Acetone Market

Acetone Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702285 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Acetone Market Size

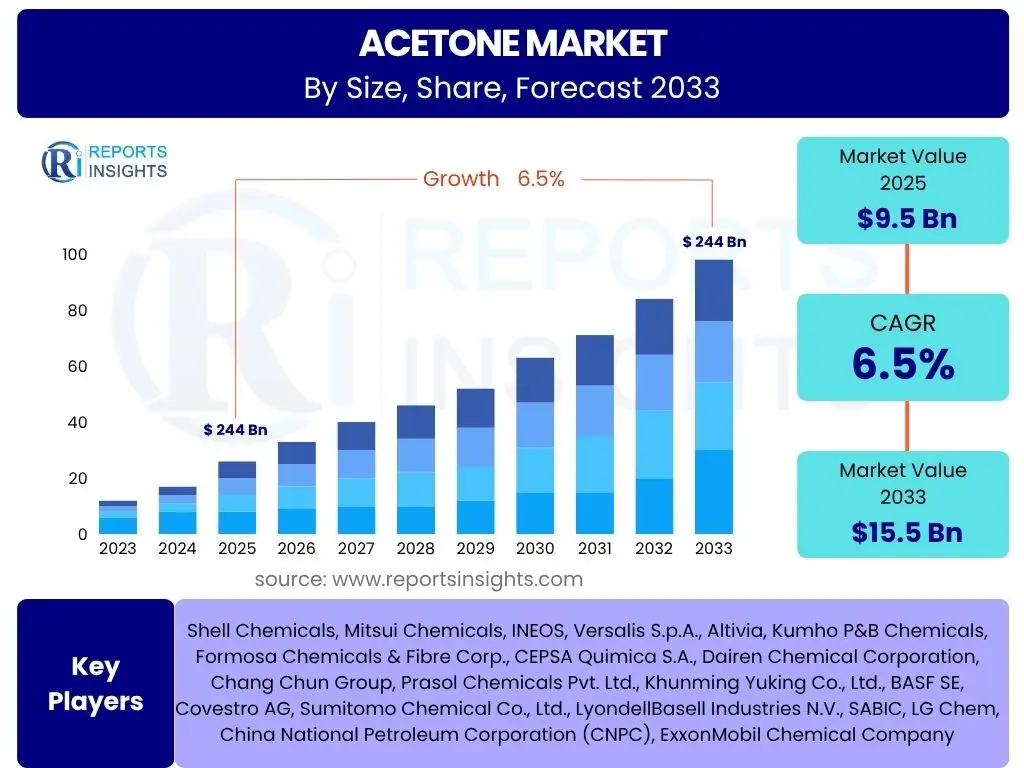

According to Reports Insights Consulting Pvt Ltd, The Acetone Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 9.5 Billion in 2025 and is projected to reach USD 15.5 Billion by the end of the forecast period in 2033.

Key Acetone Market Trends & Insights

The acetone market is currently shaped by several significant trends, reflecting shifts in both supply and demand dynamics globally. A prominent trend involves the increasing adoption of bio-based acetone, driven by growing environmental consciousness and stringent regulations aimed at reducing reliance on petrochemicals. This movement towards sustainable production methods is attracting investments in research and development, particularly in regions with strong governmental support for green chemistry initiatives. Furthermore, the expansion of the automotive and construction sectors, especially in emerging economies, continues to fuel demand for acetone derivatives like Methyl Methacrylate (MMA) and Bisphenol A (BPA), crucial components in plastics, coatings, and adhesives.

Another key insight is the evolving landscape of end-use applications. While traditional uses in paints, coatings, and solvents remain robust, there is an emerging trend of acetone being utilized in novel applications, such as in the formulation of high-performance resins and advanced composite materials. The pharmaceutical and cosmetics industries also present expanding avenues for acetone, driven by global population growth and increasing healthcare expenditure, which necessitates high-purity solvents for various manufacturing processes. The market is also observing a consolidation among key players and an emphasis on backward integration to secure raw material supplies, aiming to mitigate price volatility and enhance operational efficiencies.

Geographically, Asia Pacific continues to dominate the market due to rapid industrialization, particularly in China and India, alongside significant investments in manufacturing capabilities. However, North America and Europe are focusing on technological advancements and regulatory compliance, driving innovation in sustainable production and high-value applications. The interplay of these regional dynamics, coupled with global economic shifts, will continue to define the market's trajectory, emphasizing efficiency, sustainability, and diversification of end-use industries.

- Increasing adoption of bio-based acetone and sustainable production methods.

- Growing demand from automotive and construction sectors for MMA and BPA.

- Expansion of acetone applications in high-performance resins and composites.

- Rising consumption in the pharmaceutical and cosmetics industries.

- Strategic emphasis on backward integration and supply chain optimization by key manufacturers.

- Dominance of Asia Pacific due to rapid industrialization and manufacturing growth.

- Focus on technological innovation and regulatory compliance in developed markets.

AI Impact Analysis on Acetone

Artificial Intelligence (AI) is beginning to exert a transformative influence on various facets of the acetone value chain, primarily through enhanced operational efficiency and predictive capabilities. Users frequently inquire about how AI can optimize production processes, reduce energy consumption, and improve product quality in chemical manufacturing. AI-driven algorithms can analyze vast datasets from plant operations, including temperature, pressure, and flow rates, to identify optimal parameters for acetone synthesis, leading to higher yields and reduced waste. This data-driven approach allows for real-time adjustments, minimizing off-spec production and optimizing energy utilization, directly impacting operational costs and environmental footprint.

Furthermore, AI plays a crucial role in supply chain management and demand forecasting for acetone. Companies are exploring AI solutions to predict market fluctuations, anticipate raw material shortages, and optimize logistics, thereby ensuring a stable supply of acetone to various industries. By integrating external factors such as economic indicators, industry growth rates, and even social media sentiment, AI models can provide more accurate demand forecasts than traditional methods. This predictive power helps manufacturers and distributors to optimize inventory levels, reduce storage costs, and respond more agilely to market changes, mitigating risks associated with volatile raw material prices and global supply disruptions.

While the adoption of AI in the acetone market is still in its nascent stages, the potential for significant gains in efficiency, sustainability, and profitability is substantial. Concerns often revolve around the initial investment costs for AI infrastructure, the availability of skilled personnel to manage and interpret AI systems, and data security. However, as AI technologies mature and become more accessible, their integration is expected to become a competitive imperative, driving innovation in process optimization, quality control, and strategic decision-making across the acetone industry.

- AI optimizes acetone production parameters for higher yields and reduced waste.

- Real-time process adjustments driven by AI enhance energy efficiency and quality control.

- AI improves supply chain efficiency and demand forecasting, mitigating market volatility.

- Predictive analytics aid in optimizing inventory and logistics for acetone distribution.

- Potential for significant operational cost reductions and environmental benefits.

- Challenges include initial investment, skilled workforce requirements, and data security.

Key Takeaways Acetone Market Size & Forecast

The acetone market is poised for sustained growth through 2033, driven by its versatile applications across diverse industries and the increasing shift towards sustainable production methods. A key takeaway from the market forecast is the strong correlation between economic growth in emerging economies and the escalating demand for acetone derivatives, particularly in the construction, automotive, and packaging sectors. The anticipated expansion of these industries, especially in Asia Pacific, will be a primary catalyst for market volume and value expansion. Furthermore, the sustained demand from the pharmaceutical and cosmetics industries for high-purity acetone continues to provide a stable foundation for market growth, emphasizing the importance of quality and regulatory compliance in these segments.

Another critical insight is the growing emphasis on bio-based and green chemistry initiatives, which is expected to significantly influence market dynamics. As environmental regulations tighten and consumer preferences shift towards eco-friendly products, manufacturers are increasingly investing in sustainable acetone production technologies. This trend is not merely a compliance measure but also an opportunity for innovation and differentiation, potentially attracting new investments and fostering technological advancements that could reshape the competitive landscape. The market will likely see a greater diversification of supply sources and production methods, moving beyond traditional petrochemical reliance.

The forecast also highlights the ongoing need for strategic raw material sourcing and supply chain resilience. Volatility in crude oil prices and geopolitical factors can impact feedstock costs, necessitating robust procurement strategies. Companies that can effectively manage these external pressures, while simultaneously investing in R&D for new applications and sustainable processes, are best positioned to capitalize on the projected market expansion. The long-term outlook for acetone remains positive, underpinned by its essential role in numerous industrial processes and the continuous innovation within its application spectrum.

- Acetone market projected for consistent growth, fueled by diverse applications.

- Emerging economies, particularly Asia Pacific, will drive significant demand.

- Construction, automotive, and packaging sectors are key growth engines.

- Pharmaceutical and cosmetics industries provide stable demand for high-purity acetone.

- Increasing focus on bio-based acetone and green chemistry for sustainable growth.

- Strategic raw material sourcing and supply chain resilience are crucial for market stability.

- Continuous innovation in applications and production methods will sustain long-term market vitality.

Acetone Market Drivers Analysis

The global acetone market is fundamentally driven by robust demand from its varied end-use industries, which utilize acetone as a crucial solvent or chemical intermediate. The rapid expansion of the construction sector, particularly in developing nations, significantly boosts the demand for paints, coatings, and adhesives, all of which contain acetone. Similarly, the burgeoning automotive industry, driven by increasing vehicle production and the demand for lightweight materials, relies heavily on acetone for manufacturing plastics, composites, and specialized coatings. The versatile chemical properties of acetone make it indispensable across these high-growth sectors, ensuring a continuous uptake and contributing to market expansion.

Furthermore, the pharmaceutical and cosmetics industries represent significant and steadily growing markets for acetone. In pharmaceuticals, acetone is a preferred solvent for drug synthesis, purification processes, and the manufacture of various excipients, driven by increasing global healthcare expenditure and the development of new drug formulations. For cosmetics, it serves as a solvent in nail polish removers, fragrances, and other beauty products, benefiting from rising consumer discretionary income and evolving beauty trends. The stringent quality requirements in these industries also support the demand for high-purity acetone, influencing production standards and market value.

Technological advancements in acetone production, including more efficient and sustainable processes like the cumene process, also act as a driver by ensuring a cost-effective and environmentally sound supply. The rising adoption of Methyl Methacrylate (MMA) and Bisphenol A (BPA) in various applications, such as polycarbonate plastics and epoxy resins, further cements acetone's market position. These derivatives are vital for industries ranging from electronics to packaging, reflecting a broad base of demand that continues to expand with industrialization and urbanization globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from construction and automotive industries | +1.8% | Asia Pacific, North America, Europe | 2025-2033 |

| Expansion of pharmaceutical and cosmetics sectors | +1.5% | Global, particularly developed economies | 2025-2033 |

| Increased production of MMA and BPA | +1.2% | Asia Pacific, Europe | 2025-2033 |

| Advancements in sustainable acetone production technologies | +0.9% | Europe, North America | 2027-2033 |

| Rising demand for solvent applications in diverse industries | +0.7% | Global | 2025-2033 |

Acetone Market Restraints Analysis

Despite robust demand, the acetone market faces several significant restraints that could impede its growth trajectory. One primary concern is the volatility in raw material prices, particularly of propylene and benzene, which are key feedstocks for acetone production via the cumene process. Fluctuations in crude oil prices directly impact the cost of these petrochemical derivatives, leading to unpredictable production costs for acetone manufacturers. This price instability can squeeze profit margins and make long-term planning challenging, particularly for smaller market players who may lack the hedging capabilities of larger corporations. Such volatility can also deter new investments in production capacity.

Another critical restraint is the increasing regulatory scrutiny and environmental concerns surrounding the production and use of acetone. As governments worldwide implement stricter environmental protection laws, particularly concerning volatile organic compound (VOC) emissions, manufacturers are compelled to invest in costly abatement technologies and adhere to complex compliance standards. While these regulations promote safer and more sustainable practices, they also add to operational expenses and may limit the use of acetone in certain applications or regions. The push for green chemistry and sustainable alternatives further encourages the development of substitute solvents, potentially cannibalizing acetone's market share in some segments.

The availability and rising costs of energy, essential for the energy-intensive chemical production processes, also pose a restraint. Geopolitical tensions and supply chain disruptions can exacerbate these energy price spikes, directly impacting the economic viability of acetone manufacturing. Furthermore, competition from alternative solvents and technologies, especially in paints, coatings, and adhesives, where bio-based or water-based alternatives are gaining traction, presents a long-term challenge. These alternatives, though sometimes less efficient, appeal to environmentally conscious consumers and industries, gradually eroding acetone's market dominance in specific niches.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile raw material (propylene, benzene) prices | -1.5% | Global | 2025-2033 |

| Stringent environmental regulations on VOC emissions | -1.2% | Europe, North America, parts of Asia | 2025-2033 |

| Competition from alternative solvents and bio-based products | -1.0% | Global | 2026-2033 |

| Rising energy costs and supply chain disruptions | -0.8% | Global | 2025-2029 |

| Oversupply situations leading to price erosion | -0.5% | Asia Pacific | 2025-2028 |

Acetone Market Opportunities Analysis

The acetone market is presented with significant opportunities, primarily driven by the burgeoning demand for sustainable and high-performance materials. The growing global emphasis on reducing carbon footprints and adopting circular economy principles creates a strong impetus for the development and commercialization of bio-based acetone. Investments in biotechnological pathways for acetone production from renewable feedstocks like biomass or agricultural waste offer a compelling alternative to petrochemical-based processes. This shift not only addresses environmental concerns but also diversifies the supply chain, reducing reliance on volatile fossil fuel markets and opening new market segments focused on green products. Early movers in this space are poised to capture a substantial share of future demand, driven by corporate sustainability goals and consumer preferences.

Emerging applications in advanced materials and new industrial processes also present considerable growth avenues. For instance, the increasing use of acetone in the production of high-performance polymers, composites for aerospace and automotive lightweighting, and specialized chemicals for the electronics industry reflects a diversification beyond traditional solvent roles. Research into using acetone in novel energy storage solutions, such as electrolytes in batteries, could unlock entirely new, high-value markets. Furthermore, the expansion of the pharmaceutical and fine chemical industries, particularly in developing economies, continuously creates demand for high-purity acetone as a reaction medium, extraction solvent, and purification agent, driven by increasing healthcare needs and scientific advancements.

Geographically, untapped and expanding markets, particularly in rapidly industrializing regions of Southeast Asia, Latin America, and Africa, offer substantial opportunities for market penetration. As these regions experience economic development, infrastructure expansion, and rising consumer spending, the demand for products that utilize acetone, such as construction materials, automotive components, and consumer goods, is set to surge. Strategic investments in local production facilities or robust distribution networks in these areas can help companies capitalize on this growth. Moreover, the integration of advanced analytics and AI in production and supply chain management could lead to optimized operations, cost reductions, and improved market responsiveness, further enhancing profitability and market competitiveness for acetone producers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and adoption of bio-based acetone | +1.7% | Global, particularly Europe & North America | 2027-2033 |

| Expansion into new applications like advanced materials | +1.4% | Global | 2026-2033 |

| Growth in emerging markets (Southeast Asia, Latin America) | +1.1% | Southeast Asia, Latin America, Africa | 2025-2033 |

| Increased demand from high-growth pharmaceutical and fine chemical sectors | +0.9% | Global | 2025-2033 |

| Integration of AI and digital technologies for optimized operations | +0.6% | Global | 2028-2033 |

Acetone Market Challenges Impact Analysis

The acetone market, while promising, faces several inherent challenges that can significantly influence its growth trajectory. One key challenge is the intense competition from alternative products and solvents, which continually evolve to meet specific industrial needs or comply with environmental mandates. For example, in the coatings and adhesives sectors, there is a growing preference for water-based or low-VOC formulations, which reduces the reliance on traditional organic solvents like acetone. This trend forces acetone manufacturers to innovate and find new, high-value applications or risk losing market share in mature segments. The development of greener alternatives, while a positive step for the environment, directly competes with established acetone uses.

Supply chain disruptions and geopolitical uncertainties also pose a substantial challenge to the stability and pricing of acetone. Being primarily derived from petrochemicals, acetone production is vulnerable to volatility in crude oil prices, which directly impacts the cost of propylene and benzene. Furthermore, regional conflicts, trade disputes, or natural disasters can disrupt the flow of raw materials or finished products, leading to price spikes or supply shortages. Such external factors are largely beyond the control of individual manufacturers and necessitate robust risk management strategies and diversified sourcing. The globalized nature of the chemical industry means that local disruptions can have far-reaching effects on acetone supply and demand.

Another significant challenge is managing the environmental and health and safety implications associated with acetone production and handling. While acetone is widely used, it is flammable and requires careful storage, transportation, and disposal. Stricter global regulations on industrial emissions, waste management, and workplace safety compel manufacturers to invest heavily in advanced technologies for pollution control and safety protocols, increasing operational costs. The public perception of chemical products and the potential for negative publicity further pressure companies to adopt environmentally responsible practices and transparent reporting. Balancing the economic viability of production with increasingly rigorous environmental and safety standards remains a constant challenge for the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from substitute chemicals and greener alternatives | -1.3% | Global | 2025-2033 |

| Supply chain vulnerabilities and geopolitical risks impacting feedstock | -1.1% | Global | 2025-2029 |

| Adherence to stringent environmental, health, and safety regulations | -0.9% | Developed economies, increasingly emerging markets | 2025-2033 |

| High energy consumption in the production process | -0.7% | Global | 2025-2033 |

| Risk of overcapacity leading to price erosion in specific regions | -0.4% | Asia Pacific | 2025-2027 |

Acetone Market - Updated Report Scope

This report provides a comprehensive analysis of the global acetone market, offering a detailed understanding of its current size, historical performance, and future growth projections. It delves into the underlying market dynamics, including key drivers, restraints, opportunities, and challenges that shape the industry landscape. The scope encompasses a thorough examination of market segmentation by application, grade, and end-use industry, providing granular insights into the various revenue streams and growth pockets. Furthermore, it highlights regional market performance, identifying key countries and their respective contributions to the global market, alongside an in-depth competitive analysis of leading market players.

The report's updated scope also integrates the impact of emerging trends and technologies, such as the rise of bio-based acetone and the influence of Artificial Intelligence (AI) on production efficiencies and supply chain management. It offers strategic insights designed to assist stakeholders, including manufacturers, investors, and policymakers, in making informed decisions. The data presented is meticulously gathered and validated, ensuring accuracy and reliability for strategic planning and competitive intelligence. This holistic view aims to equip market participants with the necessary knowledge to navigate the complexities of the acetone market and capitalize on future opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 9.5 Billion |

| Market Forecast in 2033 | USD 15.5 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Shell Chemicals, Mitsui Chemicals, INEOS, Versalis S.p.A., Altivia, Kumho P&B Chemicals, Formosa Chemicals & Fibre Corp., CEPSA Quimica S.A., Dairen Chemical Corporation, Chang Chun Group, Prasol Chemicals Pvt. Ltd., Khunming Yuking Co., Ltd., BASF SE, Covestro AG, Sumitomo Chemical Co., Ltd., LyondellBasell Industries N.V., SABIC, LG Chem, China National Petroleum Corporation (CNPC), ExxonMobil Chemical Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The acetone market is segmented to provide a granular understanding of its diverse applications, quality requirements, and end-use industries, which collectively define its demand landscape. By segmenting the market based on application, we analyze the primary uses of acetone, such as its crucial role as a solvent in various industries, a chemical intermediate in the production of other compounds, and specifically for synthesizing Methyl Methacrylate (MMA) and Bisphenol A (BPA). This breakdown highlights the specific demand drivers and growth patterns associated with each application, enabling stakeholders to identify high-potential areas and tailor their strategies accordingly. The dominance of MMA and BPA production underscores acetone's significance in polymer and plastic manufacturing, reflecting broader trends in construction, automotive, and electronics industries.

Further segmentation by grade, primarily into Technical Grade and Pharmaceutical Grade, distinguishes between the varying purity requirements across different end-uses. Technical grade acetone, being less pure, is typically used in industrial applications such as paints, coatings, and adhesives, where stringent purity is not paramount. Conversely, Pharmaceutical Grade acetone, characterized by its high purity, is indispensable in the pharmaceutical, cosmetics, and food industries for drug synthesis, extraction, and formulation, where product integrity and safety are critical. This distinction in grades influences production processes, pricing, and distribution channels, catering to specialized market demands and regulatory compliance.

The end-use industry segmentation offers insights into which sectors are the primary consumers of acetone, including automotive, construction, packaging, paints & coatings, pharmaceuticals, cosmetics, adhesives, and agriculture. Each industry's growth trajectory directly impacts the demand for acetone, influenced by economic conditions, consumer trends, and regulatory changes within that specific sector. For instance, robust growth in global construction directly translates to increased demand for acetone in paints and glues, while advancements in pharmaceuticals drive the need for high-purity solvents. This detailed segmentation allows for a comprehensive assessment of market dynamics, competitive positioning, and future growth opportunities across the acetone value chain.

- By Application:

- Solvents

- Chemical Intermediates

- Methyl Methacrylate (MMA)

- Bisphenol A (BPA)

- Others (e.g., pharmaceuticals, cosmetics, agriculture)

- By Grade:

- Technical Grade

- Pharmaceutical Grade

- By End-Use Industry:

- Automotive

- Construction

- Packaging

- Paints & Coatings

- Pharmaceuticals

- Cosmetics

- Adhesives

- Agriculture

Regional Highlights

- Asia Pacific: This region is projected to maintain its dominant position in the acetone market, driven by rapid industrialization, burgeoning manufacturing sectors, and robust growth in end-use industries like construction, automotive, and electronics, particularly in China and India. The region benefits from substantial investments in chemical production capacities and increasing domestic consumption.

- North America: Characterized by technological advancements and a strong focus on research and development, North America shows steady demand for acetone, particularly in the pharmaceutical, automotive, and aerospace industries. The region is increasingly adopting sustainable production methods and high-purity acetone for specialized applications.

- Europe: Europe is a mature market focusing on innovation, regulatory compliance, and sustainability. Demand for acetone is driven by the robust automotive, construction, and pharmaceutical sectors. Strict environmental regulations here also encourage the development and adoption of bio-based acetone and low-VOC formulations.

- Latin America: This region is an emerging market for acetone, with growth driven by infrastructure development, expanding industrial bases, and rising consumer spending in countries like Brazil and Mexico. The demand is primarily from the paints & coatings, construction, and automotive industries.

- Middle East & Africa (MEA): The MEA region is expected to experience growth due to ongoing industrial diversification efforts, increasing investments in petrochemical industries, and expanding construction activities. Countries with significant oil and gas reserves are also exploring downstream chemical production, contributing to acetone demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Acetone Market.- Shell Chemicals

- Mitsui Chemicals

- INEOS

- Versalis S.p.A.

- Altivia

- Kumho P&B Chemicals

- Formosa Chemicals & Fibre Corp.

- CEPSA Quimica S.A.

- Dairen Chemical Corporation

- Chang Chun Group

- Prasol Chemicals Pvt. Ltd.

- Khunming Yuking Co., Ltd.

- BASF SE

- Covestro AG

- Sumitomo Chemical Co., Ltd.

- LyondellBasell Industries N.V.

- SABIC

- LG Chem

- China National Petroleum Corporation (CNPC)

- ExxonMobil Chemical Company

Frequently Asked Questions

What is Acetone primarily used for?

Acetone is primarily used as a solvent in various industries and as a chemical intermediate for producing other chemicals like Methyl Methacrylate (MMA) and Bisphenol A (BPA). Its applications span paints, coatings, adhesives, pharmaceuticals, and cosmetics.

Which regions are driving the growth of the Acetone market?

The Asia Pacific region, particularly countries like China and India, is a primary driver of the Acetone market growth due to rapid industrialization, strong manufacturing bases, and increasing demand from the automotive and construction sectors.

What are the key trends shaping the Acetone industry?

Key trends include a growing shift towards bio-based acetone production for sustainability, increasing demand from the automotive and construction industries for derived products, and expanding applications in the pharmaceutical and cosmetics sectors.

How do raw material prices impact the Acetone market?

Volatility in raw material prices, specifically propylene and benzene, significantly impacts the production costs of acetone. Fluctuations can squeeze profit margins for manufacturers and influence overall market stability and pricing.

What are the major challenges faced by Acetone manufacturers?

Major challenges include intense competition from alternative solvents, the impact of volatile raw material prices, stringent environmental regulations on emissions, and the need to manage complex supply chain dynamics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted