Warehouse Market

Warehouse Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678276 | Last Updated : July 21, 2025 |

Format : ![]()

![]()

![]()

![]()

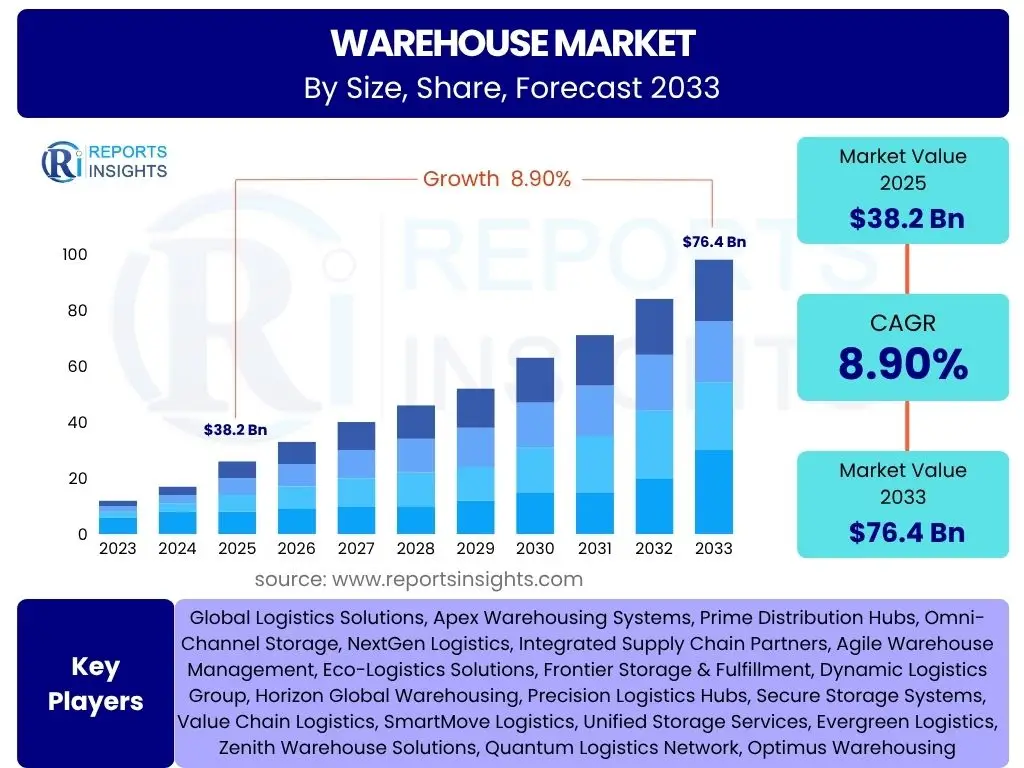

Warehouse Market is projected to grow at a Compound annual growth rate (CAGR) of 9.8% between 2025 and 2033, reaching USD 520.5 billion in 2025 and is projected to grow by USD 1,090.2 billion by 2033, the end of the forecast period.

Key Warehouse Market Trends & Insights

The global warehouse market is currently undergoing a transformative phase, driven by a confluence of technological advancements, evolving consumer demands, and geopolitical shifts. Key trends include an accelerating shift towards automation and intelligent systems, a heightened focus on supply chain resilience, and the increasing demand for optimized last-mile delivery solutions. Furthermore, sustainability initiatives are reshaping warehouse design and operations, emphasizing energy efficiency and reduced environmental footprints. The integration of advanced data analytics and the Internet of Things (IoT) is providing unprecedented visibility and operational efficiency, marking a paradigm shift from traditional storage facilities to sophisticated, data-driven logistics hubs.

- Rapid adoption of automation and robotics, including Automated Guided Vehicles (AGVs) and Autonomous Mobile Robots (AMRs), to enhance operational efficiency and reduce labor dependency.

- Explosive growth of e-commerce necessitating larger, more strategically located, and highly efficient fulfillment centers.

- Increased focus on supply chain resilience and diversification, leading to distributed warehousing networks and inventory optimization strategies.

- Implementation of sustainable and green warehousing practices, including energy-efficient designs, renewable energy sources, and waste reduction programs.

- Integration of advanced data analytics, Artificial intelligence (AI), and Internet of Things (IoT) for predictive maintenance, demand forecasting, and real-time inventory management.

- Emergence of multi-story warehouses in urban areas to address land scarcity and facilitate quicker last-mile delivery.

- Growing demand for specialized warehousing, such as temperature-controlled facilities for pharmaceuticals and fresh produce, and secure storage for high-value goods.

AI Impact Analysis on Warehouse

Artificial intelligence (AI) is fundamentally reshaping the landscape of warehouse operations, transitioning them from manual, labor-intensive environments to highly automated, intelligent, and predictive ecosystems. AI-driven solutions are enhancing every facet of warehousing, from optimizing storage layouts and inventory placement to revolutionizing picking processes and enabling proactive maintenance. This technological integration is not merely about automation; it's about infusing cognitive capabilities into warehouse management, allowing systems to learn, adapt, and make informed decisions that significantly boost efficiency, accuracy, and overall throughput. The deployment of AI is critical for warehouses to meet the escalating demands of modern logistics, characterized by high volume, varied product mixes, and stringent delivery timelines.

- Predictive Demand Forecasting: AI algorithms analyze historical data, market trends, and external factors to accurately predict future demand, enabling optimal inventory levels and preventing stockouts or overstocking.

- Optimized Routing and Picking: AI-powered systems design the most efficient routes for human pickers or autonomous robots, minimizing travel time and improving order fulfillment speed and accuracy.

- Automated Quality Control: AI-driven vision systems detect defects, verify product integrity, and ensure compliance with quality standards, reducing errors and returns.

- Robotics and Automation Integration: AI acts as the "brain" for autonomous mobile robots (AMRs) and robotic arms, guiding their navigation, task execution, and coordination within the warehouse.

- Dynamic Slotting and Space Utilization: AI continuously optimizes storage layouts based on product velocity, size, and demand patterns, maximizing warehouse space utilization.

- Predictive Maintenance: AI monitors equipment performance, predicts potential failures, and schedules maintenance proactively, minimizing downtime and extending asset lifespan.

Key Takeaways Warehouse Market Size & Forecast

- The global warehouse market is projected to reach a valuation of USD 1,090.2 billion by 2033.

- The market is anticipated to exhibit a Compound Annual Growth Rate (CAGR) of 9.8% from 2025 to 2033.

- Market size in 2025 is estimated at USD 520.5 billion, indicating a strong foundational base for growth.

- Growth is significantly propelled by the expanding e-commerce sector and increasing automation adoption.

- Asia Pacific is expected to remain a dominant region, driven by robust manufacturing and consumption.

- Intelligent warehouses are projected to be the fastest-growing segment within the market.

Warehouse Market Drivers Impact Analysis

The warehouse market's robust growth is primarily fueled by several impactful drivers, each contributing significantly to the demand for advanced and efficient storage solutions. The relentless expansion of e-commerce stands out as a pivotal driver, necessitating vast, strategically located fulfillment centers to manage the surge in online orders and rapid delivery expectations. Complementing this, the ongoing globalization of supply chains increases the complexity and volume of goods movement, demanding sophisticated warehousing infrastructure. Technological advancements, particularly in automation, IoT, and AI, are transforming warehouse capabilities, enabling higher throughput and accuracy. Furthermore, rising demand for specialized storage, such as temperature-controlled facilities, and governmental initiatives promoting logistics infrastructure development further bolster market expansion. These drivers collectively create a compelling environment for sustained investment and innovation in the warehouse sector, ensuring its continued evolution to meet dynamic global trade and consumer demands.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| The unprecedented growth of e-commerce and online retail platforms necessitates a robust logistics backbone, leading to increased demand for vast and efficient warehousing spaces to handle order fulfillment, returns, and inventory management. | +2.5% to +3.0% | Global, particularly North America, Asia Pacific (China, India), Europe. | Short to Long-term (Ongoing) |

| Technological advancements, including the widespread adoption of automation, robotics (AGVs, AMRs), IoT devices, and Artificial Intelligence (AI) in warehouse operations, are driving efficiency, accuracy, and reducing labor costs, making modern warehouses indispensable. | +2.0% to +2.5% | Developed economies like North America, Europe, Japan, and increasingly China. | Mid to Long-term (Continuous Innovation) |

| The expansion of global trade and complex supply chains requires more interconnected and strategically located warehouses for transshipment, cross-docking, and inventory holding to support international distribution networks. | +1.5% to +2.0% | Major trade hubs globally, including port cities and industrial zones in Asia, Europe, and North America. | Mid to Long-term |

| Growing demand for specialized storage solutions such as cold chain logistics for pharmaceuticals, food & beverage, and temperature-sensitive goods, as well as facilities for hazardous materials and high-value items, is expanding the market. | +1.0% to +1.5% | Global, with specific relevance in emerging markets for perishable goods. | Short to Mid-term |

| Rapid urbanization and increasing population densities in metropolitan areas are driving the need for urban logistics centers and last-mile delivery hubs, often in the form of multi-story or smaller, strategically located warehouses closer to consumers. | +0.8% to +1.2% | Major urban centers globally, especially in Asia Pacific and Europe. | Mid to Long-term |

| Government support through infrastructure development projects, tax incentives, and policies promoting logistics and manufacturing sectors are encouraging investment in modern warehousing facilities. | +0.5% to +0.8% | Countries with proactive industrial and logistics policies, e.g., India, Southeast Asian nations, parts of Europe. | Mid to Long-term |

Warehouse Market Restraints Impact Analysis

Despite the significant growth prospects, the warehouse market faces several formidable restraints that could impede its expansion and efficiency. One of the primary barriers is the substantial initial capital investment required for building new, modern warehouses, particularly those equipped with advanced automation and sustainable technologies. This high cost can deter new entrants and limit expansion for smaller players. Another critical restraint is the pervasive issue of skilled labor shortages, especially for roles involving advanced technology operation and maintenance, which can lead to operational bottlenecks and increased labor costs. Furthermore, the scarcity of suitable land in urban and semi-urban areas, coupled with escalating real estate prices, poses a significant challenge for new developments. Stringent regulatory frameworks and environmental compliance requirements can also add to the complexity and cost of warehouse operations. Addressing these restraints will require innovative financing models, strategic workforce development, and creative urban planning to ensure the continued growth and modernization of the warehouse sector.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Developing a modern, automated warehouse requires substantial upfront capital for land acquisition, construction, equipment, and technology integration. This high investment cost can deter new entrants and limit expansion, particularly for smaller and medium-sized enterprises. | -1.5% to -2.0% | Global, especially in regions with high land costs and strict financial regulations. | Short to Mid-term |

| A significant shortage of skilled labor, particularly for operating and maintaining advanced automated systems, managing complex logistics software, and data analysis, poses a challenge to optimal warehouse operations and efficiency. | -1.0% to -1.5% | Developed economies and rapidly industrializing regions with evolving workforce needs. | Mid to Long-term |

| Limited availability of large land parcels suitable for warehouse development, especially in urban and peri-urban areas, coupled with escalating real estate prices, makes expansion difficult and expensive, pushing developments further away from consumption centers. | -0.8% to -1.2% | Major metropolitan areas and logistics hubs globally, particularly in land-constrained regions like Western Europe and densely populated Asian countries. | Long-term |

| Complex and evolving regulatory landscapes, including building codes, environmental regulations, labor laws, and customs procedures, can increase compliance costs and lead to delays in development and operational efficiency. | -0.5% to -0.8% | Regions with stringent environmental and labor laws, e.g., European Union, certain states in North America. | Short to Mid-term |

| The integration of diverse technologies from various vendors can be complex and expensive, leading to interoperability issues and requiring significant IT infrastructure upgrades and specialized expertise. | -0.3% to -0.6% | Globally, particularly for companies adopting highly diversified technology stacks. | Short to Mid-term |

Warehouse Market Opportunities Impact Analysis

The global warehouse market is ripe with substantial opportunities, offering pathways for significant growth and innovation. A key area of growth lies in the accelerated adoption of advanced automation and robotics, moving beyond traditional conveyor belts to sophisticated AI-driven systems that promise unparalleled efficiency and cost savings. The burgeoning trend of third-party logistics (3PL) services presents a unique opportunity, as businesses increasingly outsource their warehousing and distribution needs, creating demand for expert providers. Furthermore, the expansion into high-growth emerging markets, coupled with the development of multi-story and 'dark' warehouses to address urban land scarcity and enhance last-mile delivery, offers novel avenues for market penetration. The increasing emphasis on sustainability also creates opportunities for developing green warehousing solutions, attracting environmentally conscious clients and reducing operational costs in the long run. These opportunities underscore the dynamic nature of the warehouse market, driven by technological advancements, evolving business models, and a global shift towards more efficient and environmentally responsible logistics.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| The ongoing advancements and increasing affordability of automation and robotics, including AS/RS, AGVs, AMRs, and robotic picking systems, offer significant opportunities to enhance operational efficiency, reduce labor costs, and improve throughput in warehouses. | +2.0% to +2.5% | Global, particularly in developed economies and increasingly in emerging markets. | Short to Long-term |

| The rising trend of businesses outsourcing their warehousing, transportation, and fulfillment needs to third-party logistics (3PL) providers creates a substantial market for specialized, efficient, and technologically advanced warehouse services. | +1.5% to +2.0% | Global, especially prevalent in Europe and North America, expanding in Asia Pacific. | Mid to Long-term |

| Untapped or underserved markets in developing regions offer significant potential for warehouse development, driven by industrialization, increasing consumption, and improving infrastructure, providing greenfield investment opportunities. | +1.0% to +1.5% | Southeast Asia, India, Latin America, Africa, parts of Eastern Europe. | Long-term |

| The development of multi-story warehouses in urban areas helps overcome land scarcity, facilitates quicker last-mile delivery, and caters to the high-density storage needs of metropolitan areas, representing a novel architectural and operational approach. | +0.8% to +1.2% | Densely populated urban centers in Asia (e.g., Japan, Singapore, China) and Europe. | Mid to Long-term |

| Growing environmental consciousness and regulatory pressures are creating opportunities for the development of "green" warehouses that incorporate sustainable building materials, energy-efficient systems, renewable energy, and waste reduction strategies, appealing to eco-conscious clients and reducing long-term operational costs. | +0.5% to +0.8% | Primarily Europe and North America, with increasing adoption in Asia Pacific. | Mid to Long-term |

Warehouse Market Challenges Impact Analysis

The warehouse market, while dynamic and growing, navigates several significant challenges that demand strategic foresight and robust solutions. Foremost among these are ongoing global supply chain disruptions, which can lead to unpredictable inventory flows, storage capacity imbalances, and operational volatility. The rising and volatile energy costs, particularly for heating, cooling, and operating heavy machinery, directly impact operational profitability and sustainability efforts. Integrating a diverse array of new technologies, such as advanced robotics, AI, and IoT, presents complex challenges in terms of interoperability, system compatibility, and the need for highly specialized technical expertise. Furthermore, ensuring data security and privacy in increasingly digitized warehouse environments is paramount, given the growing threat of cyber-attacks. Finally, the perennial challenge of attracting and retaining skilled talent capable of managing sophisticated warehouse systems remains a critical hurdle, impacting both efficiency and the adoption of new technologies. Overcoming these challenges requires adaptability, significant investment in technology and human capital, and a proactive approach to risk management.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Unforeseen global events, such as pandemics, geopolitical conflicts, or natural disasters, can severely disrupt supply chains, leading to inventory backlogs, increased dwell times, and the need for flexible yet resilient warehousing solutions. | -1.2% to -1.8% | Global, impacting intercontinental trade routes and key manufacturing regions. | Short to Mid-term (Event-driven) |

| Fluctuations in energy prices (electricity, fuel) significantly impact operational costs, particularly for large, energy-intensive warehouses and cold storage facilities, affecting profitability and investment decisions. | Global, with higher impact in regions dependent on imported energy or with volatile energy markets. | Short to Mid-term | |

| Seamlessly integrating diverse automated systems, software platforms (WMS, WCS, TMS), and IoT devices from multiple vendors into a cohesive and interoperable system presents significant technical complexities, requires specialized IT expertise, and can lead to implementation delays and cost overruns. | -0.8% to -1.2% | Globally, particularly for companies undergoing extensive digital transformation. | Mid-term |

| As warehouses become more digitized and interconnected, they become vulnerable to cyber-attacks, data breaches, and ransomware, risking operational shutdowns, financial losses, and damage to reputation, necessitating robust cybersecurity measures. | -0.5% to -0.8% | Global, especially for highly automated and data-driven warehouses. | Ongoing |

| Attracting, training, and retaining a workforce with the necessary skills for operating and maintaining advanced warehouse technologies, alongside traditional logistics roles, is increasingly difficult, leading to higher labor costs and potential operational inefficiencies. | -0.3% to -0.6% | Developed economies with tight labor markets. | Long-term |

Warehouse Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Warehouse Market, offering critical insights into its current size, future growth projections, and key market dynamics. It covers a detailed segmentation by various parameters, extensive regional analysis, and a profile of leading industry players, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Report Name | Warehouse Market |

| Market Size in 2025 | USD 520.5 billion |

| Market Forecast in 2033 | USD 1,090.2 billion |

| Growth Rate | CAGR of 9.8% from 2025 to 2033 |

| Number of Pages | 250 |

| Key Companies Covered | CWT, GKE, Accessworld, Steinweg, Glprop, Macquarie Group, AMB, Hnagroup, JD, SF-Express |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

: Market Product Type Segmentation:-- General Warehouse

- Intelligent Warehouse

- Machining

- Transfering

- Storing

Regional Highlights

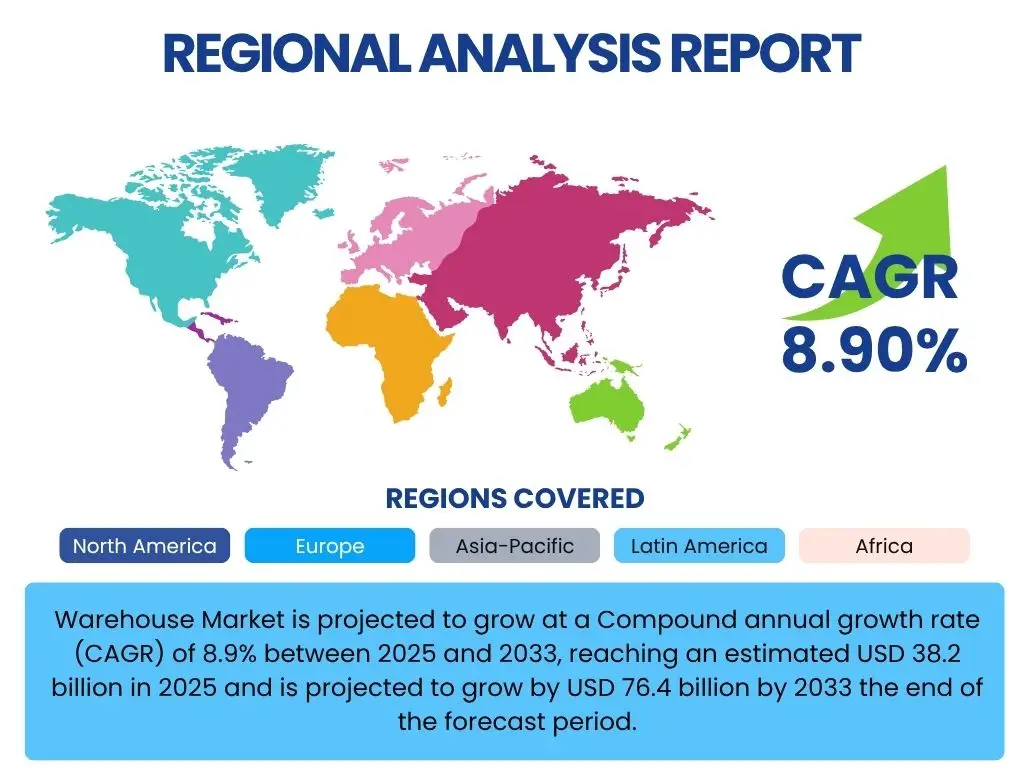

The global Warehouse Market exhibits diverse growth trajectories across different geographical regions, each driven by unique economic, technological, and logistical factors. Understanding these regional dynamics is crucial for strategic market positioning.- North America: This region is a leading market, primarily driven by the robust growth of e-commerce, significant investments in automation and robotics, and the increasing demand for expedited shipping and last-mile delivery solutions. The presence of major retail and logistics players, coupled with a focus on supply chain resilience and reshoring of manufacturing, further propels market expansion here.

- Europe: Europe represents a mature yet dynamic market, characterized by advanced logistics infrastructure, stringent environmental regulations, and a strong emphasis on sustainability. The adoption of smart warehousing technologies, consolidation of logistics hubs, and the growth of cross-border e-commerce within the EU are key drivers.

- Asia Pacific (APAC): APAC is expected to be the fastest-growing region, fueled by rapid industrialization, burgeoning e-commerce penetration in countries like China and India, and massive investments in infrastructure development. The region's role as a global manufacturing hub also necessitates extensive warehousing facilities to support production and distribution networks.

- Latin America: This region presents emerging opportunities, driven by increasing foreign direct investment, expanding consumer markets, and ongoing improvements in logistics infrastructure. The growth of organized retail and e-commerce platforms is gradually modernizing the warehousing sector across key economies like Brazil and Mexico.

- Middle East and Africa (MEA): The MEA region is developing as a strategic logistics hub, particularly driven by large-scale infrastructure projects, diversification efforts away from oil economies, and its pivotal geographical location linking East and West. Investments in modern warehousing and distribution centers are increasing to support growing trade volumes and regional consumption.

Top Key Players:

The market research report covers the analysis of key stake holders of the Warehouse Market. Some of the leading players profiled in the report include -:- CWT

- GKE

- Accessworld

- Steinweg

- Glprop

- Macquarie Group

- AMB

- Hnagroup

- JD

- SF-Express

Frequently Asked Questions:

What is the projected growth rate of the Warehouse Market?

The Warehouse Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. This consistent growth is driven by the global expansion of e-commerce, the increasing complexity of supply chains, and significant advancements in warehouse automation technologies.

What factors are primarily driving the growth of the Warehouse Market?

Key drivers include the rapid expansion of e-commerce, which demands more fulfillment centers; the increasing adoption of automation, robotics, and AI for operational efficiency; and the globalization of trade, necessitating robust logistics infrastructure. Additionally, rising demand for specialized storage solutions like cold chains and the growth of third-party logistics (3PL) services are significant contributors.

How is Artificial Intelligence (AI) impacting warehouse operations?

AI is transforming warehouse operations by enabling predictive demand forecasting, optimizing picking and routing processes, enhancing inventory management, and powering autonomous mobile robots (AMRs). It also contributes to automated quality control and predictive maintenance, leading to significant improvements in efficiency, accuracy, and cost reduction.

What are the main types of warehouses in the market?

The market primarily segments warehouses into two main types: General Warehouses, which are traditional storage facilities, and Intelligent Warehouses, which incorporate advanced technologies like automation, IoT, and AI for enhanced operational efficiency and data-driven management. The intelligent warehouse segment is experiencing rapid growth due to technological advancements.

What are the primary challenges faced by the Warehouse Market?

Key challenges include high initial capital investment for modern facilities, persistent skilled labor shortages, scarcity and rising costs of suitable land for development, and the complexities of integrating diverse new technologies. Additionally, ensuring cybersecurity in digitized environments and mitigating the impact of supply chain disruptions remain significant hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted