Computer Recycling Market

Computer Recycling Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701541 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

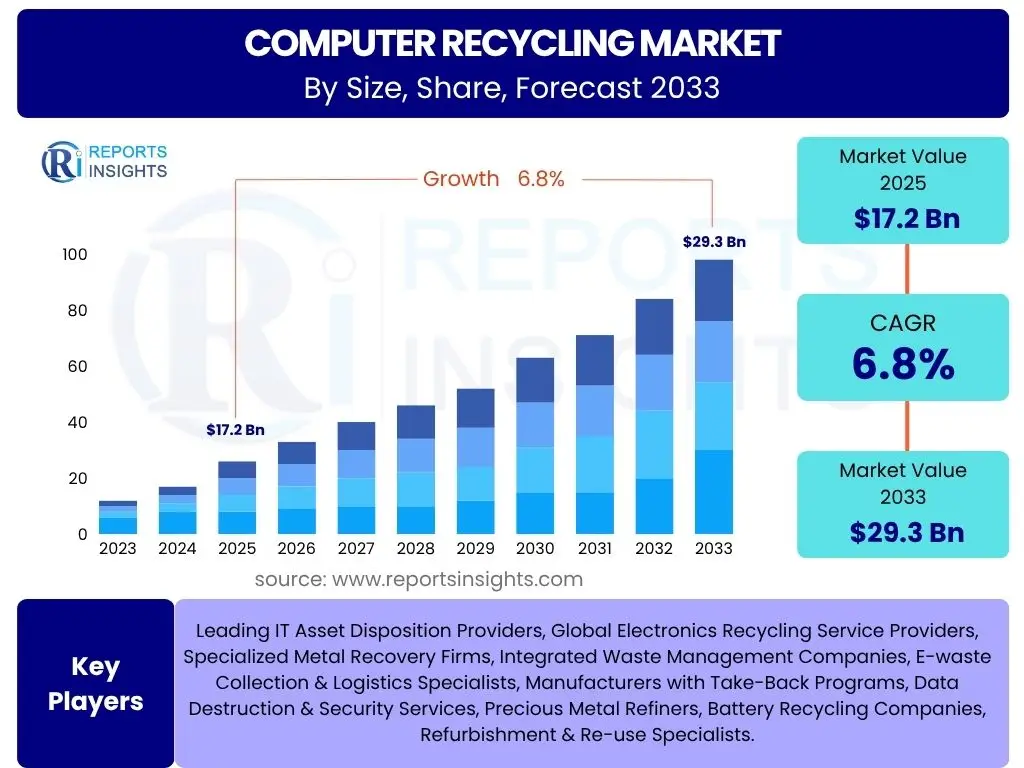

Computer Recycling Market Size

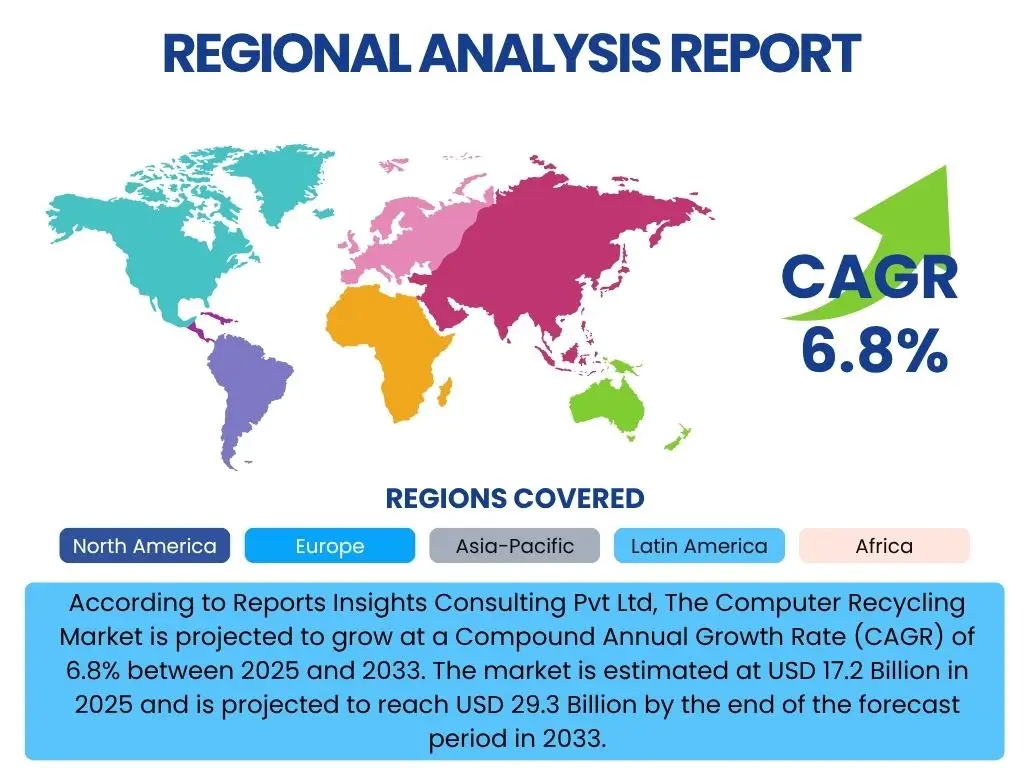

According to Reports Insights Consulting Pvt Ltd, The Computer Recycling Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 17.2 Billion in 2025 and is projected to reach USD 29.3 Billion by the end of the forecast period in 2033.

Key Computer Recycling Market Trends & Insights

User inquiries frequently highlight the evolving landscape of computer recycling, with a strong emphasis on technological advancements and policy shifts. A prevalent theme is the increasing demand for sustainable practices and circular economy principles, which are reshaping industry operations from collection to material recovery. Users are keen to understand how innovations in processing technologies and the integration of digital solutions are improving efficiency and material yields.

Another significant area of interest revolves around regulatory frameworks and corporate social responsibility. There is a clear user desire to comprehend the impact of stricter e-waste legislation globally and how businesses are adapting through enhanced take-back schemes and certified recycling programs. The convergence of environmental mandates with corporate sustainability goals is seen as a key driver for market transformation, pushing for more transparent and accountable recycling processes.

Furthermore, questions often arise regarding the recovery of critical raw materials and data security concerns. The growing value of precious metals and rare earth elements within electronic waste is driving innovation in urban mining techniques. Simultaneously, the imperative for secure data destruction during computer recycling remains a top priority for both businesses and individual consumers, influencing the choice of recycling service providers and the development of secure IT Asset Disposition (ITAD) solutions.

- Growing adoption of circular economy models and Extended Producer Responsibility (EPR) schemes.

- Increased demand for secure data destruction and IT Asset Disposition (ITAD) services.

- Advancements in automated sorting and material recovery technologies.

- Focus on critical raw material recovery from discarded electronics.

- Rising consumer and corporate awareness regarding e-waste hazards.

AI Impact Analysis on Computer Recycling

Common user questions regarding AI's influence on computer recycling often center on its potential to revolutionize efficiency, accuracy, and material recovery rates. Users are eager to understand how AI can streamline the complex processes involved in e-waste management, from initial sorting and identification of components to optimizing logistics. There is significant interest in AI's role in overcoming current manual limitations and enhancing the economic viability of recycling operations.

Concerns also emerge around the practical implementation of AI, including the initial investment costs, the need for specialized technical expertise, and the potential for job displacement in traditional recycling roles. However, the overarching expectation is that AI will act as an accelerant for the industry, enabling more sophisticated and sustainable practices. Users anticipate AI will provide unprecedented insights into waste streams, allowing for more targeted and efficient resource recovery.

Ultimately, the consensus among user queries points to AI as a transformative force in computer recycling. Its capabilities in machine vision, predictive analytics, and robotic automation are viewed as critical for addressing the escalating volume and complexity of electronic waste. The ability of AI to learn and adapt to diverse material compositions and changing regulations is perceived as a significant advantage for future recycling endeavors, promising higher recovery yields and reduced environmental impact.

- Enhanced material identification and sorting through AI-powered vision systems and robotics.

- Optimization of logistics and collection routes using predictive analytics.

- Improved efficiency in dismantling and component separation processes.

- Predictive maintenance for recycling machinery, reducing downtime.

- Development of smart recycling facilities with autonomous operations.

Key Takeaways Computer Recycling Market Size & Forecast

User queries about the key takeaways from the Computer Recycling market size and forecast consistently highlight the significant growth trajectory and the underlying drivers. There is a strong interest in understanding the primary factors contributing to this expansion, particularly the interplay of stringent environmental regulations, increasing corporate sustainability mandates, and the escalating volume of electronic waste globally. The market's upward trend is seen as a direct reflection of a growing societal and industrial commitment to responsible e-waste management.

Another prominent theme in user questions concerns the strategic opportunities within this expanding market. Users are keen to identify segments or regions that are poised for substantial growth, such as advanced material recovery technologies, secure IT Asset Disposition (ITAD) services, and innovative collection schemes. The forecast suggests that investments in R&D for more efficient and environmentally sound recycling processes will yield significant returns, addressing both resource scarcity and pollution concerns.

Furthermore, discussions frequently touch upon the critical role of stakeholder collaboration. The projected market growth underscores the necessity for synchronized efforts from governments, electronics manufacturers, recycling service providers, and consumers. The long-term outlook for the computer recycling market is overwhelmingly positive, driven by a global shift towards circular economy models and the imperative to extract maximum value from end-of-life electronic devices while minimizing their ecological footprint.

- Substantial market growth is driven by regulatory pressures and environmental consciousness.

- Increasing volume of e-waste necessitates robust recycling infrastructure development.

- Technological advancements in recycling processes are key to unlocking market potential.

- Strong emphasis on secure data destruction and resource recovery drives service demand.

- Investment in circular economy initiatives will significantly contribute to market expansion.

Computer Recycling Market Drivers Analysis

The computer recycling market is significantly propelled by an confluence of regulatory imperatives, escalating volumes of electronic waste, and a growing global awareness of environmental sustainability. Governments worldwide are enacting and enforcing stricter e-waste legislation, mandating responsible disposal and recycling practices for electronic devices. These regulations, often underpinned by Extended Producer Responsibility (EPR) schemes, place the onus on manufacturers to manage the end-of-life cycle of their products, thereby fostering a structured and compliant recycling ecosystem. This regulatory push creates a consistent demand for professional recycling services, ensuring that a greater proportion of discarded computers are channeled into formal recycling streams rather than ending up in landfills.

Beyond legislative frameworks, the sheer proliferation of electronic devices and their rapid obsolescence contribute massively to the volume of e-waste generated annually. As technology advances and consumer upgrade cycles shorten, an ever-increasing quantity of old computers, laptops, and peripherals enter the waste stream. This continuous influx of discarded hardware directly fuels the need for efficient recycling solutions, from collection and sorting to material recovery. The challenge of managing this growing waste stream has transformed into an economic opportunity for the recycling industry, driving innovation in processing techniques and business models to handle diverse and complex electronic components.

Furthermore, a heightened global awareness regarding the environmental hazards of improper e-waste disposal, coupled with a focus on resource conservation and the circular economy, is a powerful driver. Both corporate entities and individual consumers are increasingly prioritizing sustainable practices, opting for certified recycling services to ensure data security and environmental compliance. The recognition of e-waste as a valuable source of secondary raw materials, including precious metals and rare earth elements, further incentivizes recycling efforts, reducing reliance on virgin materials and mitigating mining-related environmental impacts. This shift in perception from waste to resource is fundamentally altering market dynamics, embedding recycling as an integral part of the product lifecycle.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent E-Waste Regulations & EPR Schemes | +1.8% | Europe, North America, Asia Pacific (China, India) | Short to Medium-term (2025-2029) |

| Increasing Volume of End-of-Life Electronic Devices | +1.5% | Global, particularly high-consumption regions | Medium to Long-term (2026-2033) |

| Growing Corporate Sustainability & Circular Economy Initiatives | +1.2% | North America, Europe, Developed Asia Pacific | Short to Medium-term (2025-2030) |

| Rising Awareness of Resource Scarcity & Urban Mining Potential | +1.0% | Global, especially resource-dependent economies | Medium to Long-term (2027-2033) |

Computer Recycling Market Restraints Analysis

Despite significant growth drivers, the computer recycling market faces several formidable restraints that can impede its full potential. One primary challenge is the logistical complexity and high cost associated with the collection, transportation, and processing of e-waste. Electronic devices are often bulky, contain hazardous materials, and require specialized handling, making collection from disparate sources inefficient and expensive. Furthermore, the dismantling and separation of various components, especially for complex devices like computers, demand labor-intensive processes or advanced, costly machinery, which can deter smaller players and reduce profit margins for recyclers.

Another significant restraint stems from the informal recycling sector, particularly prevalent in developing regions. While offering a seemingly low-cost solution, these unregulated operations often employ crude and environmentally damaging practices, leading to severe pollution and health hazards. The existence of a robust informal sector not only undermines formal recycling efforts by siphoning off valuable materials but also makes it challenging to enforce environmental regulations and ensure safe disposal. This competition from uncertified recyclers can depress prices for recovered materials, making formal, compliant operations less financially attractive.

Moreover, the design complexity of modern electronic devices presents a substantial hurdle. Products are increasingly designed with integrated components, proprietary fasteners, and glued-together assemblies, making them difficult and costly to disassemble for material recovery. This "design for obsolescence" rather than "design for recyclability" impacts the efficiency and economic viability of recycling processes. Coupled with the issue of low consumer participation rates in formal recycling programs due to a lack of awareness, inconvenience, or concerns about data security, these factors collectively limit the volume of e-waste entering legitimate recycling channels, thereby restricting market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Collection & Processing Costs | -1.3% | Global | Short to Medium-term (2025-2030) |

| Presence of Informal Recycling Sector | -1.0% | Asia Pacific, Latin America, Africa | Medium to Long-term (2026-2033) |

| Complex Product Design & Material Mix | -0.8% | Global | Short to Medium-term (2025-2029) |

| Low Consumer Awareness & Participation Rates | -0.7% | Global, particularly emerging economies | Short to Medium-term (2025-2030) |

Computer Recycling Market Opportunities Analysis

The computer recycling market is poised for significant growth, presenting numerous opportunities driven by technological innovation and evolving market demands. One major avenue lies in the advancement of material recovery technologies, particularly in the realm of urban mining. With the increasing value of critical raw materials like gold, silver, palladium, and rare earth elements embedded in electronic waste, there is a substantial opportunity for companies investing in cutting-edge separation, refining, and extraction techniques. Innovations in robotics, artificial intelligence, and specialized chemical processes can significantly enhance the efficiency and purity of material recovery, making the recycling process more economically viable and environmentally beneficial.

Another promising opportunity lies within the expansion of IT Asset Disposition (ITAD) services, particularly for corporate and governmental clients. As organizations replace their IT infrastructure more frequently, the demand for secure and compliant disposal of sensitive data remains paramount. Companies that can offer comprehensive, certified ITAD services, including data sanitization, asset remarketing, and environmentally responsible recycling, stand to capture a significant share of this high-value segment. The increasing focus on cybersecurity and data privacy regulations further reinforces this opportunity, positioning secure ITAD providers as indispensable partners for businesses aiming to manage their end-of-life IT assets responsibly.

Furthermore, the development of robust reverse logistics and collection infrastructure, especially in underserved regions, represents a key growth area. Many areas still lack efficient systems for collecting and transporting e-waste from consumers and businesses to recycling facilities. Investing in innovative collection models, such as convenient drop-off points, take-back programs, or incentivized collection schemes, can significantly increase the volume of e-waste entering formal recycling channels. Additionally, fostering partnerships between electronics manufacturers, retailers, and recycling companies can create more streamlined and accessible recycling pathways, unlocking untapped e-waste streams and expanding market reach. This focus on infrastructure development is crucial for realizing the full potential of the circular economy for electronics.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Urban Mining & Material Recovery Technologies | +1.6% | Global, particularly developed economies | Medium to Long-term (2027-2033) |

| Expansion of Secure IT Asset Disposition (ITAD) Services | +1.4% | North America, Europe, Developed Asia Pacific | Short to Medium-term (2025-2030) |

| Development of Robust Reverse Logistics & Collection Infrastructure | +1.1% | Emerging Economies (Asia Pacific, Latin America, Africa) | Medium to Long-term (2026-2033) |

| Growing Demand for Refurbished Components & Remarketing | +0.9% | Global | Short to Medium-term (2025-2030) |

Computer Recycling Market Challenges Impact Analysis

The computer recycling market, despite its growth potential, is confronted by several complex challenges that demand innovative solutions. One significant hurdle is the constantly evolving complexity of electronic products and their material composition. Modern computers integrate a diverse array of materials, including plastics, metals, glass, and hazardous substances, often in intricate designs that make manual or mechanical disassembly difficult and inefficient. The presence of these hazardous materials, such as lead, mercury, and cadmium, also necessitates specialized handling and disposal protocols, significantly increasing processing costs and posing environmental and health risks if not managed properly. This inherent complexity makes comprehensive material recovery a technical and economic challenge.

Another substantial challenge is ensuring complete data security during the recycling process. For businesses and individuals, the protection of sensitive information stored on hard drives and other memory components is paramount. Any breach of data during disposal can lead to severe financial and reputational damages. While specialized data sanitization services exist, the risk of data remnants, coupled with the need for verifiable destruction, creates a trust barrier for some potential recyclers. This challenge underscores the critical need for certified and transparent data destruction processes, adding a layer of complexity and cost to the overall recycling operation and requiring stringent adherence to data privacy regulations like GDPR and CCPA.

Furthermore, managing the informal e-waste sector, particularly in developing countries, presents a persistent challenge. These informal operations often lack proper environmental controls and worker safety measures, leading to significant pollution and health issues. They also divert valuable materials from formal recycling channels, impacting the economic viability of certified recyclers. Overcoming this involves not only stricter enforcement of regulations but also the establishment of accessible and economically attractive formal recycling options, coupled with public awareness campaigns. Addressing these challenges effectively is crucial for realizing a truly sustainable and responsible computer recycling ecosystem that benefits both the economy and the environment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Material Stream & Hazardous Components | -1.1% | Global | Short to Medium-term (2025-2030) |

| Ensuring Complete Data Security & Privacy Compliance | -0.9% | Global, especially developed markets | Short to Medium-term (2025-2029) |

| Management & Regulation of Informal Recycling Sector | -0.8% | Asia Pacific, Latin America, Africa | Medium to Long-term (2026-2033) |

| Lack of Standardized Recycling Processes & Certifications | -0.7% | Global | Short to Medium-term (2025-2030) |

Computer Recycling Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Computer Recycling Market, offering critical insights into its current dynamics, historical performance, and future growth trajectories. The report meticulously examines market size, growth rates, and key trends that are shaping the industry landscape. It delves into the intricate web of market drivers, identifying the forces propelling expansion, and systematically analyzes the restraints, opportunities, and challenges that influence market evolution. The scope includes a detailed segmentation analysis, breaking down the market by various parameters to offer granular insights into consumer behavior, technological adoption, and operational efficiencies across different segments.

Furthermore, the report offers a robust regional analysis, highlighting the distinct market characteristics, regulatory environments, and growth potentials across key geographic areas including North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. It profiles the competitive landscape by identifying and detailing the strategies of leading market players, assessing their market positions, and analyzing their contributions to the industry. Special emphasis is placed on the impact of emerging technologies, such as Artificial Intelligence, on recycling processes and market efficiency, providing a forward-looking perspective on industry transformation.

Designed to serve as a strategic tool, this updated report is invaluable for stakeholders across the value chain, including manufacturers, recyclers, policymakers, and investors. It provides actionable intelligence necessary for informed decision-making, strategic planning, and identifying lucrative investment opportunities within the burgeoning computer recycling sector. The report's structure ensures an easily digestible format, presenting complex market data through insightful narratives, detailed tables, and illustrative bullet points, all aimed at delivering clear, concise, and AEO/GEO optimized information.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 17.2 Billion |

| Market Forecast in 2033 | USD 29.3 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Leading IT Asset Disposition Providers, Global Electronics Recycling Service Providers, Specialized Metal Recovery Firms, Integrated Waste Management Companies, E-waste Collection & Logistics Specialists, Manufacturers with Take-Back Programs, Data Destruction & Security Services, Precious Metal Refiners, Battery Recycling Companies, Refurbishment & Re-use Specialists. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The computer recycling market is broadly segmented to provide a granular understanding of its diverse components, covering the entire lifecycle of electronic waste from its source to material recovery. This segmentation allows for precise analysis of market dynamics, identifying key growth areas, and understanding the varied demands of different stakeholders. The market is primarily categorized by product type, reflecting the different forms of computers and peripherals that require recycling, each with unique material compositions and processing requirements. This includes everything from traditional desktop towers to compact laptops, tablets, and a wide array of server and networking equipment, all contributing distinct waste streams to the recycling ecosystem.

Further segmentation is conducted by the source of e-waste, distinguishing between residential consumers, various commercial entities, and industrial generators. This differentiation is crucial for developing targeted collection strategies and understanding the volume and consistency of waste streams. Commercial sources, encompassing small to large enterprises, government agencies, and educational institutions, often generate significant volumes and require specialized IT Asset Disposition (ITAD) services for secure data handling and certified recycling. Understanding these source-specific needs is vital for market players in tailoring their service offerings and optimizing logistics for efficient e-waste management.

Moreover, the market is segmented by the recycling process itself, detailing the various stages involved from initial collection and logistics to intricate material separation techniques and final smelting or refining. This breakdown highlights the technological advancements and specialized expertise required at each step, from basic dismantling to advanced magnetic and eddy current separation, which are critical for maximizing material recovery. Finally, the market is analyzed by the recovered material types, such as various metals, plastics, and glass, and by the end-user industries that utilize these recovered resources, thereby closing the loop in the circular economy. This comprehensive segmentation provides a holistic view of the market's structure and operational intricacies.

- By Product Type:

- Desktop Computers

- Laptop Computers

- Tablets

- Servers

- Peripherals (Printers, Scanners, Keyboards, Mice, Monitors)

- Networking Equipment

- By Source:

- Residential

- Commercial

- Small & Medium Enterprises

- Large Enterprises

- Government Agencies

- Educational Institutions

- Healthcare Facilities

- Industrial

- By Recycling Process:

- Collection & Logistics

- Dismantling & Segregation

- Shredding & Grinding

- Material Separation

- Magnetic Separation

- Eddy Current Separation

- Water Separation

- Electrostatic Separation

- Smelting & Refining

- Data Destruction

- By Recovered Material:

- Metals

- Copper

- Aluminum

- Gold

- Silver

- Palladium

- Platinum

- Rare Earth Elements

- Plastics

- Glass

- Other Materials

- Metals

- By End-User Industry:

- Metal Refineries

- Plastic Manufacturers

- IT & Electronics Manufacturers (for closed-loop recycling)

- Jewelers

- Automotive Industry

Regional Highlights

- North America: A mature market driven by stringent environmental regulations, high consumer awareness, and significant corporate IT asset turnover. The region benefits from established collection infrastructure and a strong emphasis on secure ITAD services. Key countries include the United States and Canada, leading in technological adoption and advanced recycling processes.

- Europe: Leading the global charge in circular economy initiatives and Extended Producer Responsibility (EPR) schemes. European Union directives set a high standard for e-waste collection and recycling targets, fostering innovation in material recovery and certified recycling practices. Germany, the UK, France, and the Netherlands are key players with robust regulatory frameworks and advanced recycling facilities.

- Asia Pacific (APAC): The largest and fastest-growing market for e-waste generation, driven by rapid urbanization, increasing disposable incomes, and booming electronics consumption in countries like China, India, and Japan. While challenges exist with informal recycling, the region is witnessing increasing investment in formal recycling infrastructure and the adoption of stricter national e-waste policies, particularly in developed economies like South Korea and Australia.

- Latin America: An emerging market with growing awareness of e-waste management and developing regulatory frameworks. Countries like Brazil, Mexico, and Argentina are gradually establishing formal recycling systems, though challenges remain in collection infrastructure and public participation. Opportunities exist for international players to invest in and develop compliant recycling solutions.

- Middle East and Africa (MEA): Currently a nascent market for formal computer recycling, characterized by nascent regulations and limited infrastructure in many areas. However, with increasing electronics penetration and growing environmental concerns, the region presents long-term growth opportunities, particularly in countries like UAE, Saudi Arabia, and South Africa, as governments begin to prioritize e-waste management and attract foreign investment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Computer Recycling Market.- Leading Electronics Recycling Service Providers

- Global IT Asset Disposition (ITAD) Specialists

- Precious Metal Recovery and Refining Companies

- Integrated Waste Management Solution Providers

- Advanced Material Processing & Recovery Firms

- Reverse Logistics and E-waste Collection Networks

- Manufacturers with Product Take-Back Programs

- Certified Data Destruction and Security Services

- Specialized Component Recovery Companies

- Recycling Technology & Equipment Manufacturers

- Environmental Consulting & Compliance Firms

- Battery Recycling Innovators

- Refurbishment and Re-use Market Facilitators

- Sustainable Resource Management Companies

- Urban Mining Research & Development Entities

Frequently Asked Questions

Analyze common user questions about the Computer Recycling market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is computer recycling and why is it important?

Computer recycling is the process of disassembling end-of-life electronic devices to recover valuable materials and safely dispose of hazardous components. It is crucial for environmental protection by preventing landfill pollution, conserving natural resources through urban mining, and ensuring secure data destruction to protect privacy.

What materials can be recovered from old computers?

Old computers contain a wealth of recoverable materials, including precious metals (gold, silver, palladium), base metals (copper, aluminum, steel), plastics, and glass. Advanced recycling processes can extract these materials for reuse in new products, reducing the need for virgin resources.

How do e-waste regulations impact the computer recycling market?

E-waste regulations, such as Extended Producer Responsibility (EPR) schemes, mandate manufacturers and retailers to fund or manage the collection and recycling of their products. These regulations significantly drive the formal computer recycling market by ensuring a steady stream of e-waste and promoting environmentally sound practices.

What are the main challenges in computer recycling?

Key challenges include the complex design of modern electronics (making disassembly difficult), the presence of hazardous materials requiring specialized handling, ensuring complete data security during disposal, and combating the unregulated informal recycling sector that often operates unsafely.

How can I ensure my data is secure when recycling a computer?

To ensure data security, utilize certified IT Asset Disposition (ITAD) services that offer documented data sanitization or physical destruction of storage media. Look for certifications like NAID AAA or R2 to guarantee compliance with data privacy standards and responsible recycling practices.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted