Ferroalloy Market

Ferroalloy Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702378 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Ferroalloy Market Size

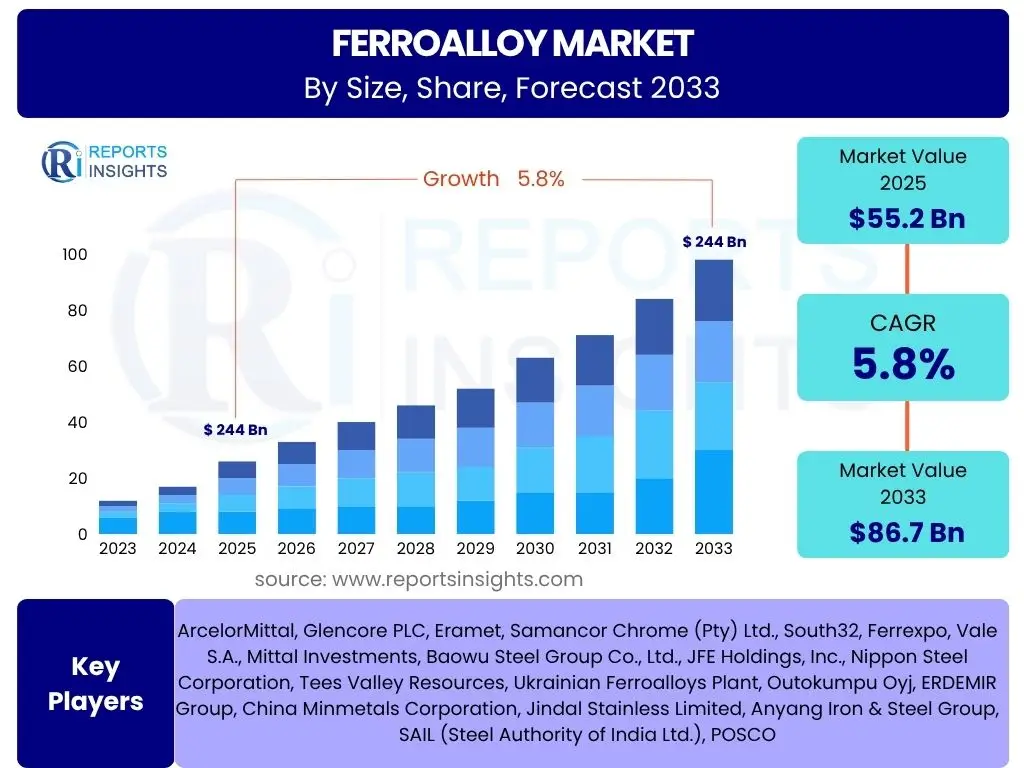

According to Reports Insights Consulting Pvt Ltd, The Ferroalloy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 55.2 Billion in 2025 and is projected to reach USD 86.7 Billion by the end of the forecast period in 2033.

Key Ferroalloy Market Trends & Insights

The Ferroalloy market is experiencing dynamic shifts driven by global industrial growth and evolving metallurgical requirements. Key trends include a heightened focus on high-performance alloys essential for advanced manufacturing sectors like aerospace and automotive. The industry is also observing a significant push towards sustainable production methods, driven by environmental regulations and corporate responsibility initiatives, which includes exploring greener energy sources for smelting and optimizing raw material usage. This paradigm shift impacts investment patterns and technological innovation across the value chain.

Furthermore, the increasing adoption of electric arc furnaces (EAFs) in steelmaking is influencing demand patterns for specific ferroalloys, as EAFs often require different alloy compositions compared to traditional blast furnaces. Digital transformation, encompassing automation and data analytics, is also becoming more prevalent in ferroalloy production, aiming to enhance operational efficiency, product quality, and supply chain resilience. Geopolitical developments and trade policies continue to shape regional market dynamics, affecting supply chains and pricing structures for essential raw materials and finished products.

- Growing demand for high-strength, lightweight steel in automotive and construction.

- Increasing adoption of sustainable and green ferroalloy production technologies.

- Shift in steelmaking processes towards electric arc furnaces (EAFs) impacting alloy demand.

- Rising investment in research and development for advanced metallurgical solutions.

- Fluctuating raw material prices and energy costs influencing production economics.

- Expansion of infrastructure projects in emerging economies driving alloy consumption.

AI Impact Analysis on Ferroalloy

Artificial intelligence is poised to significantly transform the ferroalloy industry by enhancing operational efficiency, optimizing resource utilization, and improving product quality. AI-driven predictive maintenance can minimize equipment downtime in smelting operations, ensuring continuous production and reducing maintenance costs. Furthermore, AI algorithms can analyze vast datasets from production processes to optimize furnace parameters, leading to improved energy efficiency and reduced waste generation. This analytical capability also extends to raw material procurement, where AI can forecast supply chain disruptions and optimize inventory management, thus mitigating risks and ensuring steady material flow.

In quality control, AI-powered vision systems and data analytics can detect impurities or defects in ferroalloy products with greater precision and speed than traditional methods, leading to more consistent product quality and reduced rejections. AI is also being explored for its potential in R&D, accelerating the discovery of new alloy compositions with superior properties and optimizing existing formulations. While the adoption of AI in this capital-intensive industry might be gradual, its long-term benefits in terms of cost reduction, operational excellence, and competitive advantage are becoming increasingly evident, compelling companies to invest in these transformative technologies.

- Predictive maintenance and operational optimization in smelting processes.

- Enhanced quality control and defect detection using AI-powered vision systems.

- Improved supply chain management and raw material procurement forecasting.

- Optimization of energy consumption and reduction of carbon footprint.

- Accelerated research and development for novel alloy compositions.

- Data-driven decision-making for production planning and market analysis.

Key Takeaways Ferroalloy Market Size & Forecast

The ferroalloy market is on a robust growth trajectory, primarily driven by the consistent global demand for steel and stainless steel, which are fundamental to infrastructure development, automotive manufacturing, and consumer goods production. The projected Compound Annual Growth Rate (CAGR) signifies a healthy expansion, indicating sustained investment in industrial and construction sectors worldwide. This growth is further propelled by the increasing focus on specialty alloys for high-performance applications, where precise material properties are critical, suggesting a shift towards higher-value products within the market.

Crucially, the forecast highlights the resilience of the market despite potential headwinds such as raw material price volatility and environmental regulations. The long-term outlook to 2033 underscores the indispensable role of ferroalloys in modern industrial economies. Companies that strategically adapt to evolving technological demands, invest in sustainable practices, and secure stable supply chains are well-positioned to capitalize on this growth. The market's expansion is not merely volume-driven but also increasingly influenced by technological advancements in metallurgy and the imperative for greener production processes.

- Market to reach USD 86.7 Billion by 2033, demonstrating strong growth potential.

- Consistent demand from steel and stainless steel industries remains a primary driver.

- Increasing focus on high-performance and specialty alloys contributing to value growth.

- Sustainability and technological advancements are critical for future market positioning.

- Emerging economies present significant opportunities for market expansion.

Ferroalloy Market Drivers Analysis

The global ferroalloy market is propelled by a confluence of macroeconomic and industry-specific factors. Chief among these is the escalating demand for steel, particularly from developing economies undergoing rapid urbanization and industrialization. Steel, being a primary end-use for ferroalloys, sees increased consumption in construction, automotive, and manufacturing sectors. The transition towards more advanced and high-strength steels for applications requiring lighter yet stronger materials also necessitates a higher demand for specialty ferroalloys like ferrotitanium and ferrovanadium.

Additionally, the burgeoning automotive industry, particularly with the rise of electric vehicles (EVs), drives demand for specific alloys that offer improved corrosion resistance, strength, and lightweight properties. The global push for renewable energy infrastructure, including wind turbines and solar panels, also contributes to the market's expansion, as these applications require specialized steel grades for their structural components. Infrastructure development projects worldwide, from roads and bridges to commercial buildings and utilities, continue to underpin the steady demand for various ferroalloys, ensuring a robust market outlook.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Steel Production & Demand | +1.8% | Global, particularly Asia Pacific (China, India) | 2025-2033 |

| Growth in Automotive & Transportation Industry | +1.2% | North America, Europe, Asia Pacific | 2025-2033 |

| Infrastructure Development & Urbanization | +1.0% | Emerging Economies (APAC, Latin America, MEA) | 2025-2033 |

| Rising Demand for Specialty Alloys | +0.8% | Global, especially developed markets | 2025-2033 |

| Expansion of Renewable Energy Sector | +0.5% | Europe, North America, Asia Pacific | 2025-2030 |

Ferroalloy Market Restraints Analysis

Despite the positive growth outlook, the ferroalloy market faces significant restraints that could temper its expansion. One primary concern is the volatility of raw material prices, particularly for key ores like chrome, manganese, and silicon, which are subject to supply disruptions, geopolitical tensions, and speculative trading. This unpredictability makes long-term planning and cost management challenging for manufacturers, often leading to fluctuating profit margins and production adjustments. High energy costs, especially for electricity-intensive smelting processes, also represent a substantial burden, impacting the competitiveness of producers in regions with expensive power grids.

Furthermore, stringent environmental regulations aimed at curbing carbon emissions and pollution pose considerable operational and financial challenges. Compliance with these regulations often requires significant investments in cleaner technologies, waste treatment, and emission reduction systems, which can increase production costs and potentially limit output for non-compliant facilities. Additionally, the global market is susceptible to oversupply issues, particularly from major producing nations, leading to price erosion and reduced profitability for all market participants. Trade barriers, tariffs, and anti-dumping duties imposed by various countries also create impediments to seamless international trade, disrupting supply chains and affecting market access for ferroalloy products.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -1.5% | Global | Ongoing |

| High Energy Costs & Consumption | -1.0% | Europe, Asia (non-subsidized regions) | 2025-2033 |

| Stringent Environmental Regulations | -0.8% | Europe, North America, China | 2025-2033 |

| Geopolitical Instability & Trade Barriers | -0.7% | Global, specific trade blocs | Ongoing |

| Market Oversupply & Price Erosion | -0.5% | Global, particularly major producing regions | Short to Medium Term |

Ferroalloy Market Opportunities Analysis

The ferroalloy market is rich with opportunities, primarily stemming from technological advancements and the increasing emphasis on sustainable practices. The development of advanced steel grades, such as high-strength low-alloy (HSLA) steels and ultra-high-strength steels, for lightweighting in automotive and aerospace applications, creates new avenues for specialized ferroalloys. Innovations in metallurgy that enable more precise alloying and improved material performance will further drive demand for customized ferroalloy solutions. Furthermore, the growing trend of green steel production, which involves using hydrogen or renewable energy sources, presents a significant opportunity for ferroalloy producers to adapt their processes and offer environmentally friendly products, aligning with global sustainability goals.

The expansion of electric vehicle (EV) manufacturing is another promising area, as EVs require specific steel and aluminum alloys for their body structures, battery casings, and motor components, necessitating a diverse range of ferroalloys. The circular economy model, emphasizing recycling and resource efficiency, also creates opportunities for recovering ferroalloys from industrial waste and end-of-life products, reducing reliance on virgin raw materials and promoting a more sustainable supply chain. Lastly, untapped markets in emerging economies, driven by rapid industrialization and urbanization, offer substantial growth potential for ferroalloy consumption as these regions continue to develop their manufacturing and infrastructure capabilities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Advancements in Metallurgy | +1.5% | Global | 2025-2033 |

| Growing Demand for Green Steel | +1.2% | Europe, North America, Japan | 2027-2033 |

| Recycling and Circular Economy Initiatives | +0.9% | Global, especially developed markets | 2025-2033 |

| Expansion of Electric Vehicle (EV) Production | +0.8% | China, Europe, North America | 2025-2033 |

| Untapped Markets in Emerging Economies | +0.6% | Africa, Southeast Asia, Latin America | 2025-2033 |

Ferroalloy Market Challenges Impact Analysis

The ferroalloy market faces several inherent challenges that can impede its growth and stability. One significant hurdle is the vulnerability to global economic downturns, as the industry's demand is directly tied to the health of the steel, automotive, and construction sectors. Any slowdown in these end-user industries directly translates to reduced demand for ferroalloys, impacting sales volumes and profitability. Moreover, the capital-intensive nature of ferroalloy production, requiring substantial investments in furnaces, infrastructure, and technology, makes it challenging for new players to enter the market and for existing ones to scale up or modernize quickly, especially during periods of economic uncertainty.

Supply chain disruptions, ranging from geopolitical conflicts affecting raw material supply to logistical bottlenecks and energy crises, pose a continuous threat to stable production and timely delivery. The industry is also grappling with the challenge of managing and disposing of significant amounts of industrial waste and by-products generated during the smelting process, which requires costly and environmentally compliant solutions. Additionally, the increasing focus on carbon footprint reduction and achieving net-zero emissions mandates substantial shifts in production methods, compelling companies to invest heavily in decarbonization technologies that may not yet be commercially viable at scale, adding to the operational burden and financial risk.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Economic Slowdown & Demand Volatility | -1.3% | Global | Short to Medium Term |

| Supply Chain Disruptions & Logistics Issues | -0.9% | Global | Ongoing |

| High Capital Investment & Maintenance Costs | -0.7% | Global | Long Term |

| Waste Management & By-product Utilization | -0.6% | Global, particularly regions with strict waste laws | 2025-2033 |

| Achieving Decarbonization & Net-Zero Goals | -0.5% | Europe, North America, Japan | 2030 onwards |

Ferroalloy Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Ferroalloy Market, offering a detailed understanding of its current size, historical performance, and future growth projections from 2025 to 2033. It meticulously examines key market trends, drivers, restraints, opportunities, and challenges that shape the industry landscape. The report also includes a thorough segmentation analysis by type, application, and end-use industry, alongside a detailed regional outlook. Furthermore, it identifies the impact of emerging technologies like AI and provides profiles of leading market players, offering strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 55.2 Billion |

| Market Forecast in 2033 | USD 86.7 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, Glencore PLC, Eramet, Samancor Chrome (Pty) Ltd., South32, Ferrexpo, Vale S.A., Mittal Investments, Baowu Steel Group Co., Ltd., JFE Holdings, Inc., Nippon Steel Corporation, Tees Valley Resources, Ukrainian Ferroalloys Plant, Outokumpu Oyj, ERDEMIR Group, China Minmetals Corporation, Jindal Stainless Limited, Anyang Iron & Steel Group, SAIL (Steel Authority of India Ltd.), POSCO |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The ferroalloy market is comprehensively segmented based on various critical parameters, including product type, application, and end-use industry. This granular segmentation provides a detailed understanding of demand patterns and growth drivers across different market verticals. Each segment is analyzed for its specific characteristics, technological requirements, and market dynamics, offering a holistic view of the industry's intricate structure. Understanding these segments is crucial for identifying niche opportunities, assessing competitive landscapes, and formulating targeted business strategies within the diverse ferroalloy ecosystem.

The market's performance is highly dependent on the demand generated by these distinct segments. For instance, the steel manufacturing segment, particularly the production of carbon, alloy, and stainless steels, remains the largest consumer of ferroalloys, dictating overall market trends. However, emerging applications in specialized industries and the shift towards advanced materials are influencing the growth of specific ferroalloy types. This detailed segmentation enables stakeholders to pinpoint high-growth areas and allocate resources effectively, adapting to the evolving needs of various industrial sectors.

- By Type:

- Ferrosilicon: Primarily used as a deoxidizer and alloying agent in steel and cast iron production.

- Ferrochrome: Essential for producing stainless steel, imparting corrosion resistance and hardness.

- Ferromanganese: Used as a deoxidizer, desulfurizer, and alloying element in steelmaking.

- Ferrotitanium: Applied in steel to control grain size, deoxidize, and improve properties.

- Ferronickel: Key alloy for stainless steel and other high-nickel alloys.

- Ferrovanadium: Used to increase strength, toughness, and wear resistance in steel.

- Ferromolybdenum: Enhances the strength, hardenability, and corrosion resistance of steel.

- Other Ferroalloys: Includes ferrotungsten, ferrophosphorus, ferroniobium, etc., for specialized applications.

- By Application:

- Steel Manufacturing:

- Carbon Steel: Largest application, used in construction, machinery.

- Alloy Steel: Used for specific properties like high strength, wear resistance.

- Stainless Steel: Requires high chrome and nickel content for corrosion resistance.

- Tool Steel: Demands specific alloys for hardness and abrasion resistance.

- Foundry:

- Cast Iron: Ferroalloys modify microstructure and properties.

- Steel Castings: Used for deoxidation and alloying.

- Welding Electrodes: Ferroalloys impart specific properties to weld metal.

- Others: Powder metallurgy, chemicals, and specialized non-ferrous applications.

- Steel Manufacturing:

- By End-Use Industry:

- Construction & Infrastructure: Bridges, buildings, pipes, and structural components.

- Automotive & Transportation: Vehicle bodies, engine parts, chassis, and lightweight components.

- Machinery & Equipment: Industrial machinery, heavy equipment, agricultural tools.

- Consumer Goods: Appliances, utensils, electronics components.

- Energy & Power: Power generation equipment, oil & gas pipelines, renewable energy structures.

- Oil & Gas: Drilling equipment, pipelines, and structural components requiring high strength and corrosion resistance.

Regional Highlights

- Asia Pacific (APAC): The dominant region in the ferroalloy market, driven by robust steel production in China and India. Rapid industrialization, massive infrastructure development projects, and a burgeoning automotive sector in these countries underpin strong demand. China, in particular, is a major producer and consumer, although environmental regulations are increasingly influencing production methods. Southeast Asian nations are also emerging as significant consumers due to growing manufacturing bases and construction activities.

- Europe: A mature market characterized by stringent environmental regulations and a focus on high-value, specialty steel production. Countries like Germany, Italy, and France are key consumers due to their advanced automotive, machinery, and renewable energy sectors. The region is increasingly emphasizing sustainable production methods and recycling initiatives, driving demand for greener ferroalloy products and technologies.

- North America: Exhibits steady demand, primarily from the automotive, construction, and oil & gas industries. The region is witnessing a resurgence in domestic manufacturing and infrastructure investment, supporting ferroalloy consumption. Technological advancements in steelmaking and a shift towards electric arc furnace (EAF) production are influencing the demand for specific ferroalloy types.

- Latin America: Driven by growth in infrastructure development, mining, and automotive sectors, particularly in Brazil and Mexico. The region holds significant raw material reserves for certain ferroalloys, making it an important production hub. Economic fluctuations and political stability can influence market dynamics, but long-term growth prospects remain positive due to urbanization and industrial expansion.

- Middle East and Africa (MEA): Emerging as a significant market due to ongoing urbanization, industrial projects, and diversification efforts away from oil economies. Countries like Saudi Arabia, UAE, and South Africa are investing heavily in infrastructure and manufacturing, boosting steel and thus ferroalloy demand. South Africa is also a major producer of chrome and manganese ores, playing a critical role in the global supply chain.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ferroalloy Market.- ArcelorMittal

- Glencore PLC

- Eramet

- Samancor Chrome (Pty) Ltd.

- South32

- Ferrexpo

- Vale S.A.

- Mittal Investments

- Baowu Steel Group Co., Ltd.

- JFE Holdings, Inc.

- Nippon Steel Corporation

- Tees Valley Resources

- Ukrainian Ferroalloys Plant

- Outokumpu Oyj

- ERDEMIR Group

- China Minmetals Corporation

- Jindal Stainless Limited

- Anyang Iron & Steel Group

- SAIL (Steel Authority of India Ltd.)

- POSCO

Frequently Asked Questions

What are ferroalloys primarily used for?

Ferroalloys are primarily used in the production of steel and cast iron, where they act as deoxidizers, desulfurizers, and alloying agents to impart specific properties such as strength, hardness, corrosion resistance, and ductility. They are crucial for manufacturing various types of steel, including carbon steel, alloy steel, and stainless steel, which are essential for industries like construction, automotive, and machinery.

Which factors are driving the growth of the ferroalloy market?

The ferroalloy market's growth is primarily driven by the increasing global demand for steel, particularly from rapid urbanization and infrastructure development in emerging economies. Additionally, the expansion of the automotive industry, especially with the rise of electric vehicles requiring specialized high-strength lightweight steels, and the growth in the renewable energy sector contribute significantly to market expansion.

What are the key challenges facing the ferroalloy industry?

Key challenges for the ferroalloy industry include volatile raw material prices, high energy consumption and associated costs, stringent environmental regulations requiring significant investments in cleaner technologies, and geopolitical instabilities that can disrupt supply chains. The market also faces potential oversupply issues and the need to manage industrial waste effectively.

How is AI impacting the ferroalloy market?

AI is impacting the ferroalloy market by enabling predictive maintenance for production equipment, optimizing smelting processes for greater energy efficiency and reduced waste, and enhancing quality control through advanced defect detection. It also aids in more accurate demand forecasting and supply chain management, contributing to overall operational excellence and resource utilization.

Which region dominates the ferroalloy market?

The Asia Pacific (APAC) region currently dominates the ferroalloy market. This is primarily due to the large-scale steel production and rapid industrialization in countries like China and India, coupled with extensive infrastructure development and significant growth in the automotive and manufacturing sectors across the region.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted