furniture, and automotive sectors in countries like China, India, and ASEAN nations.

- North America: Mature market characterized by stringent environmental regulations, leading to a focus on low-emission formaldehyde products and advanced material applications, with steady demand from the construction and automotive industries.

- Europe: Highly regulated market with a strong emphasis on sustainable practices and the development of formaldehyde-free alternatives. Growth is largely driven by innovation in resins and specialty chemicals, adapting to strict EU directives.

- Latin America: Emerging market with increasing industrial and construction activities, leading to growing demand for formaldehyde-based products. Brazil and Mexico are key contributors to regional growth.

- Middle East & Africa (MEA): Growing market due to ongoing infrastructure development projects, diversification of economies beyond oil, and increasing manufacturing capacities. Saudi Arabia and UAE are significant players in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Formaldehyde Market.- BASF SE

- Celanese Corporation

- DuPont de Nemours, Inc.

- Momentive Specialty Chemicals Inc.

- Georgia-Pacific Chemicals LLC

- Ashland Global Holdings Inc.

- Huntsman Corporation

- Mitsubishi Chemical Corporation

- Mitsui Chemicals, Inc.

- Lanxess AG

- Evonik Industries AG

- Perstorp Holding AB

- Formosa Plastics Corporation

- Sinopec Corp.

- Saudi Basic Industries Corporation (SABIC)

- LyondellBasell Industries N.V.

- DIC Corporation

- Synthite Industries Ltd.

- Chemanol

Frequently Asked Questions

What is formaldehyde primarily used for?

Formaldehyde is primarily used as a chemical intermediate in the production of resins, particularly urea-formaldehyde (UF), phenol-formaldehyde (PF), and melamine-formaldehyde (MF). These resins are critical components in manufacturing wood-based panels (plywood, particleboard, MDF), adhesives, coatings, and various construction materials. It is also used to produce other chemicals like polyacetals and butanediol, and in diverse applications across automotive, textile, and agricultural industries.

What are the main drivers of the formaldehyde market?

The key drivers of the formaldehyde market include the robust and expanding demand from the global construction and furniture industries for adhesives and composite wood products. Additionally, increasing applications in the automotive sector for lightweight materials and interior components, along with the growing demand for specialty chemicals and derivatives, significantly contribute to market growth.

What are the key challenges facing the formaldehyde industry?

The formaldehyde industry faces significant challenges primarily from stringent health and environmental regulations concerning emissions and exposure limits. Volatile raw material prices, particularly for methanol, also pose a challenge to production costs. Furthermore, negative public perception and the increasing demand for formaldehyde-free alternatives in consumer products necessitate continuous innovation and reformulation efforts from manufacturers.

How is sustainability impacting the formaldehyde market?

Sustainability is profoundly impacting the formaldehyde market by driving innovation towards low-emission (LEF) and ultra-low-emission (ULEF) products and processes. Manufacturers are investing in research and development to create bio-based formaldehyde and develop more environmentally friendly production methods. This focus is aimed at meeting stricter regulatory standards, improving public perception, and catering to the growing demand for greener chemical solutions.

What is the projected growth rate for the formaldehyde market?

The global Formaldehyde market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. This growth is driven by consistent demand across diverse industrial applications, particularly in the construction and automotive sectors, coupled with ongoing advancements in product development and manufacturing processes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted