Aniline Market

Aniline Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700781 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

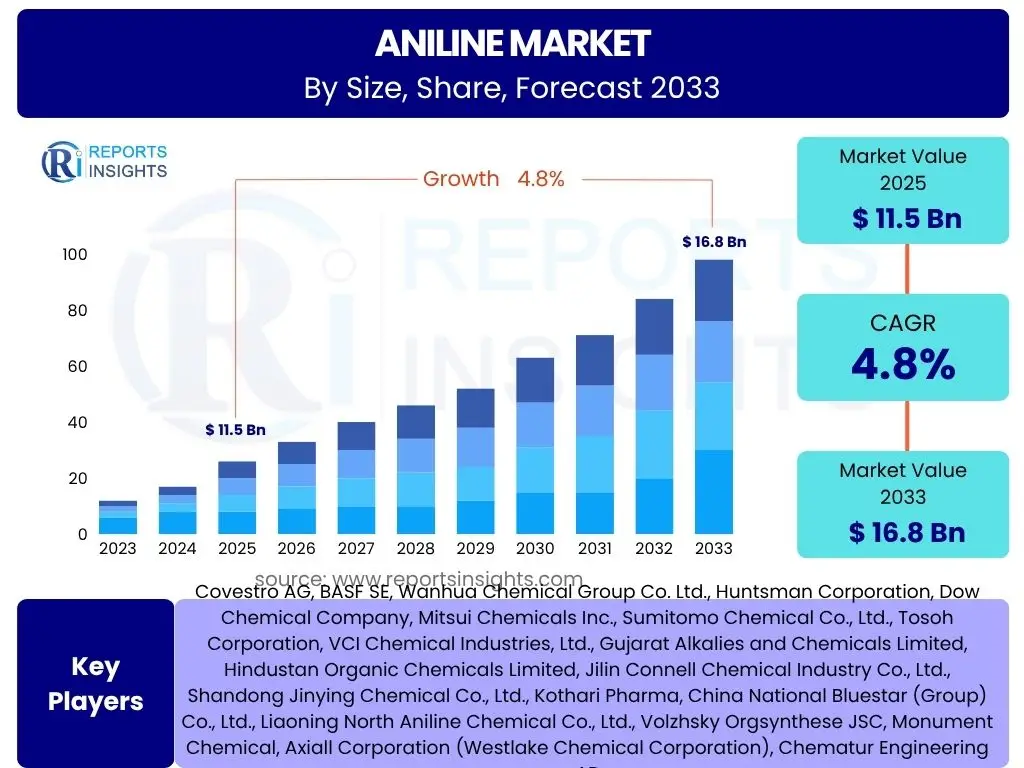

Aniline Market Size

According to Reports Insights Consulting Pvt Ltd, The Aniline Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 11.5 billion in 2025 and is projected to reach USD 16.8 billion by the end of the forecast period in 2033.

Key Aniline Market Trends & Insights

The Aniline market is currently experiencing significant shifts driven by evolving industrial demands and sustainability imperatives. Primary user inquiries often revolve around the emergence of new application areas, the impact of stricter environmental regulations, and the ongoing push for more sustainable manufacturing processes. There is keen interest in how technological advancements in production methods, such as catalytic hydrogenation, are influencing cost efficiencies and product purity. Furthermore, the market's trajectory is heavily influenced by the global growth of polyurethane production, particularly in construction and automotive sectors, leading to a consistent demand for MDI, a key derivative of Aniline.

Another area of considerable interest pertains to regional market dynamics, with a focus on growth opportunities in emerging economies and the diversification of end-use applications beyond traditional sectors. Users frequently seek information on the competitive landscape, including the strategies employed by major players to expand capacity, secure raw material supplies, and innovate their product portfolios. The interplay between raw material price volatility, supply chain resilience, and global economic conditions also forms a crucial part of user concerns, highlighting the need for adaptable market strategies.

- Growing demand for Methyl Diphenyl Diisocyanate (MDI) from the polyurethane industry, driven by construction and automotive sectors.

- Increasing adoption of Aniline in diverse applications such as rubber processing chemicals, agrochemicals, and specialty polymers.

- Shift towards bio-based Aniline production to meet sustainability goals and reduce reliance on fossil resources.

- Technological advancements in production processes aiming for higher efficiency and lower environmental impact.

- Stringent environmental regulations compelling manufacturers to invest in eco-friendly production methods and waste management.

- Expansion of manufacturing capacities in Asia Pacific due to burgeoning industrial growth and lower production costs.

- Focus on supply chain optimization and backward integration to mitigate raw material price volatility.

AI Impact Analysis on Aniline

User queries regarding Artificial Intelligence's impact on the Aniline market primarily center on its potential to revolutionize production efficiency, enhance research and development, and optimize supply chain logistics. Stakeholders are keen to understand how AI-driven analytics can improve process control in Aniline synthesis, leading to higher yields and reduced energy consumption. There is also significant interest in AI's role in predictive maintenance for manufacturing equipment, minimizing downtime and increasing operational reliability, which directly impacts production capacity and cost-effectiveness within this capital-intensive industry.

Furthermore, inquiries often delve into the application of AI in discovering new catalysts or optimizing existing catalytic processes for Aniline production, potentially unlocking more sustainable and cost-efficient routes. Users also explore how AI can assist in market forecasting, demand sensing, and risk management within complex global supply chains, enabling more agile responses to market fluctuations and geopolitical events. The integration of AI in quality control and impurity detection is another area of focus, aiming to ensure high purity Aniline for demanding applications like MDI production, thereby enhancing product value and reliability.

- AI-driven optimization of Aniline synthesis processes, leading to improved yield and reduced energy consumption.

- Predictive maintenance for manufacturing facilities, minimizing downtime and enhancing operational efficiency.

- Accelerated discovery of novel catalysts and reaction pathways for more sustainable and efficient Aniline production.

- Enhanced supply chain management through AI-powered demand forecasting and logistics optimization.

- Automated quality control and impurity detection systems ensuring higher purity and consistency of Aniline products.

Key Takeaways Aniline Market Size & Forecast

User queries concerning key takeaways from the Aniline market size and forecast consistently highlight the robust growth trajectory, primarily fueled by the burgeoning polyurethane sector and diverse industrial applications. A significant insight is the market's resilience despite raw material price fluctuations, indicating strong underlying demand. The forecast suggests sustained expansion, particularly in emerging economies, driven by rapid industrialization and infrastructure development. This emphasizes the strategic importance of geographical market penetration and capacity expansion in regions like Asia Pacific.

Another crucial takeaway frequently sought by users relates to the increasing emphasis on sustainable production methods and bio-based alternatives. This trend is expected to significantly influence future investment and R&D activities within the industry, steering it towards greener chemical processes. Furthermore, the competitive dynamics, characterized by consolidation and strategic partnerships, underscore the importance of technological differentiation and supply chain integration for market players to maintain and expand their share in a growing yet evolving market landscape.

- The Aniline market exhibits a stable growth outlook, primarily propelled by the expanding polyurethane sector.

- Asia Pacific is anticipated to remain the dominant and fastest-growing region, offering significant investment opportunities.

- Sustainability initiatives and the development of bio-based Aniline are becoming critical drivers of innovation and competitive advantage.

- Market participants are strategically focusing on capacity expansion and backward integration to secure raw material supplies.

- Diversification into new applications beyond MDI, such as specialty chemicals and pharmaceuticals, is a key growth strategy.

Aniline Market Drivers Analysis

The Aniline market's growth is predominantly propelled by the escalating demand from its derivative industries, especially the polyurethane sector. As a foundational chemical, Aniline is integral to the production of Methyl Diphenyl Diisocyanate (MDI), which in turn is a critical component of polyurethanes used extensively in construction, automotive, and furniture industries. Rapid urbanization, infrastructure development, and increasing automotive production globally directly translate into higher demand for polyurethanes, thereby boosting the consumption of Aniline. This robust demand from a well-established and expanding end-use sector forms the primary growth impetus for the Aniline market.

Beyond polyurethanes, the expanding applications of Aniline in other significant sectors further contribute to its market expansion. The rubber processing industry utilizes Aniline derivatives as accelerators and antioxidants, enhancing the durability and performance of rubber products. Growth in the automotive tire manufacturing and industrial rubber goods sectors directly influences this demand. Additionally, its use in the synthesis of agrochemicals, dyes, pigments, and pharmaceuticals provides diversified revenue streams, cushioning the market against fluctuations in any single end-use industry and ensuring a sustained growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Robust Demand for MDI from Polyurethane Industry | +1.5% - +2.0% | Global, particularly APAC, North America, Europe | Short to Long-term (2025-2033) |

| Growth in Automotive and Construction Sectors | +1.0% - +1.5% | Asia Pacific (China, India), North America, Europe | Short to Mid-term (2025-2029) |

| Expanding Applications in Rubber Processing Chemicals | +0.5% - +0.8% | Asia Pacific, Europe, North America | Mid-term (2027-2033) |

| Rising Demand for Specialty Chemicals and Agrochemicals | +0.3% - +0.6% | Global, especially emerging economies | Mid to Long-term (2028-2033) |

| Technological Advancements in Aniline Production | +0.2% - +0.4% | Developed regions (Europe, North America) and China | Long-term (2030-2033) |

Aniline Market Restraints Analysis

The Aniline market faces significant restraints, primarily stemming from the volatility of raw material prices, particularly benzene, which is a key feedstock. Fluctuations in crude oil prices directly impact benzene costs, leading to unpredictable production expenses and challenges in maintaining profit margins for Aniline manufacturers. This price instability can deter new investments and complicate long-term strategic planning, making it difficult for producers to pass on increased costs to end-users without affecting competitiveness. The global geopolitical landscape further exacerbates this volatility, creating an uncertain operational environment.

Environmental regulations and health concerns also pose substantial challenges. Aniline is classified as a toxic substance, and its production and handling are subject to stringent environmental and occupational safety standards across many regions. Compliance with these regulations necessitates significant capital expenditure on pollution control technologies, waste treatment, and safety protocols, which can increase operational costs. Additionally, the public perception and growing awareness about the environmental footprint of chemical manufacturing can lead to increased scrutiny and potential restrictions on production and new plant development.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material (Benzene) Prices | -0.8% - -1.2% | Global | Short to Mid-term (2025-2029) |

| Stringent Environmental Regulations and Health Concerns | -0.5% - -0.9% | Europe, North America, China | Long-term (2027-2033) |

| Oversupply and Price Erosion in Certain Regions | -0.3% - -0.6% | Asia Pacific (specific pockets) | Short-term (2025-2026) |

| High Capital Investment for New Production Facilities | -0.2% - -0.4% | Global | Long-term (2025-2033) |

Aniline Market Opportunities Analysis

The Aniline market is poised for significant opportunities driven by the growing emphasis on sustainable chemistry and the development of bio-based alternatives. As environmental consciousness increases and regulatory pressures for greener chemicals intensify, the research and development into producing Aniline from renewable resources, such as biomass or fermentation processes, presents a lucrative pathway. This innovation not only addresses environmental concerns but also offers a potential hedge against the volatility of fossil fuel-derived raw materials, opening new market segments and attracting environmentally conscious end-users. Investment in this area can provide a significant competitive advantage and long-term market sustainability.

Furthermore, the expansion of end-use industries in emerging economies offers substantial untapped market potential. Rapid industrialization, urbanization, and increasing disposable incomes in regions like Southeast Asia, Latin America, and parts of Africa are fueling demand for products that utilize Aniline derivatives, particularly polyurethanes in construction and automotive. Diversification into niche applications, such as advanced materials, specialized pharmaceuticals, and high-performance polymers, also presents avenues for market expansion. Strategic collaborations, technological advancements, and localized production facilities can enable market players to capitalize on these burgeoning regional demands and specialized product requirements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based Aniline Production | +0.6% - +1.0% | Global, especially Europe, North America, Japan | Mid to Long-term (2028-2033) |

| Expansion in Emerging Economies (APAC, LATAM, MEA) | +0.8% - +1.2% | China, India, Brazil, ASEAN Countries | Short to Long-term (2025-2033) |

| Increasing Demand from Niche and High-Value Applications | +0.4% - +0.7% | Global (developed countries primarily) | Mid-term (2027-2031) |

| Technological Innovations for Enhanced Purity & Efficiency | +0.3% - +0.5% | Global | Long-term (2030-2033) |

Aniline Market Challenges Impact Analysis

The Aniline market faces persistent challenges related to the stringent regulatory landscape and the need for significant capital investment in compliance and production upgrades. As a regulated chemical, Aniline production and usage are subject to evolving environmental, health, and safety (EHS) regulations globally. Adhering to these complex and often varying standards across different regions demands continuous investment in advanced pollution control technologies, process safety measures, and extensive monitoring, which can strain operational budgets and impact profitability, especially for smaller manufacturers. Furthermore, any failure to comply can lead to hefty fines, production halts, and reputational damage.

Another critical challenge is the intense competition and potential for oversupply in key production regions, particularly in Asia Pacific where significant capacity expansions have occurred. This can lead to downward pressure on prices and squeezed profit margins, making it difficult for manufacturers to differentiate their products solely on price. Geopolitical instabilities and trade disputes also pose a significant challenge by disrupting established supply chains, increasing logistics costs, and creating uncertainty in export markets. Managing these external factors requires robust risk management strategies and diversified market access to ensure business continuity and sustained growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental & Safety Regulations | -0.7% - -1.1% | Europe, North America, China | Long-term (2025-2033) |

| Intense Competition and Potential Oversupply | -0.4% - -0.8% | Asia Pacific (China), Europe | Short to Mid-term (2025-2029) |

| Supply Chain Disruptions & Geopolitical Instability | -0.3% - -0.6% | Global | Short to Mid-term (2025-2028) |

| High Energy Consumption in Production Processes | -0.2% - -0.4% | Global | Long-term (2025-2033) |

Aniline Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Aniline market, offering critical insights into its current size, historical performance, and future growth projections. It covers key market dynamics, including drivers, restraints, opportunities, and challenges, along with a detailed impact analysis of each factor. The scope encompasses a thorough examination of market segmentation by application, end-use industry, manufacturing process, and grade, providing a granular view of the market landscape. Furthermore, the report delves into regional market trends and competitive landscape analysis, profiling key industry players and their strategic initiatives, ensuring a holistic understanding for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 11.5 Billion |

| Market Forecast in 2033 | USD 16.8 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Covestro AG, BASF SE, Wanhua Chemical Group Co. Ltd., Huntsman Corporation, Dow Chemical Company, Mitsui Chemicals Inc., Sumitomo Chemical Co., Ltd., Tosoh Corporation, VCI Chemical Industries, Ltd., Gujarat Alkalies and Chemicals Limited, Hindustan Organic Chemicals Limited, Jilin Connell Chemical Industry Co., Ltd., Shandong Jinying Chemical Co., Ltd., Kothari Pharma, China National Bluestar (Group) Co., Ltd., Liaoning North Aniline Chemical Co., Ltd., Volzhsky Orgsynthese JSC, Monument Chemical, Axiall Corporation (Westlake Chemical Corporation), Chematur Engineering AB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aniline market is intricately segmented to provide a granular understanding of its diverse applications, end-use industries, and production methodologies. This segmentation allows for precise market sizing and forecasting, identifying key growth pockets and strategic areas for investment. The primary segments include application types such as MDI, rubber processing chemicals, dyes and pigments, pharmaceuticals, and agrochemicals, each driving demand from distinct industrial sectors. Understanding these segments helps in assessing the specific market dynamics influencing demand for different grades and purities of Aniline.

Further segmentation by end-use industry, including construction, automotive, furniture, footwear, and agriculture, highlights the broad utility of Aniline across foundational global industries. The analysis also covers manufacturing processes, predominantly the hydrogenation of nitrobenzene, and distinguishes between various Aniline grades such as polymeric MDI grade and pure MDI grade, which are crucial for specialized applications. This detailed breakdown offers comprehensive insights into the market structure and the interdependencies between Aniline production and its extensive value chain.

- By Application:

- MDI (Methyl Diphenyl Diisocyanate)

- Rubber Processing Chemicals

- Dyes and Pigments

- Pharmaceuticals

- Agrochemicals

- Explosives

- Others

- By End-Use Industry:

- Construction

- Automotive

- Furniture & Bedding

- Footwear

- Electrical & Electronics

- Agriculture

- Rubber Industry

- Others

- By Manufacturing Process:

- Hydrogenation of Nitrobenzene

- Others

- By Grade:

- Polymeric MDI Grade Aniline

- Pure MDI Grade Aniline

- Other Grades

Regional Highlights

The Aniline market exhibits distinct regional dynamics, with Asia Pacific standing out as the dominant and fastest-growing region. This robust growth is primarily attributable to rapid industrialization, burgeoning construction activities, and the booming automotive sector in countries like China and India. These nations are significant manufacturing hubs for polyurethanes and other Aniline derivatives, driven by large domestic markets and strong export capabilities. Government initiatives supporting infrastructure development and industrial expansion further contribute to the region's strong demand for Aniline.

North America and Europe represent mature markets for Aniline, characterized by established end-use industries and stringent environmental regulations. While growth rates may be more moderate compared to Asia Pacific, these regions focus on high-performance applications, specialty chemicals, and sustainable production methods. Innovation in bio-based Aniline and advanced material science is more prevalent here, influencing global market trends. Latin America and the Middle East & Africa regions are emerging markets, showing gradual growth influenced by economic development, urbanization, and increasing industrial output, particularly in construction and automotive sectors. These regions present future opportunities for capacity expansion and market penetration as their industrial bases continue to develop.

- Asia Pacific: Dominant market share and highest growth rate due to rapid industrialization, robust construction, and expanding automotive industries in China, India, and ASEAN countries. Significant capacity expansions and lower production costs.

- North America: Mature market with stable demand, driven by well-established automotive, construction, and rubber industries. Focus on specialty applications and increasing adoption of sustainable practices.

- Europe: Key market with strong emphasis on regulatory compliance and sustainable production. Demand is driven by automotive, construction, and furniture sectors, with a growing focus on circular economy principles and bio-based solutions.

- Latin America: Emerging market demonstrating steady growth, fueled by urbanization, infrastructure development, and expanding automotive production in countries like Brazil and Mexico.

- Middle East & Africa (MEA): Gradually growing market, influenced by investments in infrastructure, diversification of economies beyond oil, and development of local manufacturing capabilities in countries like Saudi Arabia and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aniline Market.- Covestro AG

- BASF SE

- Wanhua Chemical Group Co. Ltd.

- Huntsman Corporation

- Dow Chemical Company

- Mitsui Chemicals Inc.

- Sumitomo Chemical Co., Ltd.

- Tosoh Corporation

- VCI Chemical Industries, Ltd.

- Gujarat Alkalies and Chemicals Limited

- Hindustan Organic Chemicals Limited

- Jilin Connell Chemical Industry Co., Ltd.

- Shandong Jinying Chemical Co., Ltd.

- Kothari Pharma

- China National Bluestar (Group) Co., Ltd.

- Liaoning North Aniline Chemical Co., Ltd.

- Volzhsky Orgsynthese JSC

- Monument Chemical

- Axiall Corporation (Westlake Chemical Corporation)

- Chematur Engineering AB

Frequently Asked Questions

Analyze common user questions about the Aniline market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Aniline market?

The Aniline market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033, reaching an estimated USD 16.8 billion by the end of the forecast period.

Which factors are primarily driving the Aniline market growth?

The market's growth is primarily driven by the robust demand for Methyl Diphenyl Diisocyanate (MDI) from the polyurethane industry, coupled with expanding applications in rubber processing chemicals, agrochemicals, and specialty polymers.

What are the main applications of Aniline?

Aniline is predominantly used in the production of Methyl Diphenyl Diisocyanate (MDI) for polyurethanes, followed by significant applications in rubber processing chemicals, dyes and pigments, pharmaceuticals, and agrochemicals.

Which region is expected to dominate the Aniline market?

Asia Pacific is anticipated to remain the dominant and fastest-growing region in the Aniline market, driven by rapid industrialization, robust construction, and expanding automotive industries in countries like China and India.

What are the key challenges facing the Aniline market?

Key challenges include the volatile prices of raw materials such as benzene, stringent environmental and safety regulations, intense competition leading to potential oversupply, and the high capital investment required for new production facilities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted