Chiller Market

Chiller Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704056 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Chiller Market Size

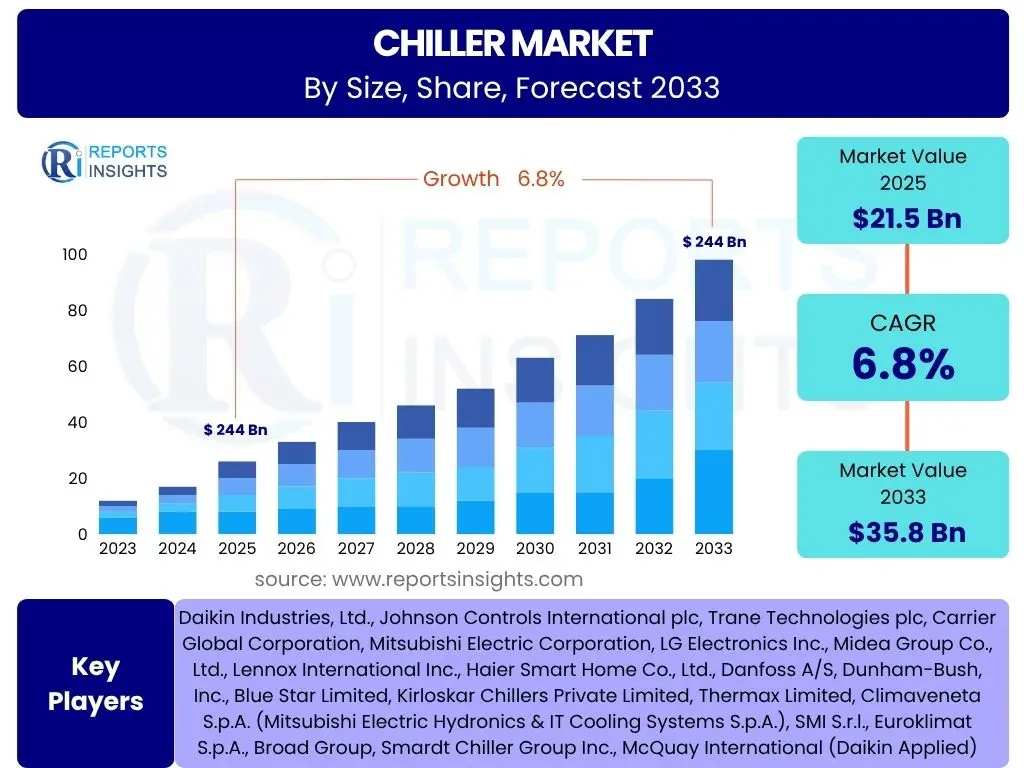

According to Reports Insights Consulting Pvt Ltd, The Chiller Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 21.5 billion in 2025 and is projected to reach USD 35.8 billion by the end of the forecast period in 2033.

Key Chiller Market Trends & Insights

Common user inquiries regarding the chiller market frequently revolve around its evolving technological landscape, shifts in regulatory frameworks, and the broader economic and environmental factors influencing demand. Users are particularly interested in understanding how advancements in energy efficiency, the adoption of eco-friendly refrigerants, and the integration of smart technologies are reshaping the industry. There is a strong emphasis on sustainability and operational cost reduction, driving the development of more advanced chiller systems.

The market is experiencing a significant pivot towards intelligent and interconnected cooling solutions. This includes the proliferation of chillers equipped with IoT capabilities, enabling real-time monitoring, predictive maintenance, and remote diagnostics. The demand for systems that offer superior energy performance, often driven by stringent energy efficiency standards and rising electricity costs, is consistently increasing. Furthermore, the imperative to reduce carbon footprints is accelerating the transition to chillers that utilize refrigerants with low Global Warming Potential (GWP), even as the industry navigates the complexities of phasedown regulations.

Regional market dynamics also play a crucial role, with varied trends observed across developed and emerging economies. While mature markets in North America and Europe focus on replacing aging infrastructure with high-efficiency models and complying with environmental mandates, rapid industrialization and urbanization in Asia Pacific and Latin America are spurring demand for new installations across commercial, industrial, and institutional sectors. The expansion of data centers globally represents a substantial growth area, requiring specialized, high-capacity, and resilient cooling solutions, further influencing market trends.

- Emphasis on energy-efficient chillers due to rising energy costs and stricter regulations.

- Growing adoption of eco-friendly refrigerants with low Global Warming Potential (GWP).

- Integration of smart technologies, IoT, and AI for predictive maintenance and optimized performance.

- Increasing demand for district cooling systems in urban areas.

- Rapid expansion of data centers and server farms driving demand for specialized cooling solutions.

- Modular and scalable chiller designs gaining traction for flexibility and ease of installation.

- Shift towards Absorption Chillers in regions with abundant waste heat or natural gas.

- Focus on noise reduction and smaller footprints for urban and commercial applications.

AI Impact Analysis on Chiller

User questions regarding the impact of Artificial Intelligence (AI) on the chiller market primarily focus on how AI can enhance efficiency, reduce operational costs, and improve system reliability. Users are keen to understand the practical applications of AI, such as predictive maintenance to minimize downtime, optimized energy consumption through intelligent control algorithms, and advanced fault detection capabilities. The overarching theme is how AI can transform chillers from standalone cooling units into smart, self-optimizing components of a larger building management or industrial process system.

AI's influence extends across the entire lifecycle of chiller systems, from design and manufacturing to operation and maintenance. In the operational phase, AI algorithms can analyze vast amounts of data from sensors, including temperature, pressure, flow rates, and energy consumption, to identify patterns and anomalies. This allows for real-time adjustments to optimize cooling loads, compressor speeds, and refrigerant flow, leading to significant energy savings. Predictive maintenance, powered by AI, can anticipate component failures before they occur, enabling proactive repairs and reducing the likelihood of costly, unexpected breakdowns.

Furthermore, AI facilitates greater integration of chillers into broader building automation and energy management systems. This enables chillers to respond dynamically to fluctuating demand, external weather conditions, and electricity pricing, enhancing overall energy efficiency and grid responsiveness. The development of AI-driven diagnostic tools also simplifies troubleshooting, making it easier for facility managers to identify and resolve issues. As AI capabilities become more sophisticated, they are expected to drive the development of truly autonomous chiller systems that can adapt and learn over time, further revolutionizing the HVAC industry.

- Enhanced energy efficiency through AI-driven optimization of chiller operations.

- Predictive maintenance capabilities, reducing downtime and operational costs.

- Real-time fault detection and diagnostics using machine learning algorithms.

- Integration with Building Management Systems (BMS) for intelligent control and automation.

- Improved chiller performance and lifespan through continuous adaptive learning.

- Automated anomaly detection and performance degradation warnings.

- Optimization of refrigerant charge and flow for peak efficiency.

Key Takeaways Chiller Market Size & Forecast

Common user questions about the key takeaways from the Chiller market size and forecast often center on identifying the primary growth drivers, understanding the most significant regional contributions, and discerning the long-term opportunities and challenges. Users seek concise summaries of what truly drives the market forward, what might impede its growth, and where the most promising investment opportunities lie. The emphasis is on actionable insights derived from the market's projected trajectory and underlying dynamics.

A central takeaway is the robust and consistent growth trajectory of the chiller market, primarily propelled by global industrial expansion, infrastructure development, and increasing urbanization. The escalating demand for efficient cooling solutions across diverse sectors such as commercial buildings, data centers, healthcare facilities, and manufacturing industries is a fundamental driver. Furthermore, the imperative for energy conservation and the adoption of environmentally friendly technologies are not merely regulatory burdens but significant market accelerators, fostering innovation and pushing for more sustainable chiller solutions.

From a strategic perspective, the market presents significant opportunities for companies investing in advanced technologies, particularly those related to energy efficiency, smart controls, and sustainable refrigerants. While the market faces challenges such as high initial investment costs and the complexities of regulatory compliance, these are often offset by long-term operational savings and environmental benefits. Geographically, Asia Pacific is poised to remain a dominant force due to rapid development and industrialization, while mature markets will focus on replacement cycles and premium, high-efficiency systems. Understanding these dynamics is crucial for stakeholders positioning themselves for future success.

- Consistent market growth driven by industrialization, urbanization, and infrastructure development.

- Strong emphasis on energy efficiency and sustainable cooling solutions as core market drivers.

- Asia Pacific region identified as a primary growth engine due to robust economic expansion.

- Increased adoption of smart and connected chiller systems for optimized performance.

- The data center boom represents a significant, specialized demand segment.

- Regulatory pressures for eco-friendly refrigerants are shaping product innovation.

Chiller Market Drivers Analysis

The chiller market's robust growth is primarily propelled by the accelerating pace of global industrialization and urbanization. As economies expand, there is a commensurate increase in the construction of commercial buildings, residential complexes, and manufacturing facilities, all of which require sophisticated cooling and climate control systems. This construction boom, particularly evident in emerging economies, directly translates into heightened demand for chillers. Furthermore, the continuous expansion of critical infrastructure, such as hospitals, airports, and educational institutions, mandates reliable and efficient cooling, reinforcing market growth.

A pivotal driver also stems from the growing global imperative for energy efficiency and sustainable practices. With rising energy costs and increasingly stringent environmental regulations, end-users are compelled to invest in modern, high-efficiency chiller systems that consume less power and utilize refrigerants with lower environmental impact. This shift is driving innovation in chiller design, leading to the development of variable speed drives, magnetic bearing compressors, and advanced control systems that optimize energy consumption. The drive for sustainability is not merely regulatory compliance but a core business strategy for many organizations aiming to reduce operational expenses and enhance their corporate social responsibility profile.

Lastly, the exponential growth of the data center industry worldwide acts as a significant catalyst for the chiller market. Data centers require massive, uninterrupted cooling to prevent equipment overheating and ensure operational continuity. As cloud computing, artificial intelligence, and big data analytics become more pervasive, the construction and expansion of hyperscale and edge data centers are accelerating, creating a specialized and high-volume demand for advanced chiller solutions. These facilities often require highly efficient, redundant, and precise cooling systems, pushing the boundaries of chiller technology.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Urbanization & Industrialization | +1.5% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Increasing Demand for Energy-Efficient Solutions | +1.2% | North America, Europe, Asia Pacific | 2025-2033 |

| Growth of Data Centers & IT Infrastructure | +1.0% | Global | 2025-2033 |

| Stringent Environmental Regulations (Refrigerants) | +0.8% | Europe, North America | 2025-2030 |

| Expansion of Commercial & Residential Construction | +0.7% | Asia Pacific, Latin America | 2025-2033 |

Chiller Market Restraints Analysis

Despite the positive growth trajectory, the chiller market faces several significant restraints that could impede its expansion. One primary concern is the high initial capital investment required for purchasing and installing chiller systems, especially advanced, high-capacity, or energy-efficient models. This substantial upfront cost can be a barrier for small and medium-sized enterprises (SMEs) or budget-constrained projects, leading them to opt for less efficient, older technologies or to defer investments, particularly in developing regions where access to financing may be limited.

Another notable restraint is the complexity and fluctuating nature of environmental regulations related to refrigerants. Global agreements like the Kigali Amendment to the Montreal Protocol mandate the phase-down of high Global Warming Potential (GWP) refrigerants. While this drives innovation, it also creates challenges for manufacturers and end-users alike. Manufacturers must invest heavily in research and development for new, low-GWP alternatives, which can be costly and time-consuming. For end-users, there is uncertainty regarding the long-term availability and cost of older refrigerants, as well as the need for system retrofits or replacements, adding to operational complexities and costs.

Furthermore, the chiller market is susceptible to economic downturns and geopolitical instability. Construction and industrial expansion, which are major demand drivers for chillers, are highly sensitive to economic cycles. A recession or a slowdown in global GDP growth can significantly reduce new construction projects and industrial output, thereby impacting chiller sales. Supply chain disruptions, often exacerbated by geopolitical tensions, can also lead to increased material costs, extended lead times, and manufacturing delays, negatively affecting market stability and profitability for manufacturers and increasing prices for consumers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -0.9% | Global, particularly SMEs | 2025-2033 |

| Complex & Changing Refrigerant Regulations | -0.7% | Europe, North America, Global | 2025-2030 |

| Economic Slowdowns & Geopolitical Instability | -0.6% | Global (variable) | Short-term to Mid-term |

| Lack of Skilled Technicians for Advanced Systems | -0.4% | Emerging Economies | 2025-2033 |

Chiller Market Opportunities Analysis

The chiller market is ripe with opportunities driven by technological advancements and evolving environmental consciousness. One significant area of opportunity lies in the burgeoning demand for energy-efficient and sustainable chiller solutions. As energy costs continue to rise globally and environmental regulations become more stringent, there is a strong incentive for businesses and industries to upgrade their existing chiller systems to newer models that offer superior energy performance and utilize low-GWP refrigerants. This replacement market, combined with new installations driven by green building initiatives, represents a substantial growth avenue for manufacturers capable of delivering cutting-edge, eco-friendly technologies.

Another major opportunity stems from the rapid expansion of specialized cooling applications, particularly within the data center and healthcare sectors. Data centers, critical for supporting the digital economy, require highly reliable, precise, and often custom cooling solutions to manage the intense heat generated by servers. Similarly, the healthcare industry, including hospitals, pharmaceutical manufacturing, and laboratories, demands extremely stable temperature and humidity control, creating a consistent need for high-performance chillers. As these sectors continue to grow globally, so too will the demand for specialized, high-capacity, and redundant chiller systems.

Furthermore, the integration of smart technologies, such as the Internet of Things (IoT), Artificial Intelligence (AI), and advanced analytics, presents significant opportunities for innovation and market differentiation. Chillers equipped with smart sensors and connectivity can offer real-time monitoring, predictive maintenance, and optimized operational efficiency. Manufacturers that can effectively leverage these technologies to provide value-added services, such as remote diagnostics, performance optimization contracts, and integrated energy management solutions, will gain a competitive edge. This shift towards "smart chillers" not only improves system performance but also reduces operational costs for end-users, driving adoption and opening new revenue streams for market players.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Green Building Solutions | +1.3% | Global | 2025-2033 |

| Technological Advancements (IoT, AI, Analytics) | +1.1% | North America, Europe, Asia Pacific | 2025-2033 |

| Growth in District Cooling & Heating Systems | +0.9% | Middle East, Asia Pacific, Europe | 2025-2033 |

| Expansion of Pharma & Healthcare Industries | +0.7% | Global | 2025-2033 |

Chiller Market Challenges Impact Analysis

The chiller market faces several notable challenges that could affect its growth trajectory and operational efficiency. One significant challenge is the ongoing pressure from evolving environmental regulations concerning refrigerants. While these regulations, such as the F-gas regulation in Europe or the SNAP program in the US, aim to phase down high-GWP substances, they simultaneously create complexities for manufacturers in terms of research and development costs, production adjustments, and the availability of suitable low-GWP alternatives. For end-users, this translates into potential retrofit costs for existing systems and uncertainty about future refrigerant supply and pricing.

Another key challenge is the volatility in raw material prices, particularly for metals like copper and steel, which are integral components in chiller manufacturing. Fluctuations in commodity markets, often driven by global supply chain disruptions, geopolitical events, or economic shifts, can directly impact manufacturing costs. This volatility can lead to higher production expenses for manufacturers, which may then be passed on to consumers, potentially affecting market competitiveness and demand. Managing these cost variations while maintaining profit margins and offering competitive pricing remains a continuous struggle for industry players.

Furthermore, the market faces a significant challenge in the form of a shortage of skilled labor and technical expertise for installation, maintenance, and repair of advanced chiller systems. As chillers become more sophisticated with integrated smart technologies, IoT, and complex control algorithms, the demand for highly trained technicians increases. The lack of adequately skilled professionals, especially in emerging markets, can lead to improper installations, inefficient operations, increased downtime, and higher service costs, undermining the benefits of advanced chiller technologies and potentially impacting customer satisfaction and market adoption rates.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.8% | Global | Short-term to Mid-term |

| Shortage of Skilled Technicians | -0.6% | Global, particularly Emerging Economies | 2025-2033 |

| Intense Competition from Local Manufacturers | -0.5% | Asia Pacific | 2025-2033 |

| High Power Consumption of Older Systems | -0.4% | Global | 2025-2030 |

Chiller Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Chiller Market, covering historical data from 2019 to 2023, a base year of 2024, and detailed forecasts up to 2033. The report offers critical insights into market size, growth drivers, restraints, opportunities, and challenges, along with detailed segmentation analysis across various types, capacities, components, and end-use industries, providing a holistic view of the market landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 21.5 Billion |

| Market Forecast in 2033 | USD 35.8 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Daikin Industries, Ltd., Johnson Controls International plc, Trane Technologies plc, Carrier Global Corporation, Mitsubishi Electric Corporation, LG Electronics Inc., Midea Group Co., Ltd., Lennox International Inc., Haier Smart Home Co., Ltd., Danfoss A/S, Dunham-Bush, Inc., Blue Star Limited, Kirloskar Chillers Private Limited, Thermax Limited, Climaveneta S.p.A. (Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A.), SMI S.r.l., Euroklimat S.p.A., Broad Group, Smardt Chiller Group Inc., McQuay International (Daikin Applied) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The chiller market is segmented to provide a granular understanding of its diverse applications and technological variations. This segmentation includes analysis by type, capacity, component, end-use industry, and refrigerant type, each offering unique insights into demand patterns and market dynamics. By breaking down the market into these specific categories, stakeholders can identify niche opportunities, understand competitive landscapes within particular segments, and tailor their strategies to address specific market needs and regulatory requirements across different regions.

Segmentation by type, such as air-cooled, water-cooled, absorption, centrifugal, screw, scroll, and reciprocating chillers, highlights the preferences and technological maturity within various applications. For instance, water-cooled chillers are often preferred for large commercial and industrial applications due to their higher efficiency, while air-cooled chillers are prevalent in smaller commercial buildings and residential sectors due to their ease of installation. Absorption chillers, powered by waste heat, find relevance in industries seeking energy recovery solutions, demonstrating the diverse utility across types.

Further segmentation by end-use industry—including commercial, industrial, residential, and specialized sectors like data centers and healthcare—reveals the key demand drivers. The commercial sector, encompassing office buildings, retail spaces, and hotels, represents a significant market share. The industrial segment, covering manufacturing, food & beverage, and chemical industries, demands robust and high-capacity chillers for process cooling. The burgeoning data center market, driven by digital transformation, stands out as a high-growth area requiring highly efficient and reliable cooling infrastructure. Understanding these segments is crucial for targeted market penetration and product development.

- By Type: Air-Cooled Chiller, Water-Cooled Chiller, Absorption Chiller, Centrifugal Chiller, Screw Chiller, Scroll Chiller, Reciprocating Chiller.

- By Capacity: Less Than 200 Tons, 200-500 Tons, More Than 500 Tons.

- By Component: Compressor, Condenser, Evaporator, Expansion Valve, Control Panel, Others.

- By End-Use Industry: Commercial (Office Buildings, Retail, Hospitality, Healthcare, Educational Institutions), Industrial (Manufacturing, Food & Beverage, Chemical & Pharmaceutical, Data Centers), Residential, Others.

- By Refrigerant Type: HFCs (Hydrofluorocarbons), HFOs (Hydrofluoroolefins), Natural Refrigerants (Ammonia, CO2, Hydrocarbons), Others.

Regional Highlights

- North America: This region is characterized by a strong emphasis on energy efficiency and the adoption of smart building technologies. The replacement market is significant as older infrastructure is upgraded to comply with stricter environmental regulations and rising energy costs. Growth is also spurred by the expansion of data centers and specialized industrial applications. The presence of major market players and robust R&D activities contribute to a highly competitive and technologically advanced market.

- Europe: Driven by stringent environmental policies, particularly the F-Gas regulation, Europe is at the forefront of adopting low-GWP refrigerants and highly efficient chiller systems. The focus is on sustainability, decarbonization, and the integration of chillers into district cooling networks. Germany, France, and the UK are key contributors, investing heavily in modernizing existing infrastructure and promoting green building initiatives.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid urbanization, industrialization, and infrastructure development, particularly in countries like China, India, and Southeast Asian nations. The burgeoning commercial and residential construction sectors, coupled with the expansion of manufacturing industries and data centers, are driving substantial demand for new chiller installations. Rising disposable incomes and improving living standards also contribute to increased adoption.

- Latin America: This region exhibits steady growth driven by increasing commercial development, a growing industrial base, and a rising focus on energy efficiency. Countries like Brazil and Mexico are leading the market, with investments in hospitality, retail, and manufacturing sectors. The market is also influenced by increasing awareness of sustainable cooling solutions, although initial investment costs can sometimes be a barrier.

- Middle East and Africa (MEA): The MEA region, particularly the Gulf Cooperation Council (GCC) countries, showcases significant demand for chillers due to extreme climatic conditions and massive infrastructure projects, including smart cities, tourism developments, and commercial hubs. The expansion of district cooling systems is a major trend in this region. Africa's market is emerging, driven by urbanization and industrial growth in key economies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Chiller Market.- Daikin Industries, Ltd.

- Johnson Controls International plc

- Trane Technologies plc

- Carrier Global Corporation

- Mitsubishi Electric Corporation

- LG Electronics Inc.

- Midea Group Co., Ltd.

- Lennox International Inc.

- Haier Smart Home Co., Ltd.

- Danfoss A/S

- Dunham-Bush, Inc.

- Blue Star Limited

- Kirloskar Chillers Private Limited

- Thermax Limited

- Climaveneta S.p.A. (Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A.)

- SMI S.r.l.

- Euroklimat S.p.A.

- Broad Group

- Smardt Chiller Group Inc.

- McQuay International (Daikin Applied)

Frequently Asked Questions

Analyze common user questions about the Chiller market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Chiller Market?

The Chiller Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 35.8 billion by 2033.

Which factors are driving the Chiller Market's growth?

Key drivers include rapid urbanization and industrialization, increasing demand for energy-efficient cooling solutions, the exponential growth of data centers, and stringent environmental regulations promoting sustainable refrigerants.

How is AI impacting the Chiller Market?

AI is transforming the chiller market by enabling enhanced energy efficiency through optimized operations, predictive maintenance, real-time fault detection, and seamless integration with building management systems for intelligent control.

What are the primary challenges in the Chiller Market?

Major challenges include high initial capital investment costs, the complexity and volatility of environmental regulations concerning refrigerants, fluctuations in raw material prices, and a shortage of skilled technicians for advanced systems.

Which region is expected to lead the Chiller Market growth?

The Asia Pacific (APAC) region is anticipated to be the fastest-growing market due to its rapid urbanization, extensive industrialization, significant infrastructure development, and increasing commercial and residential construction activities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted