Data Centre Server Market

Data Centre Server Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700642 | Last Updated : July 26, 2025 |

Format : ![]()

![]()

![]()

![]()

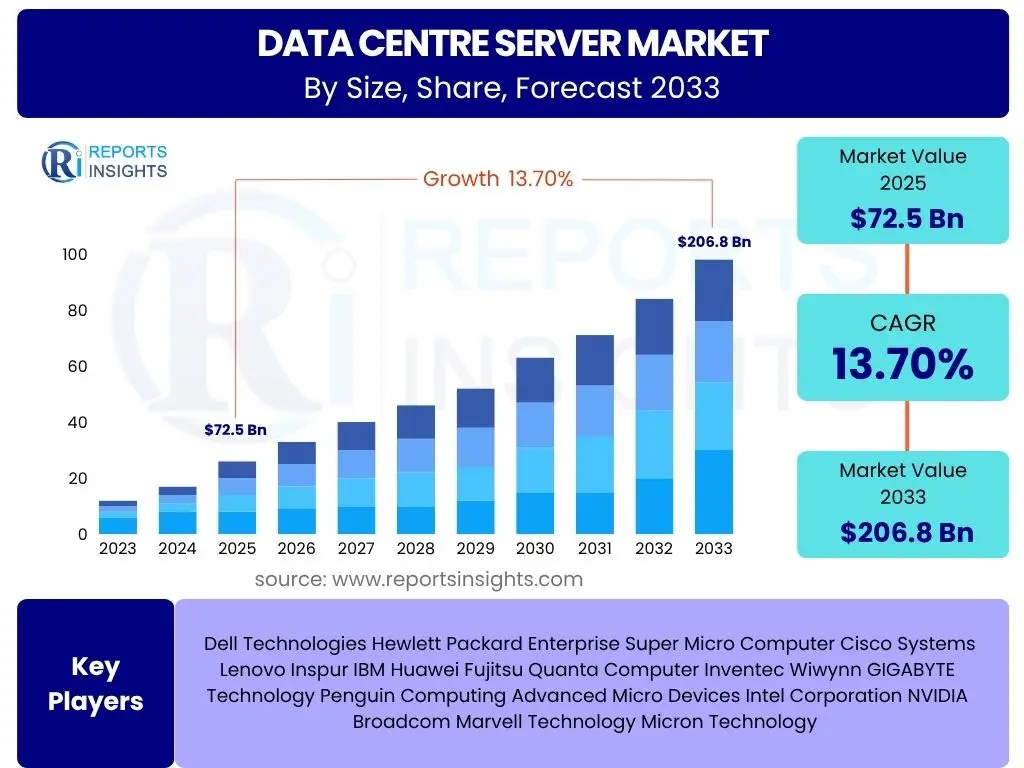

Data Centre Server Market Size

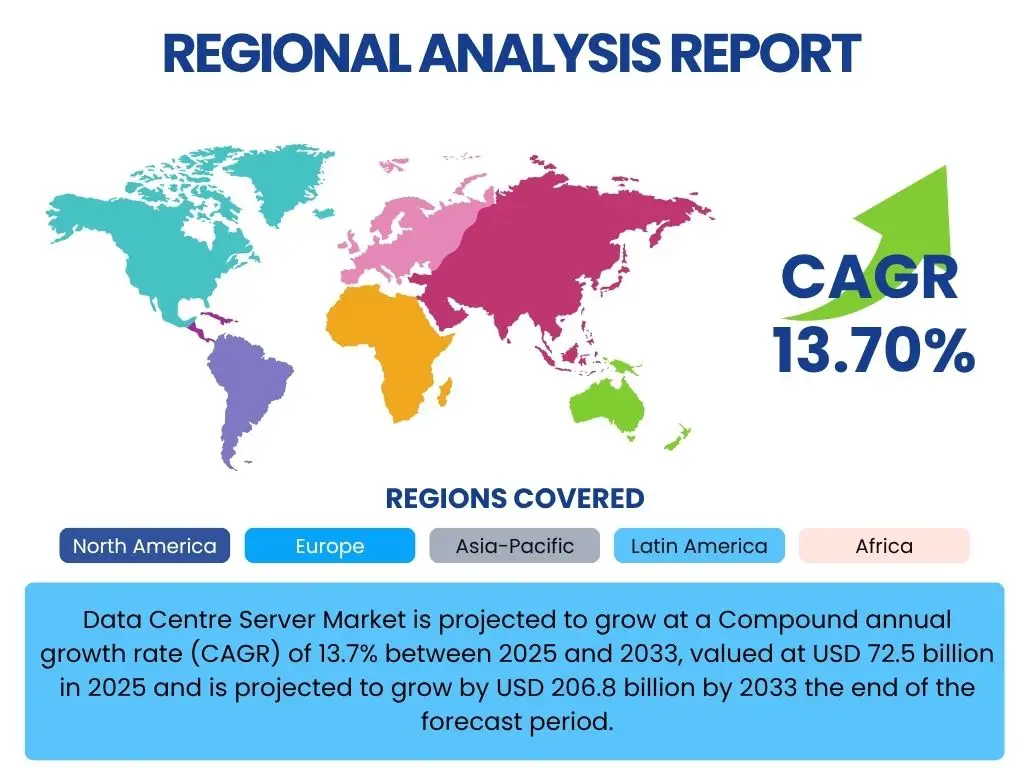

Data Centre Server Market is projected to grow at a Compound annual growth rate (CAGR) of 13.7% between 2025 and 2033, valued at USD 72.5 billion in 2025 and is projected to grow by USD 206.8 billion by 2033 the end of the forecast period.

Key Data Centre Server Market Trends & Insights

The data centre server market is witnessing transformative trends driven by the escalating demand for high-performance computing, the widespread adoption of cloud-based services, and the relentless expansion of digital transformation initiatives across industries. These trends are fundamentally reshaping how organizations manage and process data, pushing the boundaries of traditional server architectures and fostering innovation in hardware and software solutions. The shift towards more agile, scalable, and energy-efficient infrastructure is paramount, directly influencing procurement decisions and technological advancements within the sector. Furthermore, the imperative for enhanced cybersecurity measures and data privacy compliance is increasingly integrated into server design and operational protocols, reflecting a growing awareness of risk management in a highly interconnected digital ecosystem. This comprehensive evolution underscores the market's dynamic nature and its critical role in supporting the global digital economy.

- Rising adoption of AI and ML workloads.

- Increased demand for high-density and modular servers.

- Growth in hybrid cloud and multi-cloud strategies.

- Emergence of liquid cooling solutions for power efficiency.

- Focus on sustainable and energy-efficient data centre operations.

- Supply chain diversification and geopolitical considerations.

- Development of purpose-built servers for edge computing.

- Integration of advanced security features at the hardware level.

- Expansion of hyperscale data centres.

- Continued innovation in processor technologies (CPUs, GPUs, DPUs).

AI Impact Analysis on Data Centre Server

Artificial Intelligence (AI) is exerting a profound and multifaceted impact on the data centre server market, acting as a primary catalyst for innovation and growth. The computational intensity required for AI workloads, including machine learning training, inference, and complex data analytics, necessitates specialized server architectures equipped with powerful GPUs, AI accelerators, and high-bandwidth memory. This demand is driving a significant shift in server procurement, prioritizing performance and parallel processing capabilities over traditional CPU-centric designs. Consequently, server manufacturers are rapidly developing AI-optimized servers, leading to advancements in component technology, cooling solutions, and power management to accommodate the unprecedented power consumption and heat generation associated with AI operations. The continuous evolution of AI applications, from natural language processing to computer vision, ensures a sustained demand for increasingly sophisticated and efficient data centre server infrastructure.

- Increased demand for GPU-accelerated servers.

- Growth in specialized AI chip adoption.

- Requirement for high-bandwidth memory (HBM).

- Development of advanced cooling systems (e.g., liquid cooling).

- Optimization of server rack density for AI clusters.

- Shift towards more powerful power supply units (PSUs).

- Influence on server form factors and connectivity standards.

- Demand for AI-driven workload management and orchestration software.

- Acceleration of R&D in neuromorphic and quantum computing-ready servers.

Key Takeaways Data Centre Server Market Size & Forecast

- Global market size projected to reach USD 206.8 billion by 2033.

- Anticipated robust CAGR of 13.7% from 2025 to 2033.

- AI and cloud computing are primary growth drivers.

- North America and Asia Pacific lead market expansion.

- Sustainability and energy efficiency are critical investment areas.

- Hyperscale data centres significantly contribute to demand.

- Hardware innovation, especially in processors, remains crucial.

- Edge computing applications are opening new market segments.

- Cybersecurity integration in server design is intensifying.

- Market dynamics influenced by supply chain resilience and geopolitical factors.

Data Centre Server Market Drivers Analysis

The expansion of the data centre server market is propelled by a confluence of powerful drivers, each contributing significantly to the demand for enhanced computing infrastructure. The exponential growth of data generated globally, coupled with the increasing adoption of cloud computing across enterprises, necessitates robust and scalable server solutions. Furthermore, the pervasive trend of digital transformation initiatives across various industries, from manufacturing to healthcare, relies heavily on sophisticated server technology to support new digital services and operational efficiencies. The escalating demand for Artificial Intelligence and Machine Learning workloads, which require immense processing power, is a particularly potent driver, pushing innovation in server design and component capabilities. Additionally, the proliferation of IoT devices and the subsequent need for edge computing infrastructure further stimulate market growth by extending computing power closer to data sources.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Explosive Growth of Data and Digitalization | +3.5% | Global, particularly North America, Asia Pacific | Short-term to Long-term |

| Rising Adoption of Cloud Computing | +3.0% | Global, strong in developed economies | Short-term to Mid-term |

| Increasing Demand for AI and ML Workloads | +4.0% | Global, concentrated in tech hubs | Short-term to Long-term |

| Expansion of Edge Computing and IoT | +2.5% | Global, accelerating in smart cities and industrial sectors | Mid-term to Long-term |

| Emergence of 5G Technology | +0.7% | Global, especially in regions with 5G rollout | Mid-term |

Data Centre Server Market Restraints Analysis

Despite significant growth drivers, the data centre server market faces several formidable restraints that could impede its expansion. One primary concern is the substantial capital expenditure required for data centre infrastructure, including high-performance servers, which can be prohibitive for smaller enterprises or those with limited budgets. The escalating operational costs, particularly electricity consumption for cooling and powering servers, pose another significant challenge, especially as data centre density increases. Furthermore, the global supply chain vulnerabilities, including shortages of critical components like semiconductors, can disrupt manufacturing and delivery, leading to increased lead times and higher prices. Environmental regulations and the growing pressure for sustainable operations also add complexity, as data centres are major energy consumers and face scrutiny over their carbon footprint. Finally, the inherent complexity of managing and integrating diverse server architectures and software environments can create operational bottlenecks and require specialized expertise, potentially slowing down adoption for some organizations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital and Operational Costs | -2.0% | Global, more pronounced in emerging markets | Short-term to Mid-term |

| Supply Chain Disruptions and Component Shortages | -1.5% | Global, especially impacting manufacturing hubs | Short-term to Mid-term |

| Energy Consumption and Environmental Concerns | -1.0% | Global, driven by regulatory pressures in developed nations | Mid-term to Long-term |

| Data Security and Privacy Concerns | -0.5% | Global, particularly in highly regulated industries | Short-term |

| Technological Obsolescence and Upgrade Cycles | -0.7% | Global | Mid-term |

Data Centre Server Market Opportunities Analysis

The data centre server market is rife with significant opportunities stemming from evolving technological landscapes and increasing digital demands. The accelerating adoption of Artificial Intelligence, Machine Learning, and Big Data analytics across industries presents a vast opportunity for specialized, high-performance servers designed to handle intensive computational workloads. The ongoing expansion of cloud services, including private, public, and hybrid cloud models, continues to drive demand for scalable and flexible server infrastructure. Furthermore, the proliferation of 5G networks and the Internet of Things (IoT) is fueling the growth of edge computing, creating new market segments for compact, low-latency servers deployed closer to data sources. Opportunities also lie in the development of more sustainable and energy-efficient server technologies, responding to global environmental concerns and regulatory pressures. The trend towards hyperconverged infrastructure (HCI) and composable infrastructure also offers avenues for innovation, providing organizations with more agile and software-defined solutions for their computing needs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of AI and ML Applications | +4.5% | Global, particularly in North America, Asia Pacific | Short-term to Long-term |

| Growth of Edge Computing and 5G Deployments | +3.0% | Global, significant in smart cities, industrial IoT | Mid-term to Long-term |

| Demand for Sustainable and Energy-Efficient Solutions | +2.0% | Global, driven by regulations in Europe, North America | Mid-term to Long-term |

| Expansion of Hyperscale Data Centres | +1.5% | Global, concentrated in key cloud provider regions | Short-term to Mid-term |

| Development of Industry-Specific Server Solutions | +1.0% | Global, targeting healthcare, finance, manufacturing | Mid-term |

Data Centre Server Market Challenges Impact Analysis

The data centre server market faces significant challenges that demand innovative solutions and strategic foresight from industry participants. The escalating power consumption and cooling requirements of high-performance servers, particularly those optimized for AI workloads, present a substantial hurdle, pushing the limits of existing data centre infrastructure and increasing operational costs. Cybersecurity threats and data breaches remain a persistent and growing challenge, requiring continuous investment in robust hardware-level security features and advanced threat detection mechanisms. Furthermore, the rapid pace of technological advancements, while an opportunity, also creates a challenge of rapid obsolescence, compelling organizations to frequently upgrade their server infrastructure to maintain competitiveness and performance. The availability of skilled talent for managing complex data centre environments and specialized server technologies is another critical constraint. Lastly, geopolitical tensions and trade disputes can disrupt global supply chains, leading to component shortages and price volatility, complicating manufacturing and distribution processes.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Power Consumption and Cooling Demands | -1.8% | Global | Short-term to Long-term |

| Cybersecurity Threats and Data Privacy Compliance | -1.2% | Global, particularly in regulated industries | Short-term to Mid-term |

| Talent Shortage and Skill Gap in Data Centre Management | -0.9% | Global, prominent in developed economies | Mid-term to Long-term |

| High Investment in R&D for Next-Gen Technologies | -0.5% | Global, impacting key market players | Short-term |

| Geopolitical Risks and Trade Barriers | -0.8% | Global, impacting supply chains | Short-term |

Data Centre Server Market - Updated Report Scope

The comprehensive market research report on the Data Centre Server Market provides an in-depth analysis of market dynamics, growth trajectories, and key influencing factors across the historical, base, and forecast periods. It encapsulates critical insights into market sizing, growth rates, and a detailed breakdown of market segmentation by various parameters. The report further illuminates the competitive landscape by profiling leading market players, identifying emerging trends, and analyzing the impact of key drivers, restraints, opportunities, and challenges. Geographical analysis is integral, offering regional and country-level insights into market performance and strategic imperatives. This report serves as an indispensable resource for stakeholders seeking to understand market trends, make informed investment decisions, and formulate effective business strategies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 72.5 billion |

| Market Forecast in 2033 | USD 206.8 billion |

| Growth Rate | 13.7% from 2025 to 2033 |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Dell Technologies Hewlett Packard Enterprise Super Micro Computer Cisco Systems Lenovo Inspur IBM Huawei Fujitsu Quanta Computer Inventec Wiwynn GIGABYTE Technology Penguin Computing Advanced Micro Devices Intel Corporation NVIDIA Broadcom Marvell Technology Micron Technology |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Data Centre Server Market is meticulously segmented across various crucial dimensions, providing a granular view of its diverse landscape and enabling precise market analysis. These segmentations help in understanding specific market dynamics, technological preferences, and adoption patterns across different user groups and deployment models. Each segment reflects unique demand drivers and competitive intensities, offering detailed insights into market opportunities and challenges within specific niches. This comprehensive breakdown is essential for stakeholders looking to identify target markets, customize product offerings, and devise effective market entry or expansion strategies.

- By Server Type: This segment categorizes servers based on their form factor and design, catering to different space, cooling, and scalability needs within data centres.

- Rack Servers: Dominant for their high density and scalability within standard server racks.

- Blade Servers: Known for their modularity and efficiency in consolidating computing power.

- Tower Servers: Often used in smaller businesses or as standalone solutions due to their traditional PC-like form.

- Microservers: Energy-efficient, compact servers designed for scale-out workloads.

- Others: Includes specialized servers like hyperconverged and composable systems.

- By Component: This segmentation delves into the core hardware elements that constitute a data centre server, highlighting advancements and demand for critical processing, memory, and storage units.

- Processor (CPU, GPU, DPU, AI Accelerators): The central processing units, graphical processing units, data processing units, and dedicated AI accelerators that drive computational power.

- Memory (DDR, HBM): Volatile memory modules, including Double Data Rate (DDR) and High Bandwidth Memory (HBM), crucial for data access speed.

- Storage (HDD, SSD, NVMe): Non-volatile storage solutions ranging from traditional Hard Disk Drives to Solid State Drives and NVMe (Non-Volatile Memory Express) for high-speed storage.

- Power Supply Units: Components responsible for converting and regulating electrical power for server operation.

- Motherboards: The main circuit board connecting all components of a server.

- Networking Cards: Adapters facilitating network connectivity and data transfer.

- Chassis: The physical enclosure housing server components.

- By Deployment: This segment analyzes server adoption based on where the computing infrastructure is hosted and managed, reflecting different operational models and control levels.

- On-Premise: Servers deployed and managed directly within an organization's own facilities.

- Cloud: Servers accessed and managed over the internet, further categorized into:

- Public Cloud: Services offered by third-party providers over the public internet.

- Private Cloud: Dedicated cloud infrastructure used exclusively by a single organization.

- Hybrid Cloud: A combination of public and private cloud environments.

- By Enterprise Size: This segmentation categorizes the market based on the scale of businesses adopting data centre servers, indicating varying needs and budget considerations.

- Large Enterprises: Organizations with extensive IT infrastructure and significant data processing requirements.

- Small & Medium Enterprises (SMEs): Smaller businesses with growing digital needs and often seeking cost-effective, scalable solutions.

- By End-User: This segment examines the diverse industries utilizing data centre servers, showcasing how different sectors leverage these technologies for their specific operational and business objectives.

- BFSI (Banking, Financial Services, and Insurance): For transaction processing, fraud detection, and data analytics.

- IT & Telecom: For network infrastructure, cloud services, and data management.

- Healthcare: For electronic health records, medical imaging, and research.

- Government & Public Sector: For public services, defense, and national security.

- Manufacturing: For industrial automation, supply chain management, and smart factory initiatives.

- Retail: For e-commerce platforms, inventory management, and customer analytics.

- Media & Entertainment: For content creation, streaming services, and digital asset management.

- Others: Includes education, energy, and transportation sectors.

Regional Highlights

The global data centre server market exhibits distinct regional dynamics driven by varying levels of digital infrastructure development, cloud adoption, enterprise digitalization, and technological investment. Understanding these regional highlights is crucial for market participants to identify lucrative growth avenues and tailor their strategies to specific local requirements and opportunities.

- North America: This region consistently holds a dominant share in the data centre server market, primarily driven by the presence of a vast number of hyperscale cloud providers, leading technology companies, and early adoption of advanced computing technologies like AI and machine learning. The significant investment in digital transformation across various industries and robust government support for technological innovation further solidify its leading position. The demand here is characterized by a strong focus on high-performance computing, advanced cooling solutions, and sustainable data centre practices.

- Europe: Europe represents a mature and significant market, characterized by strong regulatory frameworks around data privacy (such as GDPR) and a growing emphasis on green IT initiatives. The region is witnessing substantial investments in cloud infrastructure, edge computing, and AI-driven data centres, particularly in countries like Germany, the UK, and France. Digitalization efforts across manufacturing, healthcare, and financial services sectors also contribute to sustained demand for data centre servers.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the data centre server market, fueled by rapid digitalization, increasing internet penetration, and the booming e-commerce and digital services sectors in countries like China, India, Japan, and South Korea. Government initiatives promoting local data centres, the influx of foreign direct investment in cloud infrastructure, and the massive scale of enterprise data generation are key drivers. The region presents immense opportunities due to its large population, expanding digital economy, and emerging tech hubs.

- Latin America: This region is experiencing steady growth, driven by increasing cloud adoption, digital transformation efforts across public and private sectors, and expanding internet connectivity. Countries like Brazil and Mexico are leading the charge in data centre investments, though the market remains sensitive to economic stability and infrastructure development. The demand is often for scalable, cost-effective solutions.

- Middle East and Africa (MEA): The MEA market is undergoing significant development, largely influenced by government-led digital transformation agendas, smart city initiatives, and diversification from traditional oil-based economies. Countries like the UAE and Saudi Arabia are investing heavily in hyperscale data centres and cloud regions to become regional digital hubs. While still emerging, the region shows strong potential for long-term growth as infrastructure development and connectivity improve.

Top Key Players:

The market research report covers the analysis of key stake holders of the Data Centre Server Market. Some of the leading players profiled in the report include -- Dell Technologies

- Hewlett Packard Enterprise

- Super Micro Computer

- Cisco Systems

- Lenovo

- Inspur

- IBM

- Huawei

- Fujitsu

- Quanta Computer

- Inventec

- Wiwynn

- GIGABYTE Technology

- Penguin Computing

- Advanced Micro Devices

- Intel Corporation

- NVIDIA

- Broadcom

- Marvell Technology

- Micron Technology

Frequently Asked Questions:

What is the current market size of the Data Centre Server Market?

The Data Centre Server Market was valued at USD 72.5 billion in 2025 and is projected to experience substantial growth over the forecast period.

What is the projected growth rate (CAGR) for the Data Centre Server Market?

The Data Centre Server Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.7% between 2025 and 2033, indicating robust expansion.

Which factors are primarily driving the growth of the Data Centre Server Market?

Key drivers include the explosive growth of data, increasing adoption of cloud computing services, the rising demand for AI and Machine Learning workloads, and the expansion of edge computing and IoT deployments.

What is the impact of Artificial Intelligence (AI) on the Data Centre Server Market?

AI significantly impacts the market by driving demand for high-performance servers equipped with GPUs and specialized AI accelerators, necessitating advancements in cooling, power management, and high-bandwidth memory to support intensive computational workloads.

Which region is expected to dominate the Data Centre Server Market?

North America is anticipated to continue dominating the Data Centre Server Market, driven by the strong presence of hyperscale cloud providers, advanced technology adoption, and significant investments in digital transformation initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted