Collateralized Debt Obligation Market

Collateralized Debt Obligation Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701021 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Collateralized Debt Obligation Market Size

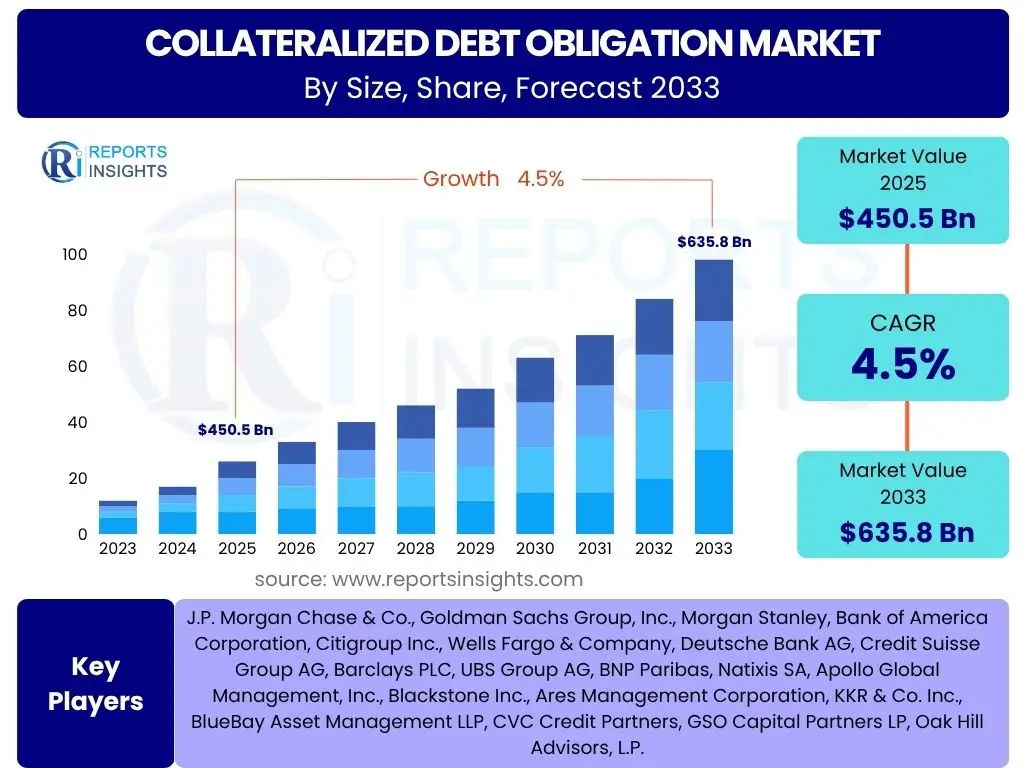

According to Reports Insights Consulting Pvt Ltd, The Collateralized Debt Obligation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 450.5 Billion in 2025 and is projected to reach USD 635.8 Billion by the end of the forecast period in 2033.

Key Collateralized Debt Obligation Market Trends & Insights

Market participants frequently inquire about the prevailing dynamics and forward-looking trajectories within the Collateralized Debt Obligation (CDO) sector. Current analysis indicates a significant shift towards enhanced structural integrity and transparency, largely influenced by post-2008 regulatory reforms. This evolution is fostering greater investor confidence, particularly in asset-backed securities and collateralized loan obligations (CLOs), which constitute a substantial portion of the modern CDO landscape. The market is witnessing a diversification of underlying assets and a sustained appetite for yield-generating financial instruments in a persistent low-interest-rate environment.

Furthermore, the integration of environmental, social, and governance (ESG) factors is emerging as a critical trend, influencing investment decisions and product design. Technology adoption, particularly in data analytics and securitization processes, is enhancing efficiency and risk assessment capabilities. The demand for customized risk-return profiles continues to drive innovation in CDO structuring, enabling sophisticated investors to allocate capital more precisely across various credit exposures. These trends collectively underscore a maturing market focused on robust credit analysis, diligent risk management, and adaptive product offerings.

- Increased focus on Collateralized Loan Obligations (CLOs) as the dominant CDO structure due to their robust performance and direct link to corporate credit.

- Rising demand for bespoke or customized CDO tranches to meet specific investor risk appetites and yield targets.

- Integration of Environmental, Social, and Governance (ESG) criteria into CDO underlying assets and structuring, driven by sustainable finance initiatives.

- Enhanced transparency and regulatory oversight mechanisms leading to more standardized and secure issuance practices.

- Technological advancements, including data analytics and automation, improving the efficiency of CDO origination, servicing, and risk management.

AI Impact Analysis on Collateralized Debt Obligation

Users frequently raise questions regarding the transformative potential of Artificial intelligence (AI) within the Collateralized Debt Obligation domain, particularly concerning its application in risk assessment, asset selection, and portfolio management. AI-driven analytics are poised to revolutionize how CDOs are structured and managed by offering unprecedented capabilities for processing vast datasets, identifying complex patterns, and forecasting credit events with greater accuracy. This technology can significantly enhance the due diligence process, automate the monitoring of underlying collateral, and optimize pricing models, thereby reducing manual effort and human error.

While the benefits are substantial, concerns often center on data quality, model interpretability (the "black box" problem), and the potential for algorithmic bias impacting fair valuation or risk allocation. The integration of AI also raises questions about regulatory compliance and the need for robust governance frameworks to manage autonomous systems in a highly regulated financial sector. Despite these challenges, the prevailing expectation is that AI will bolster the efficiency, transparency, and resilience of the CDO market, enabling more sophisticated risk management strategies and potentially unlocking new investment opportunities through enhanced analytical insights.

- Improved credit risk assessment through advanced predictive modeling of default probabilities and loss given default for underlying assets.

- Automated due diligence processes for collateral selection and monitoring, significantly reducing operational costs and time.

- Enhanced pricing accuracy and valuation models for CDO tranches by analyzing market data and historical performance trends more effectively.

- Identification of emerging risks and potential systemic vulnerabilities within CDO portfolios through real-time data analysis.

- Optimized portfolio construction and rebalancing strategies to achieve target risk-return profiles based on dynamic market conditions.

- Increased efficiency in regulatory reporting and compliance by automating data aggregation and analysis, ensuring adherence to complex rules.

Key Takeaways Collateralized Debt Obligation Market Size & Forecast

Stakeholders frequently seek concise insights into the primary conclusions drawn from the Collateralized Debt Obligation market size and forecast data. A significant takeaway is the market's demonstrated resilience and a trajectory of moderate, sustained growth post-global financial crisis, primarily driven by the robust performance of Collateralized Loan Obligations (CLOs). The forecast indicates a steady expansion, reflecting persistent investor demand for structured credit products that offer attractive yields in a low-yield environment, coupled with a more stringent regulatory landscape that has fostered greater market discipline and transparency.

Another crucial insight is the increasing sophistication in structuring and risk management, which has mitigated some of the historical perceptions of complexity and opacity associated with CDOs. The market's future growth will be intrinsically linked to the health of corporate credit markets, evolving investor appetite for diversified yield, and continuous regulatory oversight that balances market liquidity with systemic stability. The emphasis on asset quality, rigorous underwriting, and transparent reporting remains paramount for sustaining this growth and enhancing overall market confidence.

- The Collateralized Debt Obligation market, led by CLOs, is experiencing stable growth, reflecting investor confidence in well-structured and regulated products.

- Despite past challenges, the market demonstrates resilience, driven by a global search for yield and diversification.

- Stringent regulatory frameworks implemented post-2008 have fundamentally reshaped the market, promoting greater transparency and robust risk management.

- Technological advancements are playing an increasingly vital role in improving the efficiency and accuracy of CDO analysis and management.

- Future growth is anticipated to be influenced by the ongoing evolution of corporate debt markets and the integration of sustainable finance principles.

Collateralized Debt Obligation Market Drivers Analysis

The Collateralized Debt Obligation (CDO) market is propelled by several key drivers that reflect both investor demand and structural market dynamics. A primary driver is the pervasive search for yield among institutional investors, particularly in an environment characterized by low interest rates and compressed returns on traditional fixed-income assets. CDOs, especially Collateralized Loan Obligations (CLOs), offer relatively attractive risk-adjusted returns by pooling diverse credit assets. Furthermore, the increasing sophistication of financial engineering and risk management tools allows for the creation of tailored investment products that meet specific risk-return profiles, appealing to a broad spectrum of sophisticated investors seeking diversification and customized exposure to credit markets. The continuous expansion of global corporate debt markets also provides a robust pipeline of underlying assets for new CDO issuance.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Search for Yield | +1.2% | North America, Europe, Asia Pacific | Long-term (5+ years) |

| Increasing Demand for Structured Credit Products | +0.9% | Global | Medium-term (3-5 years) |

| Growth in Corporate Debt Markets | +0.8% | North America, Europe, China | Medium-term (3-5 years) |

| Advancements in Financial Modeling and Analytics | +0.6% | Global | Long-term (5+ years) |

Collateralized Debt Obligation Market Restraints Analysis

Despite the growth drivers, the Collateralized Debt Obligation (CDO) market faces significant restraints, primarily stemming from the legacy of the 2008 financial crisis and subsequent regulatory responses. Stringent regulatory frameworks, such as those imposed by Dodd-Frank and Basel III/IV, have increased compliance costs, capital requirements, and reporting burdens for financial institutions involved in CDO issuance and investment. These regulations, while enhancing stability, can limit market liquidity and issuance volume. Furthermore, the negative public perception and reputational risks associated with CDOs, particularly outside of the CLO segment, continue to deter a segment of investors and can complicate market acceptance of new product innovations. The inherent complexity and occasional opacity of underlying assets within some CDO structures also pose challenges for comprehensive risk assessment and valuation, especially for less sophisticated investors. Economic downturns and periods of credit market volatility can quickly dampen investor appetite, leading to reduced issuance and trading activity in the secondary market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Frameworks | -1.0% | North America, Europe | Long-term (5+ years) |

| Reputational Risk and Public Perception | -0.7% | Global | Long-term (5+ years) |

| Complexity and Opacity of Underlying Assets | -0.5% | Global | Medium-term (3-5 years) |

| Economic Downturns and Credit Market Volatility | -0.8% | Global | Short-term (1-3 years) |

Collateralized Debt Obligation Market Opportunities Analysis

The Collateralized Debt Obligation (CDO) market presents several compelling opportunities for growth and innovation. A significant avenue lies in the increasing focus on sustainable finance, leading to the emergence of ESG-linked CDOs that collateralize green bonds, social loans, or other assets aligned with environmental, social, and governance criteria. This trend caters to a growing pool of institutional investors with mandates for responsible investing. Additionally, the expansion of the private credit and middle-market lending sectors offers a rich source of diverse underlying assets for new CLO issuance, tapping into segments traditionally underserved by public markets. Technological advancements, particularly in blockchain and distributed ledger technologies, present an opportunity to enhance transparency, efficiency, and liquidity in CDO issuance and trading by creating immutable records and streamlining settlement processes. Finally, the gradual expansion into emerging markets, as these economies develop more sophisticated corporate debt markets and structured finance capabilities, could unlock new geographical opportunities for CDO investors seeking diversified returns.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of ESG-linked CDOs | +0.7% | Europe, North America | Long-term (5+ years) |

| Growth in Private Credit/Middle Market CLOs | +0.6% | North America, Europe | Medium-term (3-5 years) |

| Technological Advancements (e.g., Blockchain for Securitization) | +0.5% | Global | Long-term (5+ years) |

| Expansion into Emerging Markets | +0.4% | Asia Pacific, Latin America | Long-term (5+ years) |

Collateralized Debt Obligation Market Challenges Impact Analysis

The Collateralized Debt Obligation (CDO) market faces several critical challenges that require strategic navigation by market participants. One significant challenge is adapting to and consistently complying with the continuously evolving global regulatory landscapes. Divergent regulations across jurisdictions can create complexities and increase operational costs for cross-border CDO issuance and investment. Managing interest rate risk is another persistent challenge, as fluctuating interest rates can impact the valuation of both the underlying assets and the CDO tranches, potentially affecting investor returns and market stability. Ensuring consistent transparency and high-quality data for all underlying assets remains a formidable task, particularly given the often complex and diverse nature of the collateral pools, which is crucial for accurate risk assessment and maintaining investor confidence. Additionally, overcoming the historical skepticism from some institutional and retail investors, especially those not specializing in structured finance, and attracting new capital flows into certain CDO segments beyond the widely accepted CLOs, continues to be an ongoing market development challenge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Navigating Evolving Regulatory Landscapes | -0.9% | Global | Long-term (5+ years) |

| Managing Interest Rate Risk Volatility | -0.7% | Global | Short-term (1-3 years) |

| Ensuring Transparency and Data Quality of Underlying Assets | -0.6% | Global | Medium-term (3-5 years) |

| Overcoming Investor Skepticism and Attracting New Capital | -0.5% | Global | Long-term (5+ years) |

Collateralized Debt Obligation Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Collateralized Debt Obligation market, covering historical data, current market trends, and future growth projections. It aims to offer strategic insights into market size, segmentation, regional dynamics, competitive landscape, and the impact of key drivers, restraints, opportunities, and challenges affecting the market from 2019 to 2033. The report is designed to assist financial institutions, investors, asset managers, and policymakers in making informed decisions by providing a detailed understanding of the market's structure and outlook.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450.5 Billion |

| Market Forecast in 2033 | USD 635.8 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | J.P. Morgan Chase & Co., Goldman Sachs Group, Inc., Morgan Stanley, Bank of America Corporation, Citigroup Inc., Wells Fargo & Company, Deutsche Bank AG, Credit Suisse Group AG, Barclays PLC, UBS Group AG, BNP Paribas, Natixis SA, Apollo Global Management, Inc., Blackstone Inc., Ares Management Corporation, KKR & Co. Inc., BlueBay Asset Management LLP, CVC Credit Partners, GSO Capital Partners LP, Oak Hill Advisors, L.P. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Collateralized Debt Obligation (CDO) market is comprehensively segmented to provide granular insights into its diverse components and dynamics. This segmentation facilitates a deeper understanding of market trends, investor preferences, and regulatory impacts across various product types, issuer categories, investor demographics, and credit quality levels. Such detailed analysis allows for precise market sizing, forecasting, and strategic planning, enabling stakeholders to identify specific growth areas and potential risks within the intricate structured finance landscape. The varied nature of underlying assets and structural characteristics necessitates a multi-faceted approach to market analysis.

- By Type:

- Collateralized Loan Obligations (CLOs): Dominant segment, backed by corporate loans.

- Collateralized Bond Obligations (CBOs): Secured by a pool of corporate bonds.

- Collateralized Mortgage Obligations (CMOs): Backed by mortgage-backed securities (MBS).

- Collateralized Fund Obligations (CFOs): Collateralized by interests in private equity or hedge funds.

- Synthetic CDOs: Derive value from credit default swaps or other derivatives, not directly from physical assets.

- Hybrid CDOs: Combine physical assets with synthetic instruments.

- By Issuer:

- Banks: Financial institutions originating and structuring CDOs.

- Investment Banks: Specialized firms in securitization and distribution.

- Asset Managers: Firms managing large portfolios and structuring CDOs for clients.

- Corporations: Issuing CDOs backed by their own assets or receivables.

- Others: Including government agencies or special purpose vehicles.

- By Investor Type:

- Institutional Investors: Pension funds, insurance companies, hedge funds, endowments, sovereign wealth funds seeking yield and diversification.

- Retail Investors: Limited participation, primarily through specialized funds.

- Corporations: Investing surplus cash or managing specific exposures.

- Others: Diverse entities with specific investment mandates.

- By Rating:

- Investment Grade: Tranches rated highly by credit rating agencies, indicating lower risk.

- Non-Investment Grade: Tranches with higher perceived risk and consequently higher potential returns.

Regional Highlights

- North America: The United States remains the largest and most mature market for Collateralized Debt Obligations, particularly for CLOs. This region benefits from a robust corporate loan market, a sophisticated investor base, and a well-established regulatory framework. The demand for yield-generating structured products from pension funds, insurance companies, and asset managers is a significant driver, with a strong focus on asset quality and transparency post-crisis. Canada also contributes to regional activity, albeit on a smaller scale.

- Europe: Europe represents another key market for CDOs, predominantly through its CLO segment. The region's market is characterized by diverse legal and regulatory environments across member states within the European Union, influencing issuance and investment practices. Regulatory initiatives such as the EU Securitisation Regulation aim to standardize and simplify securitization, promoting market growth while ensuring financial stability. Key markets include the UK, Germany, France, and the Netherlands, with growing interest in ESG-compliant structures.

- Asia Pacific (APAC): The APAC region is an emerging but rapidly growing market for Collateralized Debt Obligations. Driven by expanding corporate debt markets, increasing investor sophistication, and the search for higher returns, countries like Japan, Australia, Singapore, and China are witnessing a gradual increase in CDO issuance and investment. While regulatory frameworks are still evolving in some parts of the region, the long-term potential is significant, fueled by economic growth and capital market development.

- Latin America: The CDO market in Latin America is relatively nascent, characterized by intermittent issuance and a developing investor base. Brazil, Mexico, and Chile are at the forefront of structured finance development, with a focus on local currency-denominated assets. Challenges include economic volatility, less developed credit markets, and varying regulatory environments, but increasing interest in securitization is observed as economies mature.

- Middle East and Africa (MEA): The MEA region's Collateralized Debt Obligation market is still in its early stages of development. Growth is primarily driven by specific opportunities in project finance, real estate, and infrastructure, particularly in the Gulf Cooperation Council (GCC) countries. Islamic finance principles also play a role, influencing the structuring of Sharia-compliant securitized products. The market faces challenges related to liquidity and regulatory harmonization but offers long-term potential as financial markets deepen.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Collateralized Debt Obligation Market.- J.P. Morgan Chase & Co.

- Goldman Sachs Group, Inc.

- Morgan Stanley

- Bank of America Corporation

- Citigroup Inc.

- Wells Fargo & Company

- Deutsche Bank AG

- Credit Suisse Group AG

- Barclays PLC

- UBS Group AG

- BNP Paribas

- Natixis SA

- Apollo Global Management, Inc.

- Blackstone Inc.

- Ares Management Corporation

- KKR & Co. Inc.

- BlueBay Asset Management LLP

- CVC Credit Partners

- GSO Capital Partners LP

- Oak Hill Advisors, L.P.

Frequently Asked Questions

Analyze common user questions about the Collateralized Debt Obligation market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Collateralized Debt Obligation (CDO)?

A Collateralized Debt Obligation (CDO) is a complex structured finance product that is collateralized by a pool of debt obligations, such as corporate loans, bonds, mortgages, or other types of credit. These pooled assets are then tranches into different slices, each with varying levels of risk and return, which are sold to investors.

How does a CDO work?

In a CDO, a Special Purpose Vehicle (SPV) issues various tranches of securities to investors, backed by cash flows from the underlying pool of debt assets. These tranches have different seniority levels, meaning senior tranches are paid first but offer lower returns, while junior (equity) tranches are paid last but offer potentially higher returns to compensate for higher risk. The SPV manages the collateral and distributes payments to investors according to the tranche's priority waterfall.

What types of assets are typically included in a CDO?

The most common underlying assets for CDOs are corporate loans, forming Collateralized Loan Obligations (CLOs). Other assets can include corporate bonds (CBOs), mortgage-backed securities (CMOs), asset-backed securities (ABS), and even interests in other funds (CFOs). Some CDOs can also be synthetic, deriving their value from credit default swaps rather than actual physical assets.

What are the primary risks associated with investing in CDOs?

Key risks include credit risk, where the underlying assets default, leading to losses for investors. Liquidity risk can arise if a secondary market for the CDO tranches is illiquid, making them difficult to sell. Complexity risk stems from the intricate structure of CDOs, making valuation and risk assessment challenging. Finally, interest rate risk can impact the value of both the underlying assets and the CDO tranches.

How has the CDO market evolved since the 2008 financial crisis?

Post-2008, the CDO market has undergone significant transformation, largely driven by stringent regulatory reforms like Dodd-Frank and Basel III/IV. This has led to a much greater focus on transparency, higher quality underlying collateral, and robust risk management practices. Collateralized Loan Obligations (CLOs) have emerged as the dominant and more resilient segment, benefiting from direct exposure to corporate loans and a more standardized structure, while other CDO types have seen reduced activity due to heightened scrutiny and complexity concerns.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted