DPF Retrofit Market

DPF Retrofit Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700530 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

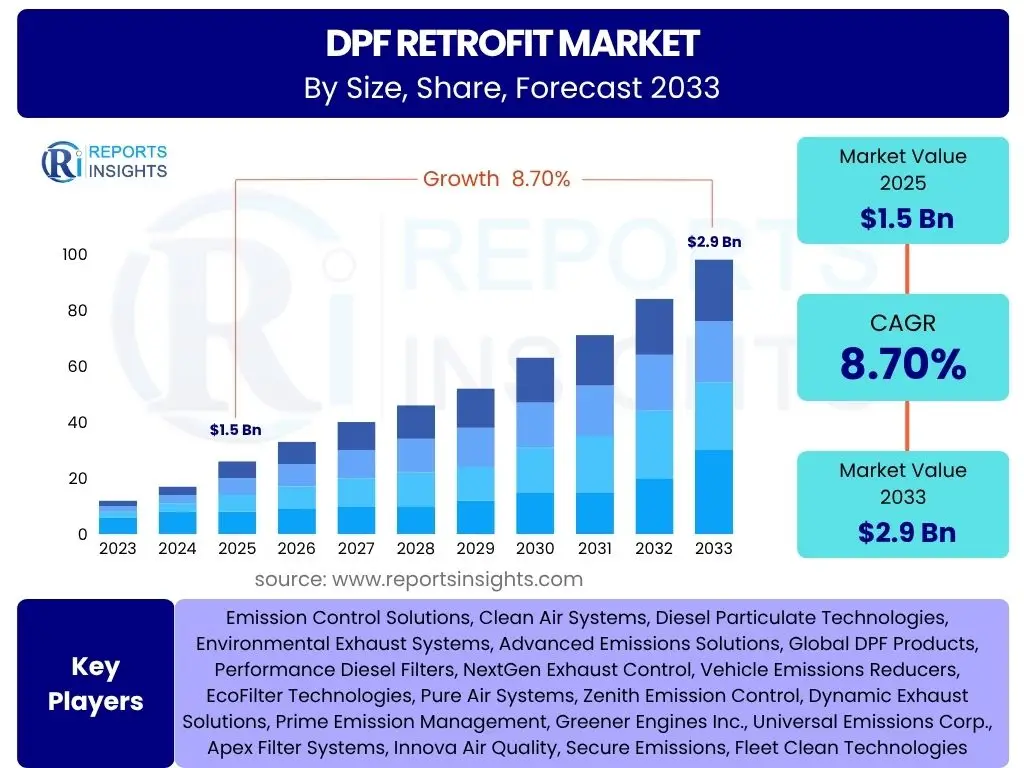

DPF Retrofit Market Size

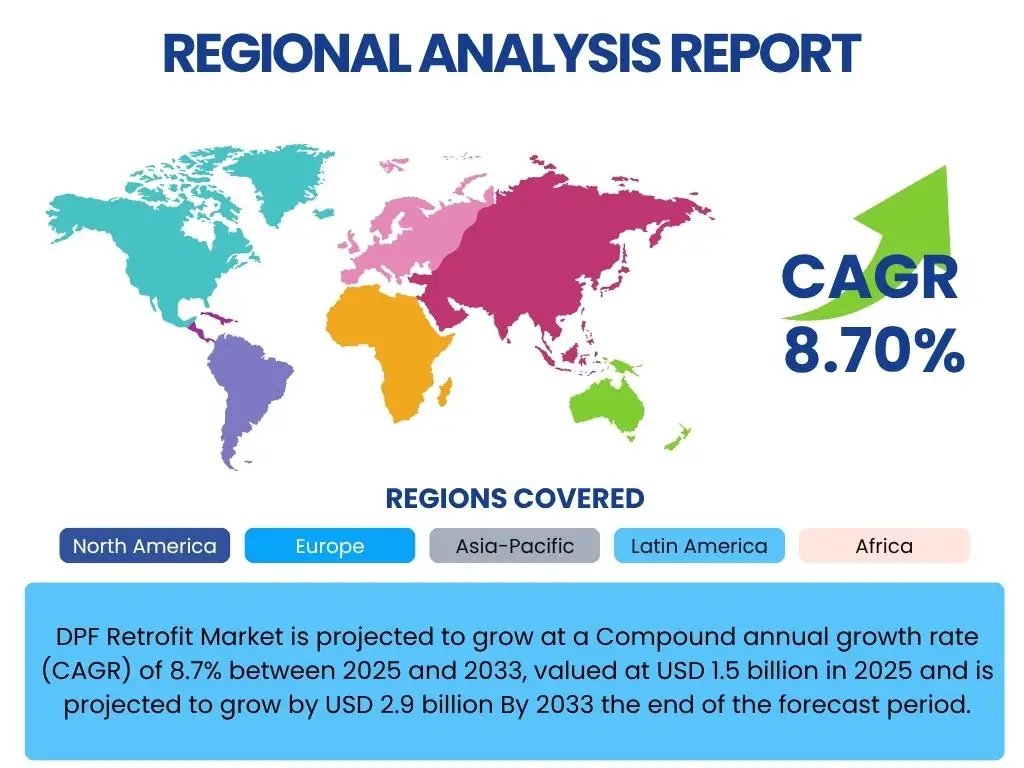

DPF Retrofit Market is projected to grow at a Compound annual growth rate (CAGR) of 8.7% between 2025 and 2033, valued at USD 1.5 billion in 2025 and is projected to grow by USD 2.9 billion By 2033 the end of the forecast period.

Key DPF Retrofit Market Trends & Insights

The DPF retrofit market is currently experiencing dynamic shifts driven by increasing environmental consciousness and evolving regulatory landscapes worldwide. A prominent trend involves the continuous advancement in DPF technology, focusing on improved filtration efficiency and extended service life to meet more stringent emission standards. There's also a growing emphasis on cost-effective retrofit solutions, making DPF technology accessible for a wider range of older commercial and passenger vehicles. This push for broader adoption is further fueled by government incentives and urban low-emission zone initiatives. Additionally, market consolidation and strategic partnerships among key players are becoming more frequent, aiming to enhance research and development capabilities and expand geographical reach for distribution and installation services. The integration of telematics and smart monitoring systems for DPF performance is another emerging trend, offering predictive maintenance and real-time compliance verification, which significantly adds value for fleet operators.

- Stricter global emission standards for internal combustion engines.

- Technological advancements in DPF materials and regeneration methods.

- Increasing adoption of DPF retrofits in older vehicle fleets.

- Growing focus on cost-effective and long-lasting retrofit solutions.

- Expansion of low-emission zones in urban areas.

- Integration of smart monitoring and diagnostic systems for DPFs.

- Rising environmental awareness among consumers and businesses.

- Shift towards specialized and application-specific retrofit solutions.

AI Impact Analysis on DPF Retrofit

Artificial Intelligence (AI) is poised to significantly transform the DPF retrofit market by enhancing various aspects of design, deployment, and maintenance. AI-driven analytics can optimize DPF regeneration cycles, predict maintenance needs, and provide real-time performance monitoring, leading to improved efficiency and reduced operational costs for vehicle operators. Furthermore, AI can assist in the development of new DPF materials and designs by simulating various operational conditions and material properties, accelerating innovation and leading to more effective and durable retrofit solutions. Its application also extends to supply chain optimization, demand forecasting, and inventory management for retrofit components, streamlining the entire value chain. In the installation and diagnostic phases, AI-powered tools can offer precise guidance for technicians, ensuring correct fitment and rapid troubleshooting, thereby minimizing downtime and maximizing the efficacy of the retrofit process.

- Predictive maintenance and optimized DPF regeneration cycles.

- AI-driven material science for advanced filter development.

- Enhanced diagnostics and troubleshooting for DPF systems.

- Supply chain optimization and demand forecasting for retrofit components.

- Personalized retrofit recommendations based on vehicle usage data.

- Automated quality control in DPF manufacturing processes.

Key Takeaways DPF Retrofit Market Size & Forecast

- The DPF retrofit market is set for robust growth, driven by stringent emission norms and increasing vehicle longevity.

- Significant market expansion is anticipated, reaching nearly double its 2025 valuation by 2033.

- Technological innovation and AI integration are key enablers for market evolution and efficiency gains.

- Regulatory support and the expansion of low-emission zones are critical growth catalysts.

- The aftermarket segment is expected to drive substantial demand for retrofit solutions.

DPF Retrofit Market Drivers Analysis

The DPF retrofit market is propelled by a confluence of factors, primarily centered around escalating global concerns over air quality and the resulting stringent emission regulations. Governments worldwide are implementing stricter policies to curb particulate matter emissions from diesel vehicles, making DPF retrofitting a necessary compliance measure for older fleets that do not meet current standards. This regulatory push creates a direct and often mandatory demand for retrofit solutions. Furthermore, the economic viability of retrofitting existing vehicles compared to purchasing new, compliant vehicles acts as a significant driver, especially for commercial fleet operators looking to extend the operational life of their assets while adhering to environmental mandates. The growing awareness among businesses and the public regarding the environmental and health impacts of diesel emissions also plays a crucial role, fostering a more receptive market for DPF retrofit technologies and services. This societal shift towards sustainability encourages investment in cleaner transportation solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Emission Regulations | +2.1% | Europe, North America, Asia Pacific (Tier 1 cities) | Short-term to Long-term |

| Aging Vehicle Fleet | +1.8% | Globally, particularly in emerging economies | Medium-term to Long-term |

| Cost-effectiveness vs. New Vehicle Purchase | +1.5% | Globally, especially for commercial fleets | Short-term to Medium-term |

| Government Incentives and Subsidies | +1.3% | Specific countries in Europe and Asia | Short-term to Medium-term |

| Increasing Environmental Awareness | +1.0% | Developed nations and progressive urban centers | Medium-term to Long-term |

DPF Retrofit Market Restraints Analysis

Despite the strong drivers, the DPF retrofit market faces several significant restraints that could temper its growth trajectory. The relatively high upfront cost of DPF retrofit systems and their installation can be a major deterrent for vehicle owners, particularly individuals or small businesses with limited budgets. While cost-effective compared to new vehicle purchases, the initial investment can still be substantial enough to cause hesitation. Another notable restraint is the lack of widespread awareness and understanding regarding the benefits and compliance requirements of DPF retrofits among certain segments of vehicle owners and operators. This knowledge gap often leads to delayed adoption or reluctance to invest. Furthermore, technical complexities associated with integrating retrofit systems into diverse vehicle models and engine types, coupled with the need for specialized installation and maintenance expertise, can pose significant challenges, limiting broader market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Cost of Retrofit Systems | -1.9% | Globally, especially for smaller fleets and individual owners | Short-term to Medium-term |

| Lack of Awareness and Information | -1.5% | Emerging markets and rural areas | Medium-term |

| Technical Complexities and Installation Challenges | -1.2% | Varied by vehicle type and region | Short-term |

| Competition from New Electric Vehicles | -1.0% | Developed markets with strong EV adoption | Long-term |

| Perceived Durability and Maintenance Issues | -0.8% | Globally, based on past experiences | Short-term |

DPF Retrofit Market Opportunities Analysis

The DPF retrofit market is ripe with opportunities that can significantly bolster its growth and expansion. One of the most promising avenues lies in the continuous advancement and development of more efficient and cost-effective DPF technologies. Innovations in filter materials, regeneration methods, and diagnostic capabilities can address existing restraints and make retrofitting a more attractive and reliable option. The expansion into developing and emerging markets, particularly in regions where environmental regulations are tightening and older vehicle fleets are prevalent, presents a substantial untapped customer base. These regions often lack the immediate infrastructure for widespread new vehicle adoption, making retrofitting a practical solution for emission compliance. Furthermore, strategic collaborations and partnerships between DPF manufacturers, vehicle service providers, and governmental bodies can streamline the adoption process, offer bundled solutions, and facilitate broader market penetration through shared expertise and resources. The growing demand for public transportation and logistics, especially in urban areas, necessitates continuous operation of existing commercial fleets, presenting a persistent opportunity for retrofit solutions to ensure compliance without major capital expenditure on new vehicles.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced & Cost-Effective DPF Technologies | +1.8% | Globally, driven by R&D hubs | Medium-term to Long-term |

| Expansion into Emerging Markets (e.g., Southeast Asia, Latin America) | +1.6% | Asia Pacific, Latin America, parts of Africa | Medium-term to Long-term |

| Strategic Partnerships and Collaborations | +1.4% | Globally, across the value chain | Short-term to Medium-term |

| Growing Demand for Commercial Vehicle Retrofitting | +1.2% | Globally, particularly in logistics and public transport | Short-term to Long-term |

| Leveraging IoT and Telematics for Performance Monitoring | +1.0% | Developed markets and large fleet operators | Medium-term |

DPF Retrofit Market Challenges Impact Analysis

The DPF retrofit market, while promising, must navigate several critical challenges that can impede its growth and widespread adoption. One significant challenge is the ongoing fluctuating prices and availability of raw materials essential for DPF manufacturing, such as platinum group metals. These volatilities can directly impact production costs and, consequently, the final price of retrofit systems, making them less attractive to cost-sensitive buyers. Another hurdle is the varying and often complex regulatory landscapes across different regions and countries. Differences in emission standards, certification processes, and enforcement mechanisms can create market fragmentation, requiring manufacturers to adapt their products and strategies, leading to inefficiencies and increased compliance costs. Furthermore, the rapid advancements in alternative vehicle technologies, particularly electric vehicles and fuel cell vehicles, pose a long-term threat. As these cleaner alternatives become more affordable and prevalent, the demand for DPF retrofits for internal combustion engines might naturally diminish over time. Moreover, ensuring proper installation and ongoing maintenance for retrofit systems requires a skilled labor force, which can be scarce in some regions, leading to quality control issues and customer dissatisfaction.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Fluctuating Raw Material Prices | -1.7% | Globally, impacts manufacturing costs | Short-term to Medium-term |

| Varying and Complex Regulatory Landscapes | -1.4% | Globally, especially across continents | Medium-term |

| Competition from New, Cleaner Vehicle Technologies | -1.1% | Developed economies and innovation hubs | Long-term |

| Lack of Skilled Labor for Installation & Maintenance | -0.9% | Globally, particularly in niche markets | Short-term to Medium-term |

| Public Perception and Trust Issues | -0.7% | Globally, varies by past experiences | Short-term |

DPF Retrofit Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the DPF Retrofit Market, covering historical performance, current dynamics, and future projections. It meticulously details market size, growth trends, key drivers, significant restraints, emerging opportunities, and prevailing challenges, offering a holistic view for stakeholders. The report segments the market by various criteria, including vehicle type, application, and end-use, providing granular insights into specific market niches. It also offers a detailed regional analysis, highlighting key country-level developments and regulatory impacts. Furthermore, the study profiles leading market players, examining their strategies, product portfolios, and competitive positioning. This report is an essential resource for businesses, investors, and policymakers seeking to understand the market's complexities and capitalize on its growth potential, ensuring informed decision-making in the evolving landscape of emission control technologies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 billion |

| Market Forecast in 2033 | USD 2.9 billion |

| Growth Rate | 8.7% (CAGR from 2025 to 2033) |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Emission Control Solutions, Clean Air Systems, Diesel Particulate Technologies, Environmental Exhaust Systems, Advanced Emissions Solutions, Global DPF Products, Performance Diesel Filters, NextGen Exhaust Control, Vehicle Emissions Reducers, EcoFilter Technologies, Pure Air Systems, Zenith Emission Control, Dynamic Exhaust Solutions, Prime Emission Management, Greener Engines Inc., Universal Emissions Corp., Apex Filter Systems, Innova Air Quality, Secure Emissions, Fleet Clean Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The DPF Retrofit Market is comprehensively analyzed across various segments to provide a detailed understanding of its diverse components and drivers. These segmentations are critical for identifying niche opportunities, understanding specific demand patterns, and formulating targeted market strategies.-

By Vehicle Type: This segment differentiates the market based on the type of vehicles undergoing DPF retrofits. It primarily includes Commercial Vehicles, which are further broken down into Heavy-duty, Medium-duty, and Light-duty vehicles, recognizing their varied usage patterns and regulatory compliance needs. Passenger Vehicles form the other significant sub-segment, driven by urban emission zones and individual environmental consciousness. The distinct operational requirements and emission profiles of these vehicle types lead to unique retrofit solutions and market demands.

-

By Application: This segmentation focuses on where the retrofitted vehicles are primarily utilized, distinguishing between On-road Vehicles and Off-road Vehicles. On-road applications encompass trucks, buses, and passenger cars used for daily transportation and logistics. Off-road applications cover heavy machinery used in Construction, Agriculture, and Mining, where robust and durable DPF solutions are essential due to harsh operating environments. Understanding these applications helps in tailoring DPF technology to specific operational stresses and regulatory frameworks.

-

By End-use: This segment categorizes the market by the nature of the entity acquiring the retrofit solutions. The Aftermarket segment represents existing vehicles that are retrofitted post-production to meet new emission standards, forming the largest portion of the DPF retrofit market. Original Equipment Manufacturers (OEMs) also play a role, particularly for new vehicles that might require specific DPF integrations or certifications, or for specialized industrial equipment that falls under retrofit mandates even at the point of initial sale. This distinction highlights different sales channels and business models within the market.

-

By Material Type: DPFs are constructed from various materials, each offering different performance characteristics and cost profiles. This segment includes Cordierite, known for its thermal shock resistance; Silicon Carbide, favored for its high filtration efficiency and durability; and Metal Fibers, which offer different regeneration capabilities. Other materials and composite solutions are also explored, reflecting ongoing research and development in filter media to enhance performance and reduce costs. The choice of material often depends on the specific engine type, expected operating conditions, and desired service life.

-

By Technology: This segmentation differentiates between the primary DPF designs available. Wall-Flow Filters are the most common type, offering high filtration efficiency by forcing exhaust gases through porous walls. Flow-Through Filters, while less common for heavy-duty applications, represent an alternative design that allows for lower back pressure in certain scenarios. Understanding these technological distinctions is crucial for assessing performance, cost-effectiveness, and suitability for various vehicle and engine configurations. Continued innovation in these technologies aims to improve regeneration effectiveness and overall system reliability.

Regional Highlights

The DPF Retrofit Market exhibits significant regional variations, primarily driven by differing emission regulations, fleet compositions, and economic conditions.- Europe: This region stands out as a top-performing market for DPF retrofits, largely due to its pioneering and continuously tightening Euro emission standards (Euro 5, Euro 6, etc.) and the widespread implementation of Low Emission Zones (LEZs) in major urban centers. Countries like Germany, the UK, France, and Italy have aggressively pushed for cleaner air, mandating retrofits for older diesel vehicles, especially commercial fleets and public transport. This strong regulatory framework, combined with significant government incentives, makes Europe a critical hub for DPF retrofit adoption and innovation. The emphasis on sustainable urban mobility also fuels steady demand.

- North America: The United States and Canada represent a substantial market, driven by federal and state-level emission regulations (e.g., EPA standards, California Air Resources Board - CARB). While regulatory approaches may differ from Europe, there is a strong push to reduce particulate matter from heavy-duty trucks and buses, which constitute a significant portion of the commercial fleet. The sheer size of the vehicle fleet and the long operational life of commercial vehicles create a consistent demand for retrofit solutions, especially in metropolitan areas and states with more stringent air quality mandates. Economic incentives and compliance programs also play a key role here.

- Asia Pacific (APAC): This region is emerging as a rapidly growing market, propelled by escalating air pollution concerns in densely populated cities and the subsequent adoption of stricter emission norms by countries like China, India, and Japan. While some parts of APAC are still developing comprehensive retrofit programs, the immense and aging vehicle fleet, coupled with increasing environmental awareness, presents colossal growth opportunities. Investment in DPF technology and infrastructure is rapidly accelerating, particularly in major industrial and urban centers, making it a crucial future market.

- Latin America: Countries in Latin America, such as Brazil and Mexico, are increasingly adopting emission standards similar to those in Europe and North America. The growing focus on improving urban air quality and controlling vehicle emissions is leading to a gradual but steady increase in DPF retrofit demand. The market here is still nascent compared to more developed regions but offers significant potential as regulatory frameworks mature and awareness increases.

- Middle East and Africa (MEA): This region is characterized by varying levels of regulatory stringency. While some countries are beginning to implement emission controls, widespread adoption of DPF retrofits is still in early stages. However, rapid urbanization and increasing vehicle populations, particularly in commercial and public transport sectors, are creating a long-term potential for market growth as environmental concerns gain traction and regulations tighten.

Top Key Players:

The market research report covers the analysis of key stake holders of the DPF Retrofit Market. Some of the leading players profiled in the report include -- Tenneco

- Cummins Inc.

- Faurecia

- Bosal Group

- Eberspächer Climate Control Systems GmbH & Co. KG

- CDTi Advanced Materials Inc.

- JM (Johnson Matthey)

- MANN+HUMMEL

- NGK Insulators Ltd.

- Dinex A/S

- Emitec GmbH

- HJS Emission Technology GmbH & Co. KG

- Proventia Solutions Oy

- Hug Engineering AG

- Engine Control Systems (ECS)

- Clean Diesel Technologies Inc.

- Cataler Corporation

- Ibiden Co., Ltd.

- Purem by Eberspaecher

- Friedrich Boysen GmbH & Co. KG

Frequently Asked Questions:

What is a DPF retrofit and why is it important?

A DPF (Diesel Particulate Filter) retrofit involves installing an exhaust aftertreatment system on existing diesel vehicles to reduce harmful particulate matter emissions. It is crucial for improving air quality, particularly in urban areas, and for enabling older diesel vehicles to comply with modern, stricter environmental regulations, thereby extending their operational lifespan and avoiding emission-related penalties.How does a DPF retrofit system work?

A DPF retrofit system functions by physically trapping diesel particulate matter (soot and ash) from the exhaust gases. The trapped particulates are then periodically removed through a process called regeneration, where the filter is heated to a high temperature, burning off the soot and converting it into harmless ash. This process ensures the filter maintains its efficiency and does not clog, allowing the vehicle to continue operating with significantly reduced emissions.What are the main benefits of installing a DPF retrofit?

Installing a DPF retrofit offers several key benefits, including compliance with stringent emission standards, enabling continued access to low-emission zones, significantly improving air quality by reducing harmful particulate matter, and extending the operational life of existing vehicles. It also provides a cost-effective alternative to purchasing new, compliant vehicles, reducing capital expenditure for fleet operators and individual owners.Which types of vehicles can be equipped with DPF retrofits?

DPF retrofits can be installed on a wide range of diesel vehicles, primarily focusing on older models that predate the integration of factory-fitted DPFs. This includes various commercial vehicles such as heavy-duty trucks, buses, and light commercial vehicles, as well as passenger cars. The suitability often depends on the vehicle's engine size, exhaust system configuration, and specific regulatory requirements in a given region.What is the future outlook for the DPF retrofit market?

The DPF retrofit market is projected for continued growth, driven by an ongoing global emphasis on air quality, the expansion of low-emission zones, and the economic benefits of extending vehicle lifespans. While advancements in electric and alternative fuel vehicles pose a long-term shift, the vast existing diesel fleet ensures a sustained demand for retrofit solutions in the medium term, particularly as regulations evolve and technologies become more efficient and affordable.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted