Data Center Liquid Immersion Cooling Market

Data Center Liquid Immersion Cooling Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_677887 | Last Updated : July 18, 2025 |

Format : ![]()

![]()

![]()

![]()

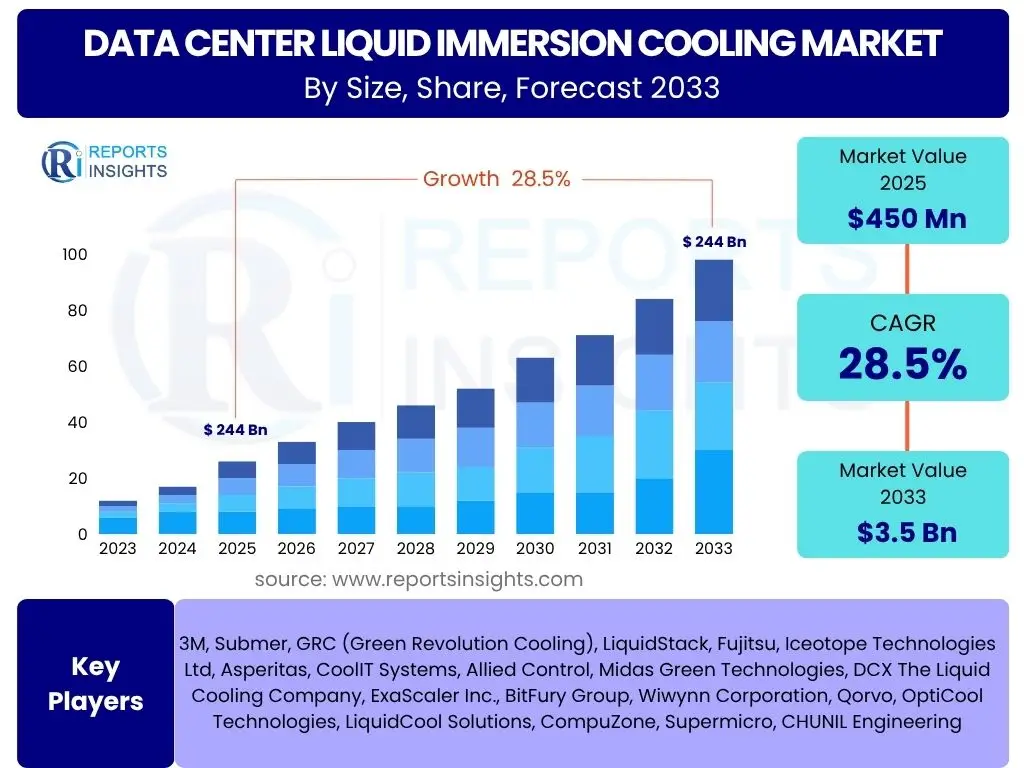

Data Center Liquid Immersion Cooling Market is projected to grow at a Compound annual growth rate (CAGR) of 28.5% between 2025 and 2033, valued at USD 550 million in 2025 and is projected to grow by USD 3.9 billion By 2033 the end of the forecast period.

Key Data Center Liquid Immersion Cooling Market Trends & Insights

The data center liquid immersion cooling market is experiencing a significant surge driven by the escalating demand for high-performance computing, particularly with the proliferation of artificial intelligence, machine learning, and advanced analytics workloads. This technology offers superior thermal management, addressing the limitations of traditional air-cooling systems in managing the intense heat generated by modern, densely packed server racks. The imperative for enhanced energy efficiency and reduced operational costs is further propelling its adoption, as immersion cooling significantly lowers power consumption associated with cooling infrastructure. Moreover, the growing focus on environmental sustainability and the push for greener data centers globally are positioning liquid immersion cooling as a critical solution, minimizing water usage and enabling heat reuse opportunities. This convergence of technological advancement, operational efficiency, and environmental responsibility is shaping the market's trajectory, making it an indispensable component for future data center designs.

- Rising power density of servers.

- Increased demand for energy efficiency and sustainability.

- Proliferation of AI, ML, and high-performance computing (HPC).

- Space optimization in data center design.

- Growing interest in waste heat recovery and circular economy principles.

- Advancements in dielectric fluids and cooling technologies.

- Shift towards modular and edge data center deployments.

AI Impact Analysis on Data Center Liquid Immersion Cooling

The transformative impact of artificial intelligence on the data center landscape is profound, making liquid immersion cooling not just an option, but an essential technology for future-proof infrastructure. AI workloads, characterized by their computational intensity and reliance on power-hungry GPUs, generate unprecedented levels of heat within server racks. Traditional air-cooling systems often struggle to efficiently dissipate this concentrated heat, leading to performance throttling and increased risk of hardware failure. Liquid immersion cooling, by directly submerging components in dielectric fluid, provides a much more effective heat transfer medium, enabling higher operational temperatures for servers and maintaining optimal performance for AI chips. This direct contact cooling not only enhances cooling efficiency but also allows for significantly higher power densities within server racks, enabling the deployment of more powerful AI clusters in smaller footprints. Consequently, the relentless demand for processing power fueled by AI development is directly accelerating the adoption and innovation within the liquid immersion cooling market, as organizations seek reliable, scalable, and energy-efficient solutions to power their intelligent operations.

- AI/ML drives demand for higher power density servers.

- Increased heat generation from GPU-intensive AI workloads.

- Need for enhanced cooling efficiency for AI hardware.

- Enables optimal performance and longevity of AI components.

- Facilitates compact and scalable AI data center designs.

Key Takeaways Data Center Liquid Immersion Cooling Market Size & Forecast

- The global Data Center Liquid Immersion Cooling Market is projected for substantial growth, reaching USD 3.9 billion by 2033.

- The market is expanding at an impressive CAGR of 28.5% from 2025 to 2033, reflecting rapid adoption.

- Growth is primarily driven by the need for enhanced energy efficiency, sustainability initiatives, and the proliferation of high-density computing.

- North America and Asia Pacific are anticipated to be leading regions due to technological advancements and rapid data center expansion.

- Key segments include Single Phase and Two Phase cooling solutions, addressing diverse data center requirements.

- Hyperscale data centers are significant adopters, alongside growing interest from small, medium, and edge data centers.

- The market is characterized by ongoing innovation in dielectric fluids, cooling systems, and infrastructure integration.

Data Center Liquid Immersion Cooling Market Drivers Impact Analysis

The global data center liquid immersion cooling market is experiencing robust growth, primarily propelled by several critical factors addressing the evolving demands of modern digital infrastructure. A significant driver is the escalating power density within data centers, as the continuous innovation in computing hardware leads to more powerful processors and GPUs packed into smaller footprints, generating unprecedented levels of heat that traditional air-cooling struggles to manage effectively. Concurrently, the imperative for greater energy efficiency and reduced operational costs is pushing data center operators towards immersion cooling, which significantly lowers cooling-related energy consumption compared to conventional methods. Furthermore, the rising global focus on environmental sustainability and carbon footprint reduction mandates more eco-friendly data center operations, where immersion cooling offers advantages like lower water usage and potential for waste heat reuse. The rapid expansion of high-performance computing (HPC), artificial intelligence (AI), and machine learning (ML) applications also necessitates superior thermal management, as these compute-intensive workloads require stable operating environments to maintain optimal performance and hardware longevity. These combined factors are creating a compelling case for the widespread adoption of liquid immersion cooling across various data center scales and types.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Server Power Density & Heat Generation | +6.5% | Global, particularly North America, Europe, APAC (Hyperscale & HPC) | Short to Mid-term |

| Growing Demand for Energy Efficiency and Sustainability | +5.8% | Europe (strict regulations), North America, APAC (growing awareness) | Mid to Long-term |

| Proliferation of AI, Machine Learning, and HPC Workloads | +7.2% | Global, especially US, China, UK, Germany, Canada | Short to Mid-term |

| Space Optimization & Compact Data Center Design | +4.0% | Urban centers globally, Edge Computing deployments | Mid-term |

| Rising Operational Costs of Traditional Cooling Systems | +5.0% | Global, highly impacted by energy prices | Short-term |

Data Center Liquid Immersion Cooling Market Restraints Impact Analysis

Despite its significant advantages, the data center liquid immersion cooling market faces several notable restraints that could temper its adoption rate. A primary hurdle is the relatively high initial capital expenditure associated with implementing immersion cooling solutions. This includes the cost of specialized tanks, dielectric fluids, and compatible server hardware, which can be considerably higher than traditional air-cooling infrastructure, posing a barrier for budget-conscious organizations or smaller data centers. Another significant restraint is the lack of standardized practices and industry-wide benchmarks. The absence of universal guidelines for fluid specifications, equipment compatibility, and deployment procedures can create uncertainty for potential adopters, slowing down widespread integration. Furthermore, there is a general unfamiliarity among data center operators and IT personnel with liquid immersion cooling technology, requiring specialized training and a shift in operational paradigms, which can be a slow process. Concerns regarding the long-term reliability and chemical compatibility of dielectric fluids with various server components also persist, although ongoing research and development are addressing these issues. Lastly, the perceived complexity of maintenance and potential for fluid leaks, while largely mitigated by modern systems, remains a psychological barrier for some decision-makers. Overcoming these restraints will be crucial for the market to realize its full growth potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -4.5% | Global, particularly SMEs & emerging markets | Short to Mid-term |

| Lack of Industry Standardization & Perceived Complexity | -3.8% | Global, impacting broad market adoption | Mid-term |

| Limited Awareness & Skill Gap among Operators | -2.0% | Global, especially traditional IT environments | Short to Mid-term |

| Concerns over Fluid Compatibility & Long-term Reliability | -2.5% | Global, particularly critical infrastructure operators | Mid-term |

Data Center Liquid Immersion Cooling Market Opportunities Impact Analysis

The data center liquid immersion cooling market is ripe with significant opportunities that promise to accelerate its growth and broader adoption. One of the most compelling opportunities lies in the expansion of edge computing, where localized data processing requires compact, efficient, and robust cooling solutions for environments with limited space and resources. Immersion cooling's ability to achieve high power densities in a small footprint makes it ideally suited for these deployments. Another key opportunity stems from the increasing adoption of renewable energy sources and the push for waste heat recovery. Immersion cooling systems can capture and reuse waste heat more efficiently than air-cooling, turning it into a valuable resource for district heating or other industrial applications, aligning with circular economy principles and enhancing energy independence. Furthermore, the continuous advancements in dielectric fluids and materials are improving performance, reducing costs, and expanding compatibility, making the technology more accessible and reliable for a wider range of applications. The growing focus on modular and containerized data centers also presents a substantial opportunity, as immersion cooling systems can be pre-integrated into these scalable units, facilitating rapid deployment and enhanced portability. As regulations around data center energy consumption and environmental impact become stricter, opportunities for government incentives and supportive policies are also emerging, further incentivizing the transition to more sustainable cooling technologies like immersion cooling. These opportunities collectively highlight a promising future for the market, driven by technological innovation and evolving industry needs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Edge Computing and Modular Data Centers | +6.0% | Global, especially emerging 5G and IoT markets | Mid to Long-term |

| Advancements in Dielectric Fluids and Materials | +5.5% | Global, R&D focused regions (North America, Europe, East Asia) | Short to Mid-term |

| Integration with Waste Heat Recovery Systems | +4.8% | Europe (strong sustainability push), countries with energy crises | Mid to Long-term |

| Government Incentives and Supportive Policies for Green Data Centers | +3.5% | Europe, North America, certain APAC countries | Mid-term |

Data Center Liquid Immersion Cooling Market Challenges Impact Analysis

Despite promising opportunities, the data center liquid immersion cooling market faces several critical challenges that stakeholders must address to ensure sustainable growth. One significant challenge is the ongoing need for substantial initial investment, which, while offering long-term operational savings, can still be a deterrent for organizations with limited capital budgets or those accustomed to traditional air-cooling infrastructure costs. This financial barrier necessitates innovative financing models and greater awareness of total cost of ownership (TCO) benefits. Another hurdle lies in regulatory complexities and the absence of widely adopted industry standards. While efforts are underway to standardize aspects of immersion cooling, a fragmented regulatory landscape across different regions can complicate deployment and create uncertainties for manufacturers and operators alike. Furthermore, integrating liquid immersion cooling solutions into existing data center infrastructures poses technical challenges, often requiring significant modifications to facilities, power distribution, and networking setups. This can lead to extended deployment times and increased complexities, particularly for retrofits. The perceived risk and psychological barriers among IT decision-makers also represent a challenge; concerns about fluid leaks, equipment compatibility, and the novelty of the technology can lead to cautious adoption. Finally, ensuring a robust and resilient supply chain for specialized components like tanks, pumps, heat exchangers, and dielectric fluids is crucial, as disruptions can impact deployment timelines. Overcoming these challenges will require collaborative efforts across the industry, focusing on education, standardization, and demonstrating clear economic and environmental advantages.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Perceived Economic Barrier | -3.0% | Global, particularly smaller enterprises and colocation providers | Short-term |

| Lack of Standardized Best Practices & Regulations | -2.2% | Global, affecting broad industry adoption | Mid-term |

| Integration Complexities with Existing Infrastructure | -1.8% | Global, especially for retrofit projects | Short to Mid-term |

| Supply Chain Limitations for Specialized Components | -1.5% | Global, sensitive to geopolitical and economic factors | Short-term |

Data Center Liquid Immersion Cooling Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Data Center Liquid Immersion Cooling Market, offering valuable insights into its current state, key trends, and future projections. It covers detailed market sizing, segmentation, regional analysis, and competitive landscape, enabling stakeholders to make informed strategic decisions. The report incorporates extensive primary and secondary research, including insights from industry experts, to provide a holistic view of market dynamics, growth drivers, restraints, opportunities, and challenges. It is designed to assist businesses, investors, and decision-makers in understanding the market's complexities and identifying potential growth avenues within the evolving data center cooling landscape.

| Report Attributes | Report Details |

|---|---|

| Report Name | Data Center Liquid Immersion Cooling Market |

| Market Size in 2025 | USD 550 million |

| Market Forecast in 2033 | USD 3.9 billion |

| Growth Rate | CAGR of 2025 to 2033 28.5% |

| Number of Pages | 275 |

| Key Companies Covered | Alfa lava AB, Asetek, CoolIT Systems, Inc, Green Data Center LLP, Green Revolution Cooling, Inc, Horizon Computing Solutions, Inc, IBM Co., Midas Green Technologies LLC, Rittal GmbH & Co., Schneider Electric SE, Fujitsu, Vertiv Co., Chilldyne Inc., Liquid Cool Solutions, Mitsubishi Electric Corporation, Submer |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis:

Market Product Type Segmentation:-- Single Phase Cooling

- Two Phase Cooling

- Small and Medium Data Centers

- Large Data Centers

- Hyper-Scale Data Centers

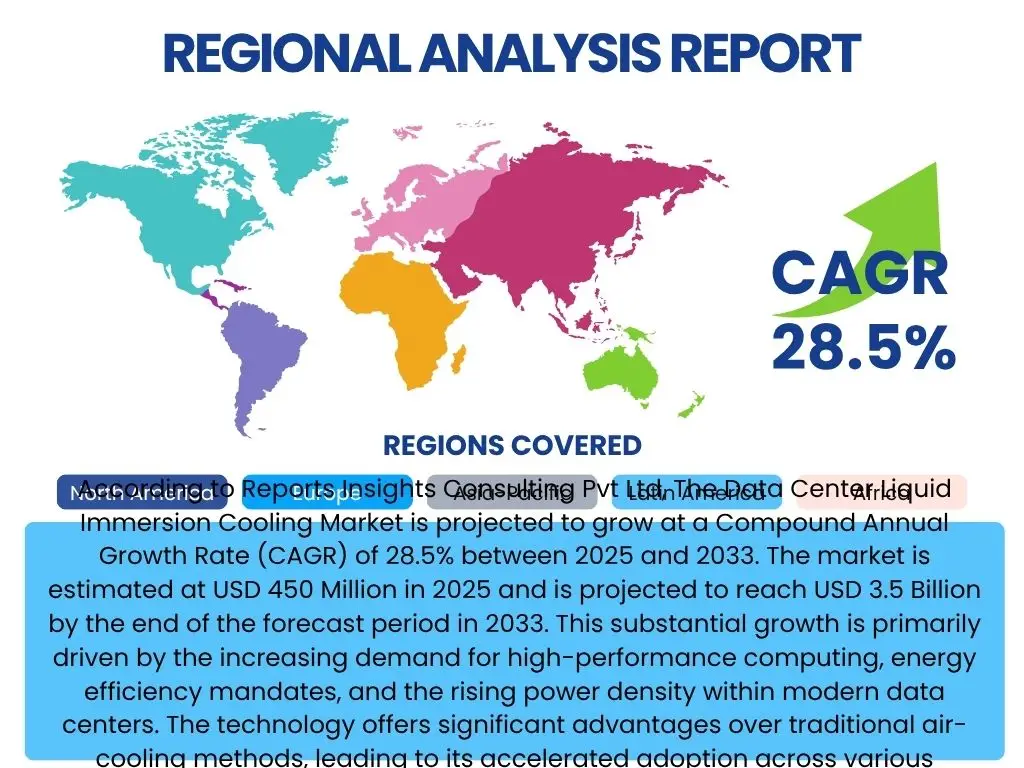

Regional Highlights

The global data center liquid immersion cooling market demonstrates varied adoption rates and growth trajectories across different regions, influenced by factors such as technological maturity, regulatory environments, energy costs, and the pace of digital transformation. Understanding these regional nuances is crucial for market stakeholders.

- North America: This region stands as a dominant force in the data center liquid immersion cooling market, primarily driven by the presence of a vast number of hyperscale data centers, major cloud service providers, and technology giants. The early adoption of advanced computing technologies, coupled with the rising demand for high-performance computing (HPC) and AI workloads, necessitates efficient cooling solutions. Additionally, increasing energy costs and a strong focus on energy efficiency initiatives contribute significantly to the market's growth here. The region benefits from robust research and development activities and a well-established infrastructure for innovation.

- Europe: Europe is rapidly emerging as a key region for immersion cooling, largely propelled by stringent environmental regulations and ambitious sustainability goals. Countries like Germany, the Netherlands, and the Nordics are at the forefront of promoting greener data center practices, including waste heat recovery and reduced water consumption, which are inherent advantages of immersion cooling. High electricity prices in many European nations also incentivize operators to seek out energy-efficient cooling solutions, making liquid immersion cooling an attractive option for reducing operational expenses and achieving carbon neutrality targets.

- Asia Pacific (APAC): The APAC region is poised for significant growth, fueled by rapid digital transformation, increasing internet penetration, and the booming demand for data center infrastructure, particularly in countries like China, India, Japan, and South Korea. The rapid expansion of hyperscale and colocation data centers to meet the demands of a burgeoning digital economy is driving the need for scalable and efficient cooling solutions. While initial adoption may be slower due to cost considerations, the long-term benefits of energy efficiency and the rising awareness about sustainable data center practices are expected to accelerate market growth in this dynamic region.

- Latin America: While a nascent market compared to other regions, Latin America is experiencing growing investment in data center infrastructure, driven by increasing digitalization and cloud adoption. Countries like Brazil and Mexico are leading the charge. As data centers expand and modernize, the demand for advanced cooling solutions, including liquid immersion cooling, is expected to grow. The region's focus on developing sustainable energy practices and improving energy efficiency will further support the adoption of this technology.

- Middle East and Africa (MEA): The MEA region presents emerging opportunities for the data center liquid immersion cooling market. Countries in the Middle East, particularly the UAE and Saudi Arabia, are investing heavily in digital infrastructure, smart city initiatives, and AI, leading to increased demand for high-density, efficient data centers. Africa's burgeoning digital economy and expanding connectivity are also fostering data center growth. As these regions face challenges such as high ambient temperatures and energy costs, liquid immersion cooling offers a viable and efficient solution for sustainable data center operations.

Top Key Players:

The market research report covers the analysis of key stake holders of the Data Center Liquid Immersion Cooling Market. Some of the leading players profiled in the report include -:- Alfa lava AB

- Asetek

- CoolIT Systems, Inc

- Green Data Center LLP

- Green Revolution Cooling, Inc

- Horizon Computing Solutions, Inc

- IBM Co.

- Midas Green Technologies LLC

- Rittal GmbH & Co.

- Schneider Electric SE

- Fujitsu

- Vertiv Co.

- Chilldyne Inc.

- Liquid Cool Solutions

- Mitsubishi Electric Corporation

- Submer

Frequently Asked Questions:

What is Data Center Liquid Immersion Cooling?

Data Center Liquid Immersion Cooling is an advanced thermal management technology where server components, or entire servers, are fully submerged in a non-conductive dielectric fluid. This fluid directly contacts the heat-generating components, providing superior heat transfer compared to traditional air-cooling methods. It effectively dissipates heat from high-density computing equipment, enabling higher efficiency and lower operational costs in data centers.

Why is Liquid Immersion Cooling gaining prominence in data centers?

Liquid immersion cooling is gaining prominence due to the escalating power density of modern servers, especially those used for AI, machine learning, and high-performance computing, which generate excessive heat. It offers significantly higher energy efficiency, reduced operational expenditure, and a smaller physical footprint compared to air-cooling. Additionally, its ability to enable waste heat recovery aligns with growing sustainability goals, making it an ideal solution for greener and more efficient data centers.

What are the primary benefits of using Liquid Immersion Cooling?

The primary benefits of liquid immersion cooling include enhanced energy efficiency, leading to significant reductions in power consumption and operational costs. It enables higher power densities within server racks, optimizing space utilization. Immersion cooling also provides superior thermal management for high-performance components, extending hardware lifespan and improving reliability. Furthermore, it offers significant environmental advantages through lower water usage and potential for waste heat reuse, contributing to data center sustainability.

What are the main types of Liquid Immersion Cooling systems?

The main types of liquid immersion cooling systems are Single-Phase Immersion Cooling and Two-Phase Immersion Cooling. In single-phase cooling, the dielectric fluid remains in a liquid state throughout the cooling process, circulating to transfer heat away. In two-phase cooling, the fluid boils at a low temperature, changing from liquid to vapor to absorb heat, and then condenses back to liquid, offering highly efficient heat transfer with minimal pumping required.

What is the market outlook for Data Center Liquid Immersion Cooling?

The market outlook for Data Center Liquid Immersion Cooling is highly positive, projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033, reaching USD 3.9 billion by 2033. This growth is driven by the increasing demand for high-performance computing, rising energy costs, sustainability mandates, and the continuous need for efficient thermal management in evolving data center architectures, including hyperscale, enterprise, and edge deployments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted