Data Center Accelerator Market

Data Center Accelerator Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707228 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Data Center Accelerator Market Size

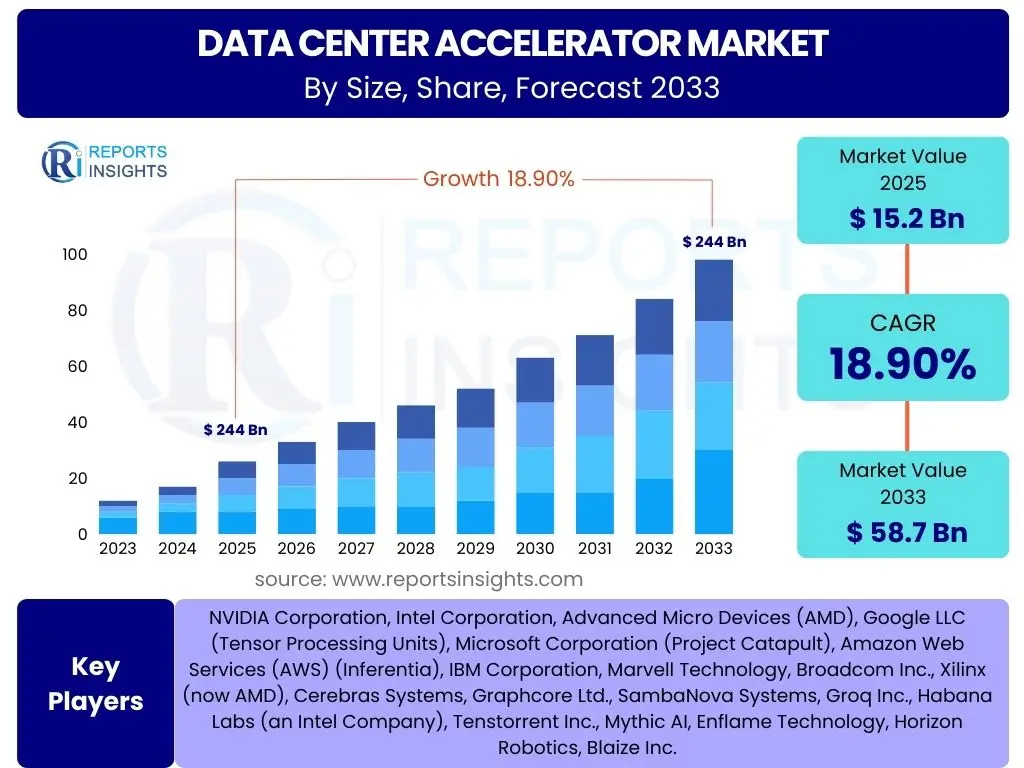

According to Reports Insights Consulting Pvt Ltd, The Data Center Accelerator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.9% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 58.7 Billion by the end of the forecast period in 2033.

Key Data Center Accelerator Market Trends & Insights

User queries regarding data center accelerator market trends frequently highlight the rapid evolution of computational demands, particularly driven by artificial intelligence and machine learning workloads. There is a strong interest in understanding how specialized hardware is transforming traditional data center architectures and enabling next-generation applications. Furthermore, concerns about energy efficiency, scalability, and the integration of diverse accelerator types are consistently raised, indicating a shift towards more heterogeneous and optimized computing environments.

The market is witnessing a significant trend towards the adoption of application-specific integrated circuits (ASICs) and field-programmable gate arrays (FPGAs) in addition to graphics processing units (GPUs), driven by the need for highly efficient processing of specific workloads like AI inference and big data analytics. Another notable trend is the increasing focus on software-defined infrastructure and open standards, allowing for greater flexibility and interoperability in deploying and managing accelerators across cloud and on-premise environments. The rise of edge computing also necessitates the deployment of smaller, more power-efficient accelerators closer to data sources, further fragmenting and diversifying the market landscape.

- Proliferation of AI/ML workloads demanding specialized processing power.

- Growing adoption of cloud computing and hyperscale data centers.

- Increased demand for high-performance computing (HPC) across various sectors.

- Emphasis on energy efficiency and sustainable data center operations.

- Emergence of edge computing architectures requiring distributed acceleration.

- Advancements in semiconductor technology leading to more powerful and efficient accelerators.

- Shift towards heterogeneous computing environments integrating various accelerator types.

- Rising investments in custom silicon development by major technology companies.

AI Impact Analysis on Data Center Accelerator

Common user questions regarding AI's impact on data center accelerators center on the specific hardware requirements for training and inference, the implications for data center power consumption and cooling, and the future evolution of AI-driven computing. Users seek to understand how AI is not just a consumer of accelerator technology but also a driver of innovation, shaping the design and capabilities of next-generation data center infrastructure. There is also significant curiosity about the economic benefits and operational efficiencies that AI-optimized accelerators can deliver.

Artificial intelligence is fundamentally reshaping the data center accelerator market by creating an insatiable demand for computational throughput and parallel processing capabilities. AI model training, especially for large language models and complex neural networks, requires immense computational resources, making GPUs, ASICs, and FPGAs indispensable. Beyond training, AI inference, which involves deploying trained models to make predictions or decisions, is driving the need for accelerators that offer high efficiency and low latency at scale. This dual demand for both training and inference hardware is accelerating research and development in specialized silicon, leading to the creation of highly optimized chips tailored for various AI workloads.

The profound impact of AI also extends to data center design and operations. The power density of accelerator-equipped servers is significantly higher, necessitating advanced cooling solutions and robust power delivery infrastructure. Furthermore, AI is fostering innovation in software stacks and programming models that can effectively utilize these powerful accelerators, enabling developers to build and deploy AI applications more efficiently. This symbiotic relationship ensures that as AI capabilities advance, so too will the underlying data center accelerator technologies, pushing the boundaries of what is computationally possible.

- Drives demand for high-performance GPUs, ASICs, and FPGAs for AI training and inference.

- Increases power density and cooling requirements within data centers.

- Accelerates development of specialized AI chips and architectures.

- Necessitates optimized software stacks and AI frameworks for efficient hardware utilization.

- Promotes the adoption of heterogeneous computing for diverse AI workloads.

- Enhances data center efficiency by offloading AI tasks from general-purpose CPUs.

- Influences infrastructure investment towards AI-ready data centers.

Key Takeaways Data Center Accelerator Market Size & Forecast

User queries about key takeaways from the Data Center Accelerator market size and forecast consistently focus on the market's aggressive growth trajectory, driven by the pervasive adoption of AI and cloud computing. There is a clear interest in identifying the primary drivers contributing to this expansion and understanding the long-term investment opportunities available. Users also seek concise summaries of how the market is evolving and what factors are most critical for future development and competitive advantage.

The data center accelerator market is poised for robust expansion, reflecting a fundamental shift in computing paradigms towards specialized hardware for data-intensive workloads. The forecast indicates sustained high growth rates, underscoring the increasing reliance on accelerated computing for applications ranging from artificial intelligence and machine learning to big data analytics and high-performance computing. This growth is not merely incremental but represents a transformative phase in data center infrastructure, where traditional CPU-centric architectures are augmented or replaced by more efficient, purpose-built accelerators. Understanding the nuances of this transition is crucial for stakeholders.

- Market projected for strong double-digit CAGR from 2025 to 2033.

- AI and Machine Learning adoption are primary growth catalysts.

- Significant investment opportunities in specialized hardware and related software.

- Cloud and hyperscale data centers are key adopters and drivers of market scale.

- Continued innovation in chip design and cooling technologies will sustain growth.

- Power efficiency and total cost of ownership (TCO) remain critical considerations for deployment.

Data Center Accelerator Market Drivers Analysis

The data center accelerator market is significantly driven by the escalating demand for high-performance computing capabilities across various industries. As businesses and research institutions increasingly rely on complex data processing, real-time analytics, and advanced simulations, general-purpose CPUs often fall short in delivering the required computational speed and efficiency. This inadequacy fuels the adoption of accelerators, which are specifically designed to offload and expedite these intensive workloads, leading to substantial performance gains and reduced processing times. The shift towards big data and analytics further amplifies this need, as organizations seek to derive actionable insights from massive datasets rapidly.

The pervasive integration of Artificial Intelligence (AI) and Machine Learning (ML) technologies across virtually every sector stands out as the most powerful driver for data center accelerators. AI models, particularly deep neural networks, require immense parallel processing power for both training and inference phases. Accelerators like GPUs, ASICs, and FPGAs are uniquely suited for these compute-intensive tasks, providing the necessary horsepower for developing and deploying sophisticated AI applications. As AI continues to evolve and become more complex, the demand for more powerful and efficient accelerators will only intensify, propelling market growth.

Furthermore, the continuous expansion of cloud computing and hyperscale data centers globally is a critical market driver. Cloud service providers are at the forefront of deploying accelerators to offer their clients high-performance, cost-effective computing resources for AI, HPC, and data analytics. Their massive infrastructure investments and rapid scaling capabilities create a substantial market for accelerator vendors. The ongoing digital transformation initiatives across enterprises, coupled with the increasing volume of data generated by IoT devices, further necessitate the adoption of accelerated computing to manage and process information efficiently, thus sustaining the market's upward trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Adoption of AI and Machine Learning Workloads | +5.5% | Global, particularly North America, APAC | Long-term (2025-2033) |

| Growing Demand for High-Performance Computing (HPC) | +3.0% | Global, particularly Europe, North America | Medium to Long-term (2025-2030) |

| Expansion of Cloud Computing and Hyperscale Data Centers | +4.2% | Global, particularly North America, APAC | Long-term (2025-2033) |

| Increasing Volume of Big Data and Analytics | +2.8% | Global | Medium-term (2025-2028) |

| Need for Energy Efficiency and Reduced Latency | +1.5% | Global | Long-term (2025-2033) |

Data Center Accelerator Market Restraints Analysis

Despite the robust growth prospects, the data center accelerator market faces significant restraints, primarily stemming from the high initial investment costs associated with acquiring and deploying advanced accelerator hardware. These specialized units, especially high-end GPUs and custom ASICs, can be considerably more expensive than traditional CPUs. For many enterprises, particularly small and medium-sized businesses (SMBs), the capital expenditure required to upgrade existing infrastructure or build new accelerator-optimized data centers can be prohibitive, acting as a barrier to widespread adoption. This cost factor often necessitates a careful return on investment (ROI) analysis, which can delay or deter implementation.

Another key restraint is the complexity involved in integrating these accelerators into existing data center environments and developing or adapting software to effectively utilize their capabilities. Deploying accelerators requires specialized expertise in hardware configuration, system integration, and programming for parallel architectures. The scarcity of skilled professionals capable of designing, managing, and optimizing accelerator-driven workloads poses a significant challenge. Furthermore, the lack of standardized programming interfaces and ecosystems across different accelerator types can lead to vendor lock-in and complicate multi-vendor deployments, increasing development effort and operational overhead.

Moreover, concerns related to power consumption and thermal management present ongoing challenges. Accelerators, while highly efficient for specific workloads, often consume substantial amounts of power and generate considerable heat, especially in dense configurations. This necessitates significant investments in advanced cooling systems and robust power delivery infrastructure, further increasing operational expenses (OpEx). While manufacturers are striving for more power-efficient designs, the exponential growth in computational demand from AI and HPC applications often outpaces these efficiency gains, making power and thermal management a persistent restraint for widespread and cost-effective deployment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Total Cost of Ownership (TCO) | -2.0% | Global, particularly Emerging Markets | Long-term (2025-2033) |

| Complexity of Integration and Programming | -1.5% | Global | Medium-term (2025-2029) |

| Significant Power Consumption and Thermal Management Challenges | -1.0% | Global, particularly High-Density Data Centers | Long-term (2025-2033) |

| Lack of Skilled Workforce and Expertise | -0.8% | Global | Long-term (2025-2033) |

| Supply Chain Disruptions and Component Shortages | -0.5% | Global | Short-term (2025-2026) |

Data Center Accelerator Market Opportunities Analysis

The burgeoning field of edge computing presents a significant opportunity for the data center accelerator market. As more data is generated and processed closer to its source, there is an increasing need for compact, power-efficient, and high-performance accelerators at the edge. These edge accelerators can enable real-time AI inference for applications like autonomous vehicles, industrial IoT, and smart cities, where latency is critical. Developing specialized accelerator solutions tailored for resource-constrained edge environments, focusing on low power consumption and robust performance, will unlock a vast, untapped market segment and diversify revenue streams for accelerator manufacturers.

Another substantial opportunity lies in the continuous innovation of custom silicon and domain-specific architectures. While GPUs remain dominant, the trend towards ASICs and FPGAs designed for specific workloads (e.g., AI training, video transcoding, genomic sequencing) is gaining momentum. Companies that can design and produce highly optimized, energy-efficient custom accelerators for niche or emerging applications will gain a competitive advantage. Furthermore, the development of open-source hardware architectures and software ecosystems around accelerators could foster greater adoption and innovation by reducing barriers to entry and promoting interoperability, creating new collaborative opportunities.

The growing emphasis on sustainability and energy efficiency in data centers also opens up opportunities for accelerator vendors. Accelerators, when properly optimized, can offer significantly better performance per watt compared to general-purpose CPUs for specific workloads. Developing and marketing highly energy-efficient accelerator solutions that help data centers reduce their carbon footprint and operational costs will be a compelling value proposition. Additionally, the integration of accelerators with other emerging technologies like quantum computing and advanced networking (e.g., CXL) could create new hybrid computing paradigms, expanding the scope and utility of data center accelerators well beyond current applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Edge Computing and AI at the Edge | +3.5% | Global | Long-term (2026-2033) |

| Advancements in Custom Silicon and Domain-Specific Architectures (DSA) | +2.8% | Global, particularly North America, APAC | Long-term (2025-2033) |

| Increasing Focus on Sustainable and Energy-Efficient Computing | +1.8% | Global, particularly Europe | Long-term (2025-2033) |

| Emergence of Hybrid Cloud and Multi-Cloud Environments | +1.2% | Global | Medium-term (2025-2029) |

| Demand for Accelerated Databases and Data Warehousing | +0.9% | Global | Medium-term (2025-2030) |

Data Center Accelerator Market Challenges Impact Analysis

The rapid pace of technological innovation in the semiconductor industry poses a significant challenge for the data center accelerator market. New accelerator architectures and technologies are introduced frequently, leading to a quick obsolescence cycle for existing hardware. This rapid evolution means that data center operators must constantly invest in upgrades to maintain competitive performance, which can be financially burdensome. Furthermore, supporting diverse and rapidly changing hardware platforms requires significant engineering effort in terms of software development, driver compatibility, and system integration, adding complexity and cost to deployments.

Thermal management and power density remain critical operational challenges for data center accelerators. As accelerators become more powerful, their heat generation increases substantially, necessitating advanced and often expensive cooling solutions such as liquid cooling or direct-to-chip cooling systems. The high power draw of these systems also strains existing data center power infrastructure, requiring upgrades that can be complex and costly. Effectively managing heat dissipation and ensuring reliable power delivery at scale are essential for maximizing accelerator performance and lifespan, but these factors represent ongoing hurdles for widespread and cost-effective deployment, especially for smaller or older data centers.

The scarcity of a highly skilled workforce capable of deploying, optimizing, and managing data center accelerators presents another substantial challenge. The specialized knowledge required for programming and fine-tuning these complex systems, often involving deep understanding of parallel computing, AI frameworks, and low-level hardware interactions, is in high demand and short supply. This talent gap can hinder the efficient adoption and utilization of accelerators, leading to suboptimal performance, increased operational costs, and delayed project timelines. Bridging this skill gap through training programs and simplified development environments is crucial for the sustained growth of the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Upgrade Cycles | -1.5% | Global | Long-term (2025-2033) |

| Escalating Power Consumption and Thermal Management | -1.2% | Global, particularly High-Density Data Centers | Long-term (2025-2033) |

| Shortage of Skilled Professionals and Expertise | -0.9% | Global | Long-term (2025-2033) |

| Interoperability Issues and Lack of Standardization | -0.7% | Global | Medium-term (2025-2029) |

| Regulatory and Compliance Requirements | -0.4% | Regional (e.g., EU, China) | Long-term (2025-2033) |

Data Center Accelerator Market - Updated Report Scope

This report provides a comprehensive analysis of the global Data Center Accelerator market, covering market sizing, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. It delves into the impact of emerging technologies like AI and edge computing, offers detailed segmentation analysis by component, type, application, and end-user, and highlights regional market dynamics. The scope includes an assessment of competitive landscape and profiles of key market participants, aiming to deliver actionable insights for stakeholders seeking to navigate this evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 58.7 Billion |

| Growth Rate | 18.9% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | NVIDIA Corporation, Intel Corporation, Advanced Micro Devices (AMD), Google LLC (Tensor Processing Units), Microsoft Corporation (Project Catapult), Amazon Web Services (AWS) (Inferentia), IBM Corporation, Marvell Technology, Broadcom Inc., Xilinx (now AMD), Cerebras Systems, Graphcore Ltd., SambaNova Systems, Groq Inc., Habana Labs (an Intel Company), Tenstorrent Inc., Mythic AI, Enflame Technology, Horizon Robotics, Blaize Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Data Center Accelerator market is segmented across several dimensions to provide a granular view of its structure and dynamics. These segments allow for a detailed understanding of technology adoption patterns, application areas, and end-user preferences, which are crucial for strategic planning and investment decisions. Each segment plays a distinct role in shaping the market's growth trajectory and addressing specific computational demands.

Segmentation by component distinguishes between the physical hardware (such as GPUs, FPGAs, ASICs, CPU Accelerators, and other specialized processors) and the enabling software (including APIs, SDKs, libraries, and frameworks) essential for programming and managing these accelerators. Hardware forms the foundational layer, while software dictates usability and application efficiency. The 'By Type' segmentation categorizes accelerators based on their primary function, such as HPC accelerators for scientific simulations, AI/ML accelerators for deep learning, NPUs for network optimization, DPUs for data processing, VPUs for video, and storage accelerators for I/O intensive tasks.

Application-based segmentation highlights the diverse use cases, ranging from deep learning training and inference to high-performance computing, enterprise applications, cloud services, data analytics, virtualization, and gaming. This provides insights into which sectors are driving demand for specific accelerator types. Finally, the end-user segmentation classifies market adoption by various industry verticals, including cloud service providers, enterprise data centers, research institutions, government, telecommunications, healthcare, and financial services, reflecting the broad applicability and varied requirements of accelerated computing across different organizational types.

- By Component:

- Hardware (GPU, FPGA, ASIC, CPU Accelerator, Other Processors)

- Software (API, SDK, Libraries, Frameworks)

- By Type:

- High-Performance Computing (HPC) Accelerator

- AI/Machine Learning Accelerator

- Network Processing Unit (NPU)

- Data Processing Unit (DPU)

- Video Processing Unit (VPU)

- Storage Accelerator

- By Application:

- Deep Learning Training

- Deep Learning Inference

- High-Performance Computing

- Enterprise Applications

- Cloud & Web Services

- Data Analytics

- Virtualization

- Gaming

- By End-User:

- Cloud Service Providers (CSPs)

- Enterprise Data Centers

- Research & Academia

- Government & Defense

- Telecommunications

- Healthcare & Life Sciences

- Financial Services

Regional Highlights

- North America: Dominant market share attributed to the presence of major cloud service providers, leading AI research institutions, and early adoption of advanced computing technologies. High investments in data center infrastructure and a strong focus on enterprise digital transformation continue to drive demand.

- Asia Pacific (APAC): Fastest-growing region, fueled by rapid expansion of data centers in China, India, Japan, and South Korea, coupled with significant government initiatives for AI development and smart cities. Growing adoption of cloud services and increasing enterprise investments contribute to accelerated market growth.

- Europe: Stable growth driven by increasing investments in HPC for scientific research, stricter data privacy regulations promoting localized data processing, and growing enterprise adoption of AI. Germany, the UK, and France are key contributors, focusing on energy-efficient solutions and sustainability.

- Latin America: Emerging market with growing cloud adoption and increasing digital transformation efforts across industries. Brazil and Mexico are leading the adoption, driven by rising internet penetration and local data processing needs.

- Middle East and Africa (MEA): Gradual adoption supported by smart city initiatives, government investments in digital infrastructure, and diversification of economies beyond oil. UAE and Saudi Arabia are key countries driving initial deployments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Data Center Accelerator Market.- NVIDIA Corporation

- Intel Corporation

- Advanced Micro Devices (AMD)

- Google LLC (Tensor Processing Units)

- Microsoft Corporation (Project Catapult)

- Amazon Web Services (AWS) (Inferentia)

- IBM Corporation

- Marvell Technology

- Broadcom Inc.

- Xilinx (now AMD)

- Cerebras Systems

- Graphcore Ltd.

- SambaNova Systems

- Groq Inc.

- Habana Labs (an Intel Company)

- Tenstorrent Inc.

- Mythic AI

- Enflame Technology

- Horizon Robotics

- Blaize Inc.

Frequently Asked Questions

What is a Data Center Accelerator?

A data center accelerator is a specialized hardware component designed to offload and speed up specific, compute-intensive workloads that general-purpose CPUs handle inefficiently. These workloads often include artificial intelligence (AI) training and inference, high-performance computing (HPC), big data analytics, and real-time data processing, significantly enhancing performance and energy efficiency within data centers.

What are the primary types of Data Center Accelerators?

The primary types of data center accelerators include Graphics Processing Units (GPUs), Field-Programmable Gate Arrays (FPGAs), Application-Specific Integrated Circuits (ASICs), Network Processing Units (NPUs), Data Processing Units (DPUs), Video Processing Units (VPUs), and CPU Accelerators. Each type is optimized for different computational tasks, offering varying levels of flexibility and performance efficiency.

How is AI impacting the Data Center Accelerator market?

AI is a major driver, creating immense demand for high-performance accelerators for both AI model training (requiring extensive parallel processing) and inference (requiring efficient, low-latency execution). This has led to rapid innovation in specialized AI chips (ASICs), increased power density in data centers, and a focus on software-hardware co-optimization for AI workloads.

What are the key drivers for Data Center Accelerator market growth?

Key drivers include the surging adoption of AI and Machine Learning workloads, the increasing demand for High-Performance Computing (HPC) across various sectors, the continuous expansion of cloud computing and hyperscale data centers, and the growing volume of big data requiring rapid analysis. The pursuit of energy efficiency also drives adoption.

What challenges does the Data Center Accelerator market face?

Challenges include high initial investment costs and total cost of ownership, the complexity of integrating accelerators into existing infrastructure, significant power consumption and thermal management issues, rapid technological obsolescence necessitating frequent upgrades, and a shortage of skilled professionals capable of managing these advanced systems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted